Published on May 15th, 2026, by Josh Arnold

Monthly dividend stocks have instant appeal for many income investors. Stocks that pay their dividends each month offer more frequent payouts than traditional quarterly or semi-annual dividend payers.

For this reason, we created a full list of 119 monthly dividend stocks.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yields and payout ratios) by clicking on the link below:

Healthpeak Properties (DOC) switched to a monthly dividend payout schedule in April 2025. This potentially makes the stock more attractive for income investors looking for more frequent dividend payouts.

This article will analyze Healthpeak Properties in greater detail.

Business Overview

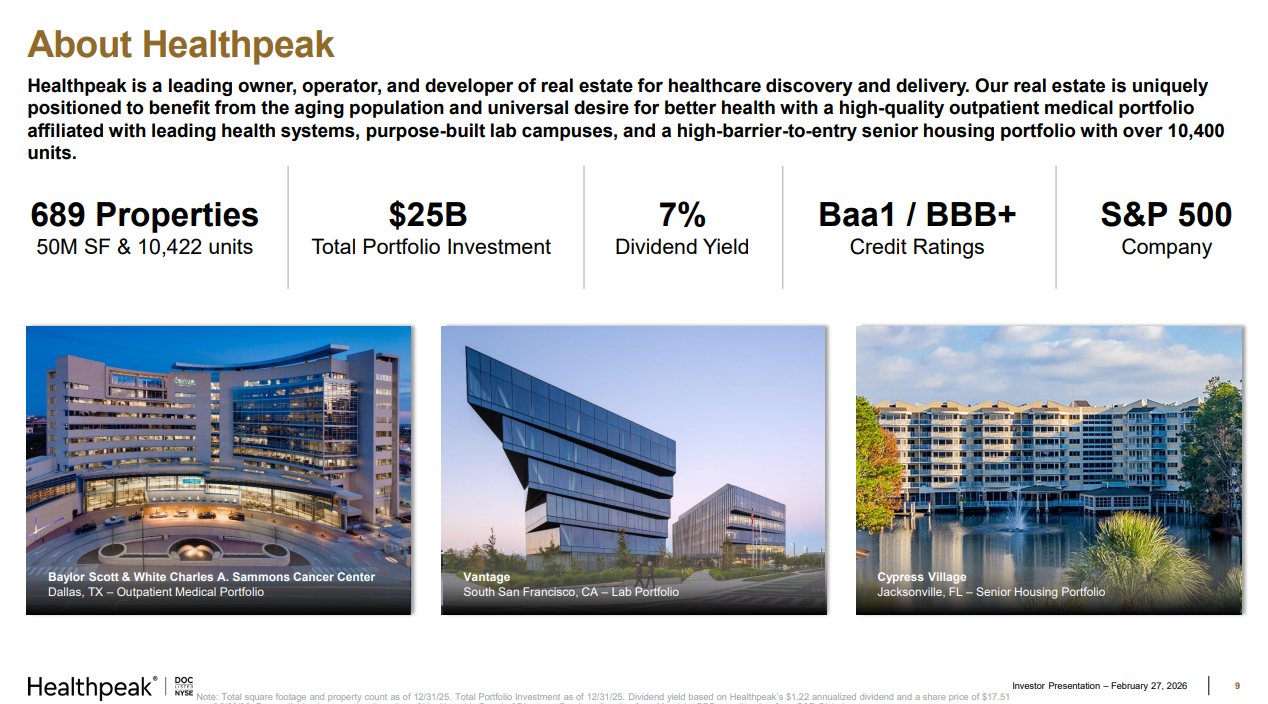

Healthpeak Properties is the largest healthcare REIT in the U.S., with 689 properties. It was the first healthcare REIT that was included in the S&P 500. The 38-year old REIT invests in life science facilities, senior houses, and medical offices, with 97% of its portfolio based on private-pay sources. It has a market capitalization of $14 billion.

Healthpeak Properties posted declining FFO for six consecutive years, until 2022. However, Healthpeak Properties has sold several assets and has used the proceeds to reduce its debt. As a result, the REIT has received credit rating upgrades from S&P and Fitch (to BBB+) as well as Moody’s (to Baa1).

Source: Investor Presentation

Healthpeak posted first quarter earnings on May 6th, 2026, and results were quite strong. Funds-from-operations per-share came to 45 cents, which was two cents ahead of estimates. Revenue was up 7.1% year-over-year to $753 million, beating estimates by a staggering $60 million.

The trust bought the Gateway campus in San Francisco at what it called a fraction of replacement cost. The campus has 62k square feet of signed leases and a further 113k square feet in progress. The trust also completed the IPO of its senior housing business in March of 2026, with the proceeds expected to add about four cents to earnings-per-share this year. Further, Healthpeak has closed more than $700 million of acquisitions.

Outpatient Medical finished the quarter at 91% total occupancy with a 5.4% cash re-leasing spread on renewals, and 79% tenant retention. Lab ended the quarter at 77.7% total occupancy.

Healthpeak bought back $100 million of stock in April at a 10%+ FFO yield, which management said allowed them to raise guidance.

Speaking of guidance, the trust now expects FFO of $1.70 to $1.74 per share, up two cents from prior on both ends of the range.

