Published on June 1st, 2026 by Bob Ciura

Many investors focus on the biggest stocks in the market –called large caps – for their stability and predictability. This makes large cap stocks generally appealing to income investors.

On the other side, some investors focus on small caps because they tend to offer stronger growth potential.

Between them is a group that is often overlooked: midcap stocks.

These are generally stocks with market caps of $2 billion to $10 billion.

Despite their modest market caps, there are many midcap stocks with high dividend yields above 5%.

You can download your copy of the high dividend stocks list below:

The appeal of midcap stocks is that they could be in the “sweet spot” of market caps.

While small caps are potentially riskier businesses and large caps may lack growth opportunities, midcaps are large enough to achieve profitability while small enough to retain their long-term growth potential.

This article will rank the 10 best midcap dividend stocks in the Sure Analysis Research Database with the highest expected total returns over the next five years.

The list excludes REITs, MLPs, BDCs, and international stocks.

Table of Contents

Best Midcap Stock #10: Wesbanco, Inc. (WSBC)

Expected Annual Returns: 12.8%

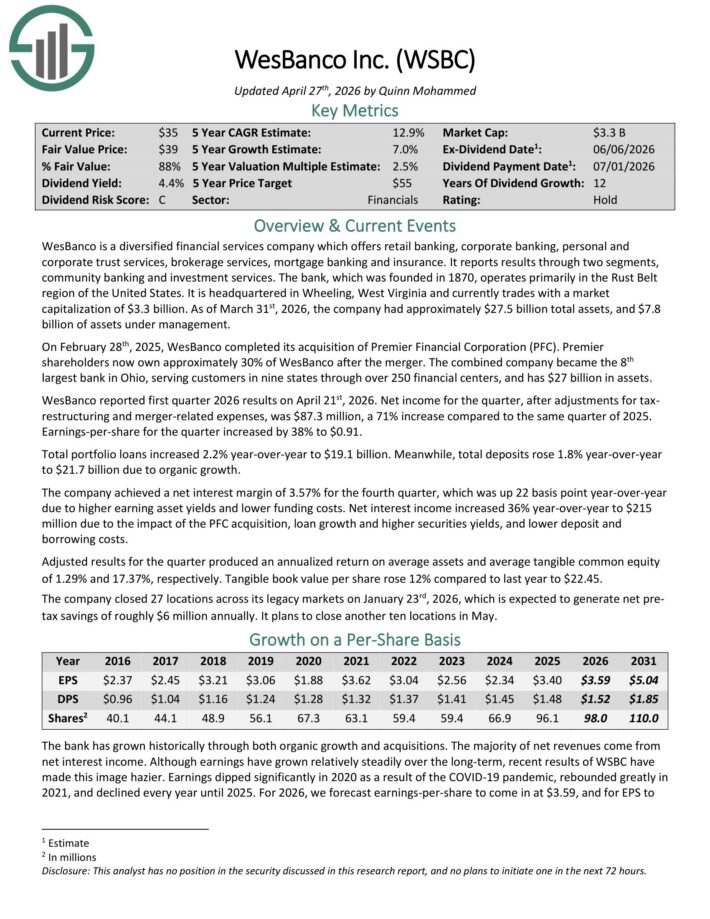

WesBanco is a diversified financial services company which offers retail banking, corporate banking, personal and corporate trust services, brokerage services, mortgage banking and insurance.

It reports results through two segments, community banking and investment services. The bank, which was founded in 1870, operates primarily in the Rust Belt region of the United States.

As of March 31st, 2026, the company had approximately $27.5 billion total assets, and $7.8 billion of assets under management.

WesBanco reported first quarter 2026 results on April 21st, 2026. Net income for the quarter, after adjustments for tax restructuring and merger-related expenses, was $87.3 million, a 71% increase compared to the same quarter of 2025. Earnings-per-share for the quarter increased by 38% to $0.91.

Total portfolio loans increased 2.2% year-over-year to $19.1 billion. Meanwhile, total deposits rose 1.8% year-over-year to $21.7 billion due to organic growth.

The company achieved a net interest margin of 3.57% for the fourth quarter, which was up 22 basis point year-over-year due to higher earning asset yields and lower funding costs.

Net interest income increased 36% year-over-year to $215 million due to the impact of the PFC acquisition, loan growth and higher securities yields, and lower deposit and borrowing costs.

Adjusted results for the quarter produced an annualized return on average assets and average tangible common equity of 1.29% and 17.37%, respectively. Tangible book value per share rose 12% compared to last year to $22.45.

