Updated on July 8th, 2026 by Nathan Parsh

Only the best companies can increase dividends through multiple recessions.

The Dividend Kings are a group of stocks that have increased their dividends for at least 50 consecutive years. Accomplishing this task is no small feat. The fact that only 58 companies meet the requirement to become a Dividend King is evidence of this.

You can see all 58 Dividend Kings here.

You can also download an Excel spreadsheet with the full list of Dividend Kings (plus important metrics such as price-to-earnings ratios and dividend yields) by clicking on the link below:

Johnson & Johnson (JNJ) has increased its dividend for 64 consecutive years, one of the longest dividend growth streaks in the stock market.

This healthcare giant is one of the most popular dividend growth stocks due to its excellent recession-resistant business model and strong dividend track record.

Johnson & Johnson stock remains an excellent holding for long-term dividend growth.

Business Overview

Johnson & Johnson was founded in 1886 and has transformed into one of the largest companies in the world. Johnson & Johnson is a mega-cap stock with a market capitalization of $640 billion. The company generates annual sales of $94 billion.

Johnson & Johnson operates a diversified business model, enabling it to appeal to a broad range of customers within the healthcare sector. J&J now operates two segments: pharmaceuticals and medical devices, following the spin-off of its consumer health businesses.

Growth Prospects

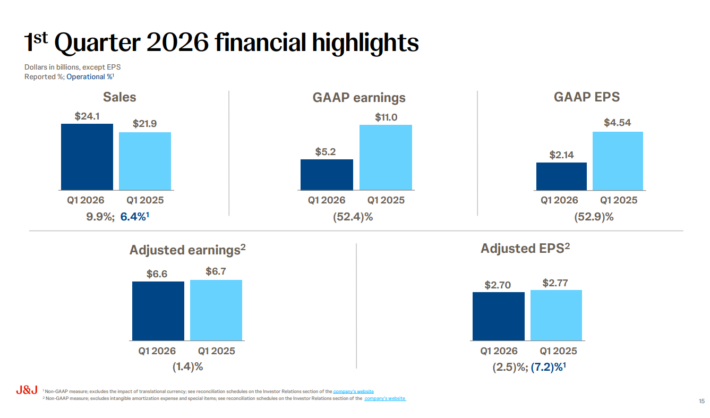

Johnson & Johnson reported first-quarter results on April 14th, 2026.

Source: Investor Presentation

For the period, revenue increased nearly 10% to $24.1 billion, which beat estimates by $450 million. Adjusted earnings-per-share of $2.70 was down from $2.77 in the prior year, but this was $0.20 better than expected.

Regionally, U.S. sales increased by 8.3%, while international markets were up 11.9%, resulting in 9.9% growth in total worldwide sales. Adjusting for currency exchange, revenue grew 6.4% worldwide.

The Innovative Medicine segment reported 7.4% currency-neutral growth, driven by strength in oncology and neuroscience, offset by weaker results in immunology. MedTech grew 4.6% as all product categories were higher for the period, with cardiovascular leading the way with double-digit sales growth.

Johnson & Johnson revised its full-year 2026 guidance to reflect better operational performance. The company anticipates adjusted EPS to be in the range of $11.45 to $11.65, up from the previously reported range of $11.28 to $11.48. This would represent 7% growth at the midpoint. Sales for 2026 are expected to grow between 5.6% and 6.6%, demonstrating management’s confidence in sustained growth.

Source: Investor Presentation

We expect Johnson & Johnson to generate 6% annual earnings-per-share growth over the next five years. The pharmaceutical segment will continue to be the company’s main growth driver, as it has for several years.

Competitive Advantages & Recession Performance

Johnson & Johnson has multiple advantages over its competitors.

Johnson & Johnson’s size and scale are unmatched in its industry. It also has a AAA credit rating from Standard & Poor’s and Moody’s Investors Service, which is higher than the U.S. government’s.

Microsoft Corporation (MSFT) is the only other company with an AAA credit rating.

The company’s size and scale, along with its credit rating, provide Johnson & Johnson with the financial flexibility to make acquisitions that fuel further growth.

Johnson & Johnson also invests heavily in research and development to bring new products to market. This investment has resulted in the company’s extensive portfolio of brands that lead their respective categories.

These competitive advantages allowed Johnson & Johnson to weather multiple recessions. Listed below are the company’s earnings-per-share results before, during, and after the last major recession:

2006 earnings-per-share: $3.76

2007 earnings-per-share: $4.15 (9.4% increase)

2008 earnings-per-share: $4.57 (10.1% increase)

2009 earnings-per-share: $4.63 (1.3% increase)

2010 earnings-per-share: $4.76 (2.8% increase)

Johnson & Johnson had EPS growth of almost 12% from 2007 through 2009, an impressive accomplishment given the circumstances of the Great Recession.

The company’s dividend also continued to grow. With more than six decades of dividend growth, Johnson & Johnson is likely to continue increasing its dividend well into the future. Additionally, the spinoff of its consumer business has allowed Johnson & Johnson to focus on the growth aspects of its business, which could lead to improved results and a higher multiple from the market.

Johnson & Johnson’s competitive advantages and recession performance make the stock an excellent defensive stock.

Valuation & Expected Returns

With a current share price of $266 and expected earnings per share of $11.55 for the year, Johnson & Johnson has a price-to-earnings ratio of 23.0.

We view the stock as slightly overvalued, with a fair value P/E estimate of 17. Multiple contraction to 17 from 23 could reduce annual returns by 2.1% over the next five years.

Total returns will also consist of earnings growth and dividends.

Given the company’s competitive advantages and recent business performance, we feel that a 6% average annual EPS growth rate is achievable over the next five years.

Finally, Johnson & Johnson stock has a current dividend yield of 2.0%. Therefore, total annual returns are expected to be 2.1% annually through 2030.

Final Thoughts

Few Dividend Kings are as well-known or popular among dividend growth investors as Johnson & Johnson.

For good reason, Johnson & Johnson’s diversified business model has enabled the company to endure several recessions while still increasing its dividends for the past 64 years. This growth streak is nearly unmatched.

That being said, the stock is trading above our target multiple, which could mean that a valuation headwind could cap total returns over the medium-term. For that reason, we rate shares of Johnson & Johnson as a hold.

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

-1024x668.jpg "What’s the Deal with Vance’s War on Milton Friedman?")

-1024x683.jpg "Strait Outta Hormuz: Getting the Iran Oil Story Straight")

Has a Digital-Distribution and Service Engine Bigger Than an Industrial-Cycle Trade")

{kind=link}