The US president is, quite literally, throwing the world into disarray to the point that the traditional safe-haven asset, gold, has gone from significant gains to double-digit weekly declines. From a peak exceeding $5,600 per troy ounce towards the end of January of this year, it has fallen by more than 20 percent, the most abrupt—and unimaginable—drop in its history.

As the Greek philosophers said, violence—whose monopoly is claimed by states, creators of wars and all kinds of conflicts—is always contrary to the natural, spontaneous order of the cosmos and, therefore, disruptive.

Trump began by complicating the entire global economy with his tariffs, which his supporters defined as a “geopolitical strategy.” But even if this were true, it’s a strategy like spitting in the wind, since the tariffs are a tax on its own citizens and directly and primarily harm them.

And now there’s the war with Iran, which he is obviously losing, to the point that he has just stated that the Strait of Hormuz will be governed by him and the Ayatollah, thus consolidating the authority of the criminal regime in Iran.

Given this situation, it is frankly impossible today to try to predict the outcome of any investment anywhere in the world.

But be careful, despite the tactical weakness, the context of high debt, inflation, and low real benchmark interest rates continues to support gold in the medium and long term as the ultimate safe haven, as can be seen in the following chart, which shows its unbeatable performance beyond the current situation:

In the context of high geopolitical tension, the weakness of gold may seem counterintuitive. But the market reaction responds more to liquidity and positioning dynamics than to a questioning of its role as a safe-haven asset. In the initial stages of financial stress, investors typically cash in and sell their most profitable assets to generate liquidity.

Gold—after a strong previous rally—is now one of the main sources of cash to cover the unexpected losses resulting from the current uncertainty. This pattern—already observed in episodes like 2008 or the crisis created from the covid—implies widespread selling before the market returns to safe havens. It’s not that gold ceases to be a safe haven, but first the unexpected crisis caused by the war must be resolved, and then the future can be considered.

Turkey, for example, has accumulated significant official holdings of this precious metal over the last decade, with reserves valued at approximately $135 billion (USD) at the beginning of March, and is now reportedly considering selling a portion to support its currency, the lira, according to Bloomberg.

Added to this is the strengthening of the dollar, which is acting as the main safe haven in the current scenario. The inverse relationship between the two assets remains crucial, as a stronger dollar makes gold more expensive for international investors and puts downward pressure on its price.

Furthermore, the market focus has shifted towards energy, as tensions in the Strait of Hormuz have driven up oil prices and revived the perceived “inflationary” risk, attracting flows into energy-related assets at the expense of gold. The implicit message is clear: the dominant concern is not financial, but energy-related; that is, the market is increasing energy prices to discourage consumption while simultaneously encouraging new investments in production.

Now, this widespread error of confusing inflation with rising CPI figures—which, moreover, are arbitrary calculations depending on who is estimating them and how—leads to counterproductive policies and practices. Inflation is not the rise in prices, but rather the opposite: the depreciation of the currency because of excessive money printing in real time.

The relative movement of prices is normal and beneficial in the market. In this case, I reiterate that the rise in crude oil prices occurs because supply is tight, and therefore, the increased cost encourages less consumption and attempts to produce more.

Among the misguided policies promoted by this confusion is the widespread belief among state central banks that, to lower “inflation”—the rise in the CPI, strictly speaking—benchmark interest rates must be increased, which would cause a contraction in the money supply and, consequently, in the rise in prices in general.

But this increase, being artificial and not spontaneously induced by the market, causes a mismatch in investment and consumption since, in a free market, interest rates—denominated in money prices—arbitrate by efficiently directing the supply and demand of funds.

Because of this misconception about interest rates, many investors believe that—given the current situation and the “inflationary expectations” due to rising oil prices—the Fed will raise them, “strengthening” the dollar. It doesn’t strengthen the dollar at all, but it does make it more profitable, thus reducing the relative attractiveness of gold in the short term.

Many analysts, therefore, believe that in the short term, it is possible that gold will continue to show volatility or sideways movement in a market dominated by liquidity factors, the “strength” of the dollar, and the evolution of oil prices. However, the medium- and long-term outlook continues to support its strategic role given the combination of high global debt, structural purchases by central banks, persistent inflationary pressures, and potentially negative real interest rates, all of which create a favorable environment for gold.

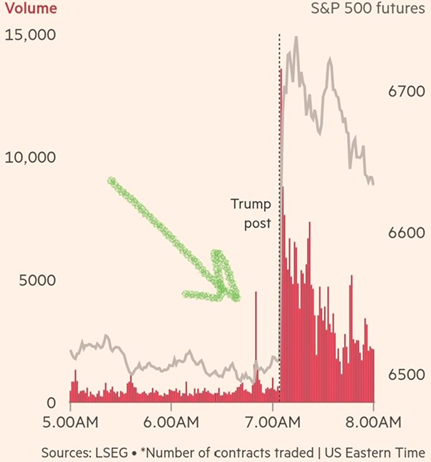

Finally, among other unusual behaviors in the financial markets in recent days, a group of “investors” bought S&P 500 futures contracts worth $1.5 billion—an operation so large that it caused the entire index to rise by 0.3 percent in that same minute, and sold crude oil worth around $500 million, as highlighted by the Financial Times.

A quarter of an hour later, Trump announced “productive talks” with Iran, which turned out to be false but immediately caused the stock market index to soar and these “investors” to earn $60 million in just fifteen minutes. Incidentally, some skeptics suspect that this could be the work of “insiders,” meaning corruption within the US government, because they allegedly used “internal information.”

")

{kind=link}