Click here to download our most recent Sure Analysis report on WSBC (preview of page 1 of 3 shown below):

Best Midcap Stock #9: Portland General Electric (POR)

Expected Annual Returns: 13.0%

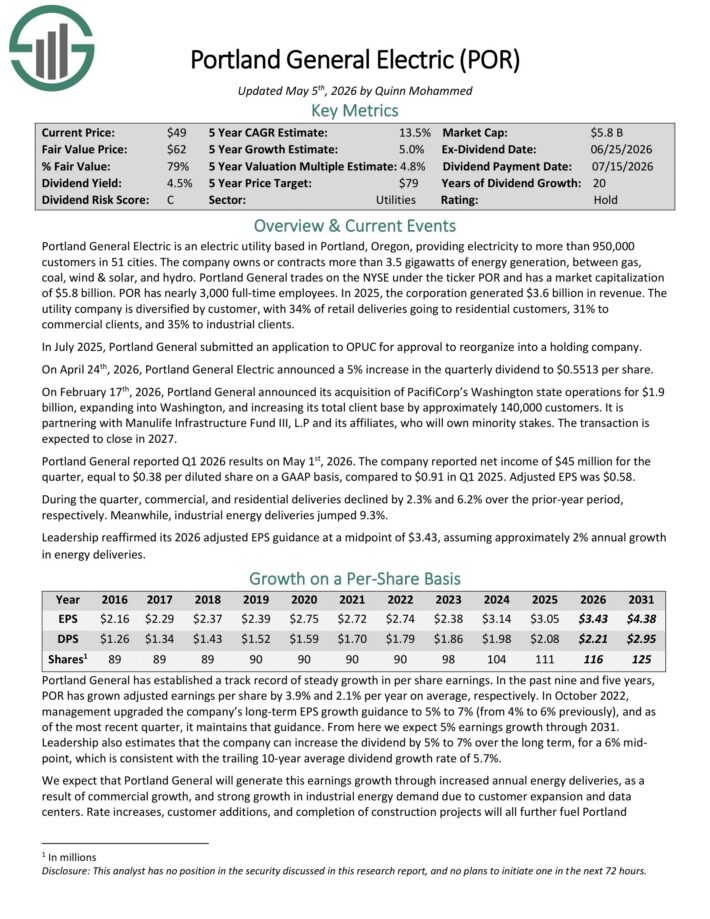

Portland General Electric is an electric utility based in Portland, Oregon, providing electricity to more than 950,000 customers in 51 cities.

The company owns or contracts more than 3.5 gigawatts of energy generation, between gas, coal, wind & solar, and hydro. In 2025, the corporation generated $3.6 billion in revenue.

The utility company is diversified by customer, with 34% of retail deliveries going to residential customers, 31% to commercial clients, and 35% to industrial clients.

On April 24th, 2026, Portland General Electric announced a 5% increase in the quarterly dividend to $0.5513 per share.

Portland General reported Q1 2026 results on May 1st, 2026. The company reported net income of $45 million for the quarter, equal to $0.38 per diluted share on a GAAP basis, compared to $0.91 in Q1 2025. Adjusted EPS was $0.58.

During the quarter, commercial, and residential deliveries declined by 2.3% and 6.2% over the prior-year period, respectively. Meanwhile, industrial energy deliveries jumped 9.3%.

Leadership reaffirmed its 2026 adjusted EPS guidance at a midpoint of $3.43, assuming approximately 2% annual growth in energy deliveries.

Click here to download our most recent Sure Analysis report on POR (preview of page 1 of 3 shown below):

Best Midcap Stock #8: Simmons First National (SFNC)

