Published on May 15th, 2026 by Josh Arnold

Cardinal Energy (CRLFF) has two appealing investment characteristics:

#1: It is offering an above-average dividend yield of 5.8%, which is nearly six times the average dividend yield of the S&P 500.

#2: It pays dividends monthly instead of quarterly.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

Cardinal Energy’s combination of an above-average dividend yield and a monthly dividend makes it an attractive option for individual investors, and particularly those that rely on dividend income for living expenses.

But there’s more to the company than just these factors. Keep reading this article to learn more about Cardinal Energy.

Business Overview

Cardinal Energy is a Canadian oil and gas producer that has operations primarily in Alberta and Saskatchewan, with a strong focus on conventional light and medium oil.

Its operations are centered on mature, low-decline fields where enhanced oil recovery methods, such as water flooding and CO₂ injection, are actively used to maintain stable production. The company was formed in 2010 and is headquartered in Calgary, Canada.

Cardinal Energy manages a large inventory of vertical and horizontal wells tied into company-owned infrastructure, which supports efficient field operations and cost control.

With over 90% of production weighted to oil and natural gas liquids (NGLs), Cardinal’s day-to-day operations are heavily oil-driven, with ongoing maintenance, re-completions, and targeted infill drilling forming the backbone of its development activity.

As an almost pure oil producer, Cardinal Energy is highly sensitive to the dramatic cycles of the oil industry. It has reported losses in 4 of the last 10 years and has exhibited a highly volatile performance record. There have been other years where it produced a profit, but only just above breakeven. The company initiated a dividend in 2014, but has cut the payout repeatedly and even briefly eliminated it over that period.

On the other hand, Cardinal Energy has some advantages compared to well-known oil producers. Most oil and gas producers have been struggling to replenish their reserves due to the natural decline of their producing wells.

Source: Investor Presentation

Cardinal Energy is the conventional producer with the lowest decline rate in Canada. This is a major competitive advantage, as the company needs to spend lower amounts on capital expenses than most of its peers to replenish its reserves. The company also continues to grow its proved and probable reserves, which certainly bodes well for future production growth.

In the first quarter of this year, Cardinal Energy maintained essentially flat production vs. the prior year’s quarter but its earnings per share dipped 20%, from $0.15 to $0.12, primarily due to a decrease in realized oil prices.

Cardinal posted fourth quarter and full-year earnings on March 12th, 2026, and results were somewhat mixed. Net revenue was just under $80 million, which was off 12% year-over-year. Record production volumes were offset by notably lower realized commodity prices. Production average 23,514 barrels of oil equivalent per day, which was up 7% year-over-year. Crude oil and NGLs made up 91% of total production mix.

Adjusted funds flow was $34 million, reflecting weaker global pricing, partially offset by the Reford thermal project. Diluted earnings-per-share came to -$0.13, sharply worse than the profit of 12 cents a year earlier. For this year, we expect earnings of $1.00 per share.