Growth Prospects

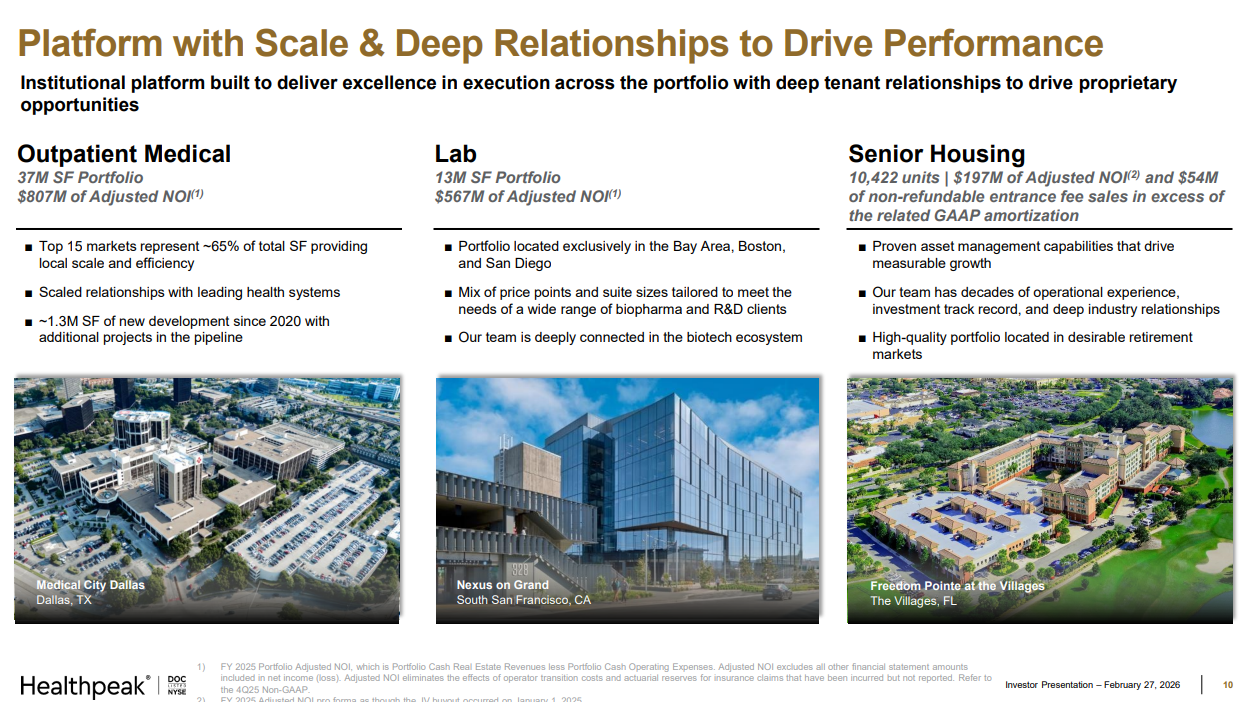

Healthpeak Properties benefits from favorable secular trends. As the baby boomer generation ages and the average life expectancy is on the rise, the senior population of the U.S. is expected to grow significantly in the upcoming years. The 80+ age group is expected to grow by about 5% per year on average until 2030.

In addition, this age group has immense spending power. Thanks to these trends, healthcare spending in the U.S. is expected to grow by about 5% per year on average until 2030. Healthpeak stands to benefit from this as it is solely focused on the ever-growing need for medical care and discovery.

Source: Investor Presentation

Although Healthpeak Properties posted declining FFO for six consecutive years, until 2022, and the restructuring process will keep burdening the REIT in the near future, most of the damage has already been done. We also expect the trust to enter a sustainable growth trajectory. Indeed, the trust has seen growing earnings every year since then, with expectations for that streak to end in 2026.

We expect earnings of $1.72 per-share on an adjusted basis this year, which would be meaningfully worse than last year’s $1.84 should that come to fruition. In addition, we see 3% annual growth going forward.

Dividend & Valuation Analysis

The performance of Healthpeak Properties has been poor at times in recent years and the REIT cut its dividend by -19% in 2021, due to the impacts of the coronavirus pandemic. As this was the second dividend cut in the last decade, it is evident that the REIT is vulnerable to downturns. To its credit, however, the dividend has been raised a couple of times since then.

In addition, interest expense has doubled since 2021 due to high interest rates and the Physicians Realty Trust merger.

On the other hand, we note that the payout ratio is steady at about 70% of earnings. DOC has a 2026 expected dividend payout ratio of 71%, based on the midpoint of the REIT’s adjusted FFO-per-share guidance for 2026. This indicates a sustainable dividend payout backed by sufficient FFO.

We also view the REIT as fairly valued. Based on expected adjusted FFO-per-share of $1.72 for 2026, shares of DOC currently trade for a price-to-FFO ratio of 11.4. This is modestly below our fair value estimate of 12.3 times FFO. That implies a small tailwind to total returns from a favorable valuation, should the stock trade up to that level over time.

We see total returns coming in at about 10% annually going forward, consisting mostly of the 6.2% dividend yield, 3% growth, and a small tailwind from the valuation.

Final Thoughts

Healthpeak Properties is a relatively new monthly dividend stock, having started paying its dividend on a monthly basis in April 2025.

The REIT has recovered from the various challenges faced during the pandemic, and could offer strong average annual returns over the next five years, thanks to growth of FFO per share, its 6.2% dividend yield, and a small expansion of the valuation multiple.

Nevertheless, due to the volatile performance record and the high debt load of the REIT, we rate it as a hold for patient, risk-tolerant investors who can endure extended periods of stock price pressure.

Additional Reading

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Strait Outta Hormuz: Getting the Iran Oil Story Straight")

Has an Oncology-and-Animal-Health Engine Bigger Than the Keytruda-Patent-Cliff Debate")

{kind=link}