Expected Annual Returns: 13.3%

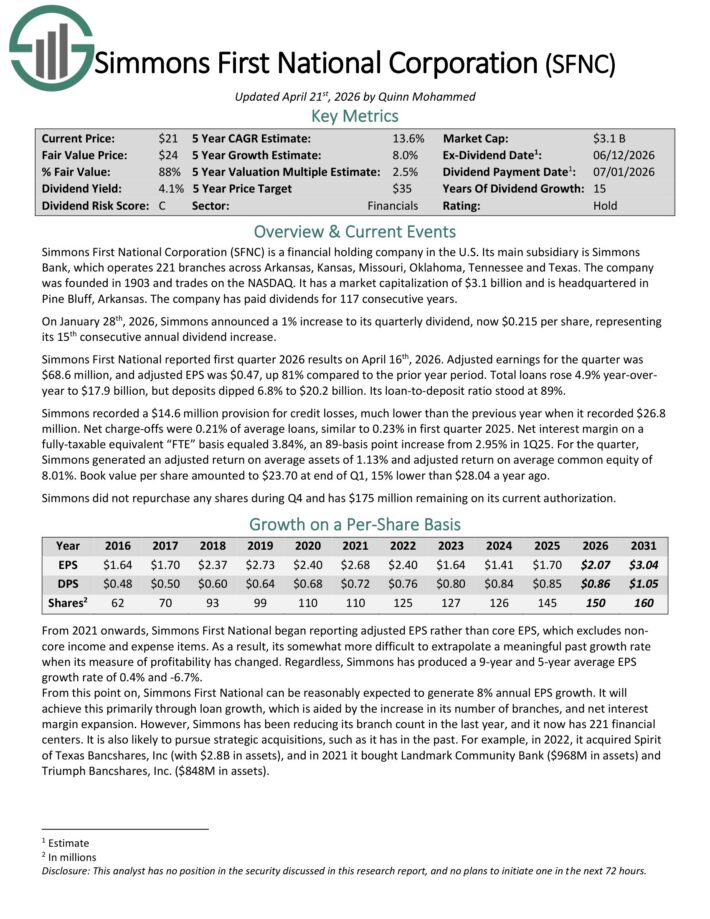

Simmons First National Corporation (SFNC) is a financial holding company in the U.S.

Its main subsidiary is Simmons Bank, which operates 221 branches across Arkansas, Kansas, Missouri, Oklahoma, Tennessee and Texas. The company has paid dividends for 117 consecutive years.

On January 28th, 2026, Simmons announced a 1% increase to its quarterly dividend, now $0.215 per share, representing its 15th consecutive annual dividend increase.

Simmons First National reported first quarter 2026 results on April 16th, 2026. Adjusted earnings for the quarter was $68.6 million, and adjusted EPS was $0.47, up 81% compared to the prior year period.

Total loans rose 4.9% year-over-year to $17.9 billion, but deposits dipped 6.8% to $20.2 billion. Its loan-to-deposit ratio stood at 89%.

Simmons recorded a $14.6 million provision for credit losses, much lower than the previous year when it recorded $26.8 million. Net charge-offs were 0.21% of average loans, similar to 0.23% in first quarter 2025.

Net interest margin on a fully-taxable equivalent “FTE” basis equaled 3.84%, an 89-basis point increase from 2.95% in 1Q25.

For the quarter, Simmons generated an adjusted return on average assets of 1.13% and adjusted return on average common equity of 8.01%. Book value per share amounted to $23.70 at end of Q1, 15% lower than $28.04 a year ago.

Click here to download our most recent Sure Analysis report on SFNC (preview of page 1 of 3 shown below):

Best Midcap Stock #7: LCI Industries (LCII)

Expected Annual Returns: 13.4%

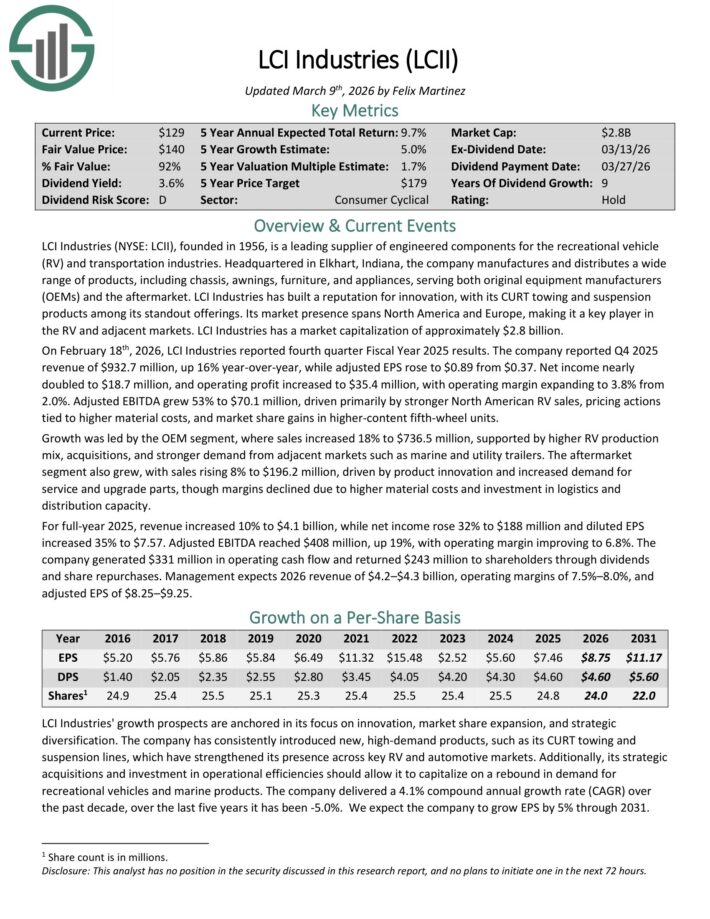

LCI Industries, founded in 1956, is a leading supplier of engineered components for the recreational vehicle (RV) and transportation industries.