Growth Prospects

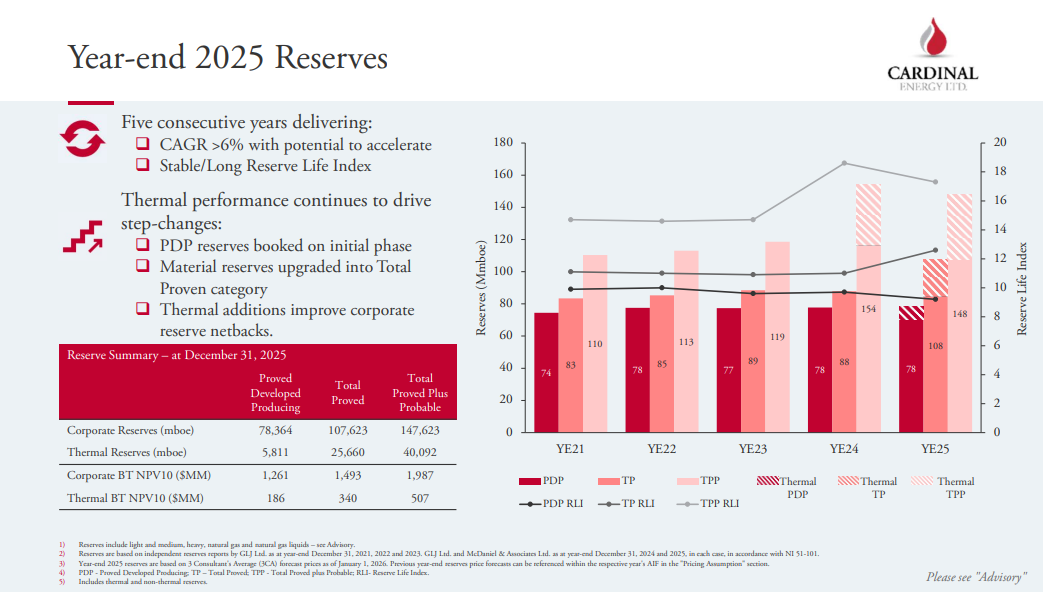

Cardinal Energy has posted one of the highest reserve growth rates in its peer group in recent years.

Source: Investor Presentation

Even better, the company has ample room for future growth thanks to some growth projects.

Cardinal Energy has provided guidance for average production of ~25,000 barrels per day this year. If it meets its guidance, it will post meaningfully higher output compared to last year, thanks to the Reford project.

However, when the ongoing growth projects begin to contribute to the output of the company, they are likely to result in meaningful production growth.

Overall, in the absence of a major downturn, Cardinal Energy can grow its earnings per share by 5% per year on average over the next five years.

On the other hand, as an oil producer, Cardinal Energy is highly sensitive to the fluctuations in the price of oil. The company posted record earnings per share in 2021 and 2022 thanks to the recovery of global oil consumption, which led the price of oil to surge to a 13-year high.

The war in Iran has driven global energy prices up very sharply in 2026, and Cardinal stands to be a significant beneficiary.

As a result, the earnings per share of Cardinal Energy have decreased from an all-time high of $1.46 in 2021 and $1.42 in 2022 to $0.47 in 2024, and just $0.09 in 2025. We expect earnings per share of approximately $1 this year.

Notably, Cardinal Energy has a rock-solid balance sheet. Its interest expense consumes just 3% of its operating income while its long-term debt is only $60 million, which is a tiny fraction of the $1.6 billion market capitalization of the stock.

A strong balance sheet is paramount in the oil industry, as it is likely to help the company endure future downturns in its business.

Dividend & Valuation Analysis

Cardinal Energy is currently offering an above-average dividend yield of 5.8%, which is more than five times the 1% yield of the S&P 500. The stock is an interesting candidate for income investors, but they should be aware that the dividend is far from safe due to the dramatic cycles of the price of oil.

Cardinal Energy has a modest payout ratio of 52%, which is sustainable over the long run so long as earnings hold up. Nevertheless, thanks to the solid financial position of the company, its dividend is not likely to be reduced dramatically under current oil prices.

In reference to the valuation, Cardinal Energy is currently trading for about 9 times its expected earnings per share this year. Given the high cyclicality of the company, we assume a fair price-to-earnings ratio of 9.0, which is a typical mid-cycle valuation level for oil producers.

Therefore, the current earnings multiple is right at the assumed fair price-to-earnings ratio. If the stock trades at its fair valuation level in five years, it will see basically no impact from the valuation.

Taking into account the 5.0% annual growth of earnings per share, the 5.8% current dividend yield and no impact from the valuation, Cardinal Energy could offer a ~10% average annual total return over the next five years.

The expected return signals that the stock is a good long-term investment, but only for those with a high risk tolerance.

Final Thoughts

Cardinal Energy has been thriving since 2021 thanks to an ideal environment of above-average oil prices. The stock is offering an above-average dividend yield of 5.8%, and the payout ratio has moderated of late. Given its decent growth prospects and its reasonable valuation, the stock appears attractive.

On the other hand, the company has proven highly vulnerable to the fluctuations in the price of oil. As a result, it is not suitable for investors who cannot stomach high stock price volatility.

Moreover, Cardinal Energy is characterized by low trading volume. This means that it is hard to establish or sell a large position in this stock. Still, the longer energy prices remain elevated, the better the outlook for Cardinal.

Additional Reading

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Strait Outta Hormuz: Getting the Iran Oil Story Straight")

Has an Oncology-and-Animal-Health Engine Bigger Than the Keytruda-Patent-Cliff Debate")

{kind=link}