The company manufactures and distributes a wide range of products, including chassis, awnings, furniture, and appliances, serving both original equipment manufacturers (OEMs) and the aftermarket.

On February 18th, 2026, LCI Industries reported fourth quarter Fiscal Year 2025 results. The company reported Q4 2025 revenue of $932.7 million, up 16% year-over-year, while adjusted EPS rose to $0.89 from $0.37.

Net income nearly doubled to $18.7 million, and operating profit increased to $35.4 million, with operating margin expanding to 3.8% from 2.0%.

Adjusted EBITDA grew 53% to $70.1 million, driven primarily by stronger North American RV sales, pricing actions tied to higher material costs, and market share gains in higher-content fifth-wheel units.

Growth was led by the OEM segment, where sales increased 18% to $736.5 million, supported by higher RV production mix, acquisitions, and stronger demand from adjacent markets such as marine and utility trailers.

The aftermarket segment also grew, with sales rising 8% to $196.2 million, driven by product innovation and increased demand for service and upgrade parts, though margins declined due to higher material costs and investment in logistics and distribution capacity.

For full-year 2025, revenue increased 10% to $4.1 billion, while net income rose 32% to $188 million and diluted EPS increased 35% to $7.57.

Click here to download our most recent Sure Analysis report on LCII (preview of page 1 of 3 shown below):

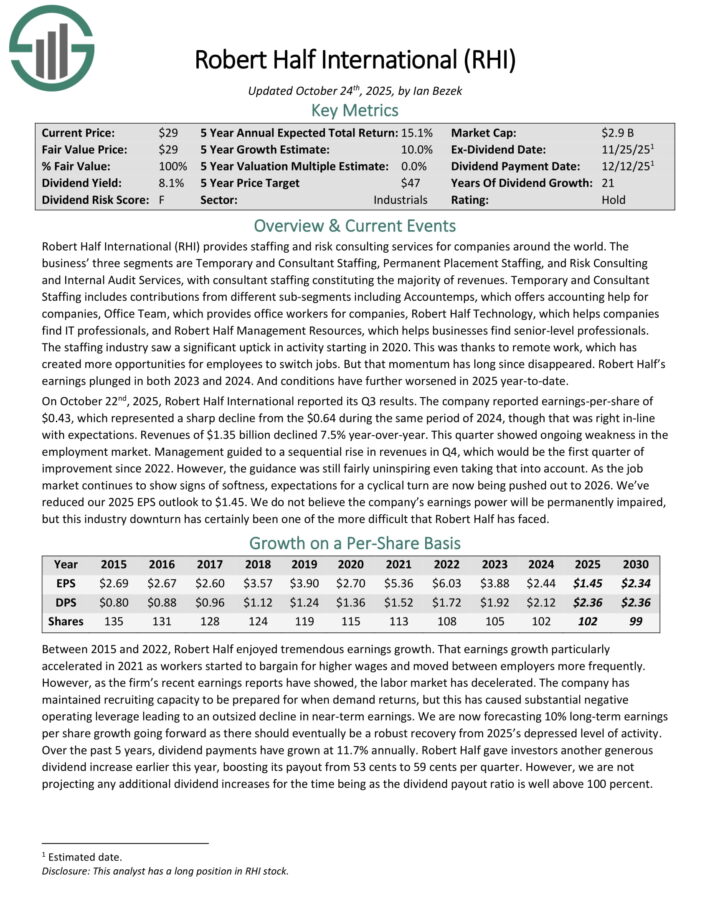

Best Midcap Stock #6: Robert Half Inc. (RHI)

Expected Annual Returns: 13.8%

Robert Half International provides staffing and risk consulting services for companies around the world.

Its three segments are Temporary and Consultant Staffing, Permanent Placement Staffing, and Risk Consulting and Internal Audit Services, with consultant staffing constituting the majority of revenues.

Temporary and Consultant Staffing includes contributions from different sub-segments including Accountemps, which offers accounting help for companies, Office Team, which provides office workers for companies, Robert Half Technology, which helps companies find IT professionals, and Robert Half Management Resources, which helps businesses find senior-level professionals.

Robert Half’s earnings plunged in both 2023 and 2024, and conditions further worsened in 2025.

On October 22nd, 2025, Robert Half International reported its Q3 results. The company reported earnings-per-share of $0.43, which represented a sharp decline from the $0.64 during the same period of 2024.

Revenue of $1.35 billion declined 7.5% year-over-year. This quarter showed ongoing weakness in the employment market. Management guided to a sequential rise in revenues in Q4, which would be the first quarter of improvement since 2022.

However, the guidance was still fairly uninspiring even taking that into account. As the job market continues to show signs of softness, expectations for a cyclical turn are now being pushed out to 2026.

Click here to download our most recent Sure Analysis report on RHI (preview of page 1 of 3 shown below):

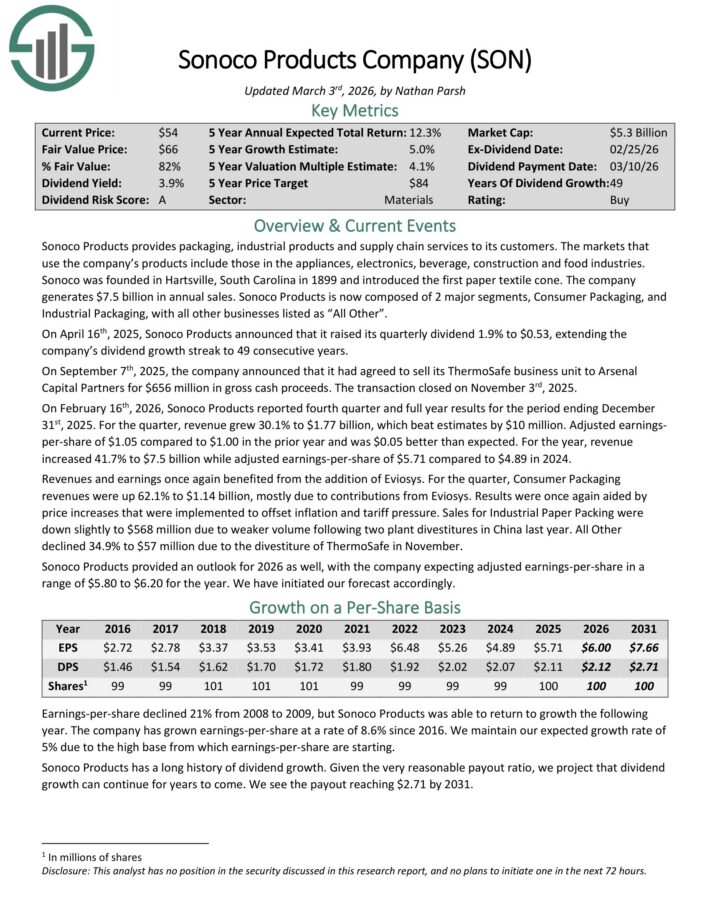

Best Midcap Stock #5: Sonoco Products (SON)

Expected Annual Returns: 13.9%

Sonoco Products provides packaging, industrial products and supply chain services. The markets that use the company’s products include those in the appliances, electronics, beverage, construction and food industries.

The company generates $7.5 billion in annual sales. Sonoco Products is now composed of 2 major segments, Consumer Packaging, and Industrial Packaging, with all other businesses listed as “All Other”.

On February 16th, 2026, Sonoco Products reported fourth quarter and full year results. For the quarter, revenue grew 30.1% to $1.77 billion, which beat estimates by $10 million.

Adjusted earnings-per-share of $1.05 compared to $1.00 in the prior year and was $0.05 better than expected.

For the year, revenue increased 41.7% to $7.5 billion while adjusted earnings-per-share of $5.71 compared to $4.89 in 2024.

For the quarter, Consumer Packaging revenues were up 62.1% to $1.14 billion, mostly due to contributions from Eviosys. Results were once again aided by price increases that were implemented to offset inflation and tariff pressure.

Sales for Industrial Paper Packing were down slightly to $568 million due to weaker volume following two plant divestitures in China last year. All Other declined 34.9% to $57 million due to the divestiture of ThermoSafe in November.

Sonoco Products provided an outlook for 2026 as well, with the company expecting adjusted earnings-per-share in a range of $5.80 to $6.20 for the year.

Click here to download our most recent Sure Analysis report on SON (preview of page 1 of 3 shown below):

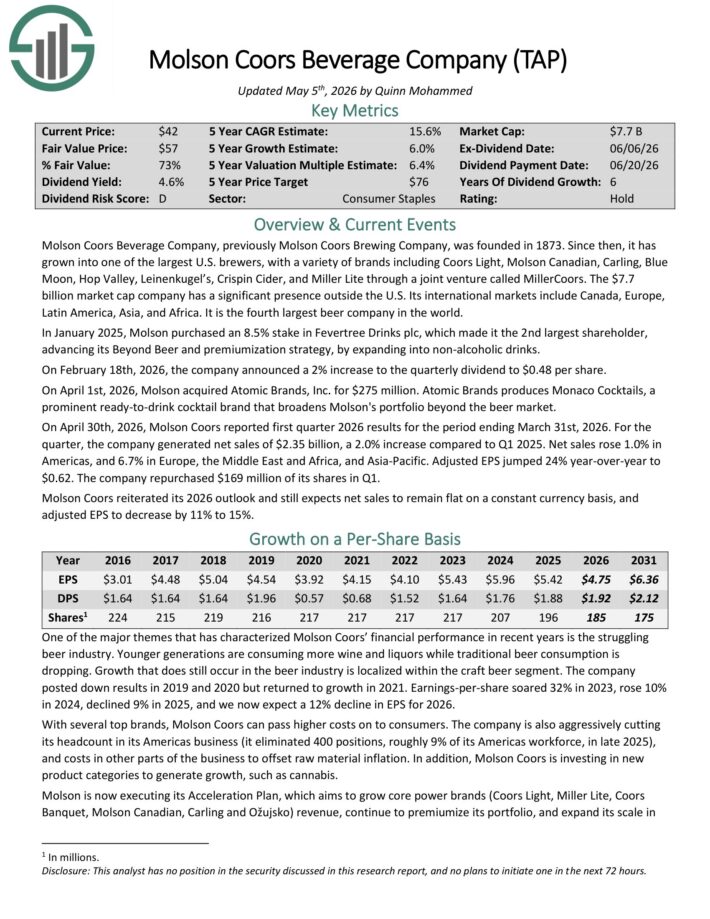

Best Midcap Stock #4: Molson Coors (TAP)

Expected Annual Returns: 16.7%

Molson Coors Beverage Company, previously Molson Coors Brewing Company, was founded in 1873.

Since then, it has grown into one of the largest U.S. brewers, with a variety of brands including Coors Light, Molson Canadian, Carling, Blue Moon, Hop Valley, Leinenkugel’s, Crispin Cider, and Miller Lite through a joint venture called MillerCoors.

On February 18th, 2026, the company announced a 2% increase to the quarterly dividend to $0.48 per share.

On April 1st, 2026, Molson acquired Atomic Brands, Inc. for $275 million. Atomic Brands produces Monaco Cocktails, a prominent ready-to-drink cocktail brand that broadens Molson’s portfolio beyond the beer market.

On April 30th, 2026, Molson Coors reported first quarter 2026 results for the period ending March 31st, 2026. For the quarter, the company generated net sales of $2.35 billion, a 2.0% increase compared to Q1 2025.

Net sales rose 1.0% in Americas, and 6.7% in Europe, the Middle East and Africa, and Asia-Pacific. Adjusted EPS jumped 24% year-over-year to $0.62. The company repurchased $169 million of its shares in Q1.

Molson Coors reiterated its 2026 outlook and still expects net sales to remain flat on a constant currency basis, and adjusted EPS to decrease by 11% to 15%.

Click here to download our most recent Sure Analysis report on TAP (preview of page 1 of 3 shown below):

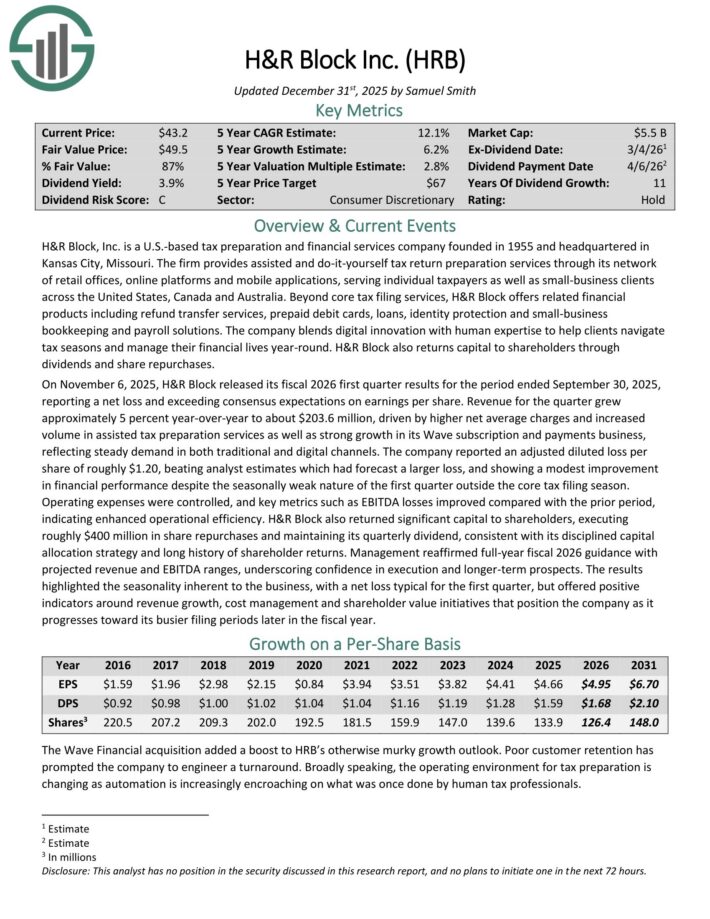

Best Midcap Stock #3: H&R Block (HRB)

Expected Annual Returns: 17.0%

H&R Block, Inc. is a U.S.-based tax preparation that provides assisted and do-it-yourself tax return preparation services through its network of retail offices, online platforms and mobile applications.

Beyond core tax filing services, H&R Block offers related financial products including refund transfer services, prepaid debit cards, loans, identity protection and small-business bookkeeping and payroll solutions.

On November 6, 2025, H&R Block released its fiscal 2026 first quarter results. Revenue for the quarter grew approximately 5% year-over-year to about $203.6 million.

Growth was driven by higher net average charges and increased volume in assisted tax preparation services as well as strong growth in its Wave subscription and payments business, reflecting steady demand in both traditional and digital channels.

The company reported an adjusted diluted loss per share of roughly $1.20, beating analyst estimates which had forecast a larger loss, and showing a modest improvement in financial performance despite the seasonally weak nature of the first quarter outside the core tax filing season.

Operating expenses were controlled, and key metrics such as EBITDA losses improved compared with the prior period, indicating enhanced operational efficiency.

H&R Block also returned significant capital to shareholders, executing roughly $400 million in share repurchases and maintained its quarterly dividend.

Click here to download our most recent Sure Analysis report on HRB (preview of page 1 of 3 shown below):

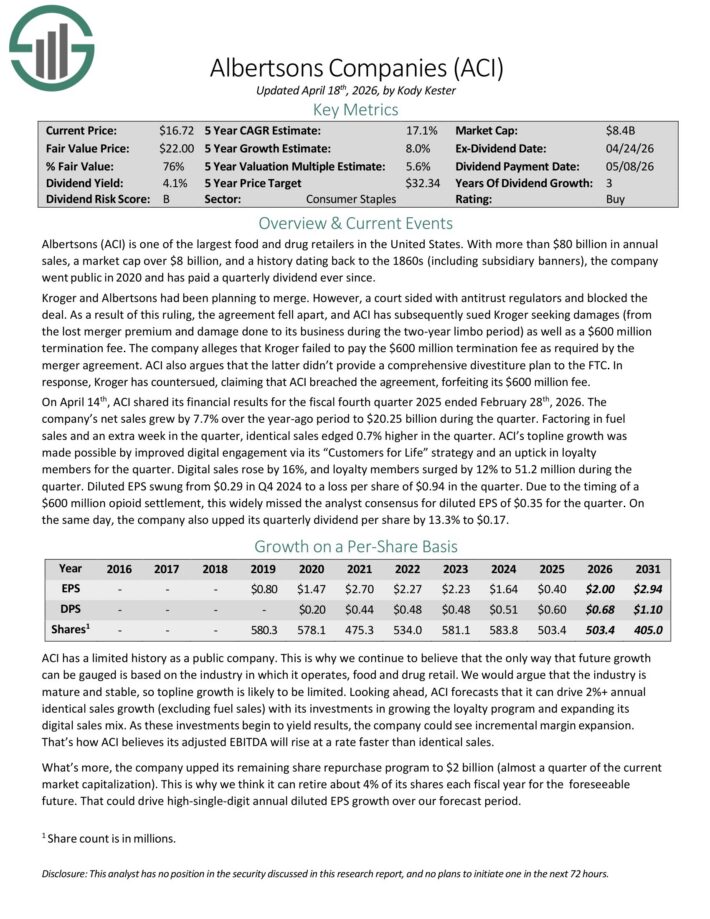

Best Midcap Stock #2: Albertsons Companies (ACI)

Expected Annual Returns: 18.8%

Albertsons (ACI) is one of the largest food and drug retailers in the United States.

With more than $80 billion in annual sales, and a history dating back to the 1860s (including subsidiary banners), the company went public in 2020 and has paid a quarterly dividend ever since.

On April 14th, ACI shared its financial results for the fiscal fourth quarter 2025 ended February 28th, 2026. The company’s net sales grew by 7.7% over the year-ago period to $20.25 billion during the quarter.

Factoring in fuel sales and an extra week in the quarter, identical sales edged 0.7% higher in the quarter. ACI’s topline growth was made possible by improved digital engagement via its “Customers for Life” strategy and an uptick in loyalty members for the quarter.

Digital sales rose by 16%, and loyalty members surged by 12% to 51.2 million during the quarter. Diluted EPS swung from $0.29 in Q4 2024 to a loss per share of $0.94 in the quarter.

Due to the timing of a $600 million opioid settlement, this widely missed the analyst consensus for diluted EPS of $0.35 for the quarter.

On the same day, the company also upped its quarterly dividend per share by 13.3% to $0.17.

Click here to download our most recent Sure Analysis report on ACI (preview of page 1 of 3 shown below):

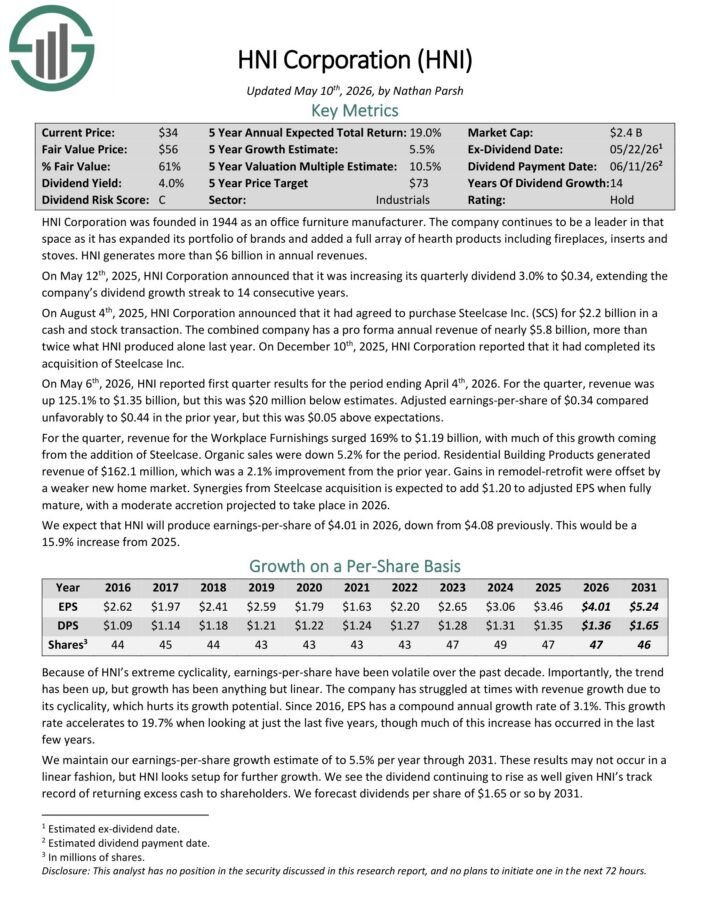

Best Midcap Stock #1: HNI Corp. (HNI)

Expected Annual Returns: 21.0%

HNI Corporation was founded in 1944 as an office furniture manufacturer. The company has a full array of hearth products including fireplaces, inserts and stoves. HNI generates more than $6 billion in annual revenue.

On May 6th, 2026, HNI reported first quarter results for the period ending April 4th, 2026. For the quarter, revenue was up 125.1% to $1.35 billion, but this was $20 million below estimates.

Adjusted earnings-per-share of $0.34 compared unfavorably to $0.44 in the prior year, but this was $0.05 above expectations.

For the quarter, revenue for the Workplace Furnishings surged 169% to $1.19 billion, with much of this growth coming from the addition of Steelcase. Organic sales were down 5.2% for the period.

Residential Building Products generated revenue of $162.1 million, which was a 2.1% improvement from the prior year. Gains in remodel-retrofit were offset by a weaker new home market.

Synergies from Steelcase acquisition is expected to add $1.20 to adjusted EPS when fully mature, with a moderate accretion projected to take place in 2026.

Click here to download our most recent Sure Analysis report on HNI (preview of page 1 of 3 shown below):

Additional Reading

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

")

with This Scalable Rental Strategy")

{kind=link}