AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Guidance adjusted $3.49 – $3.63|Stock $32.72 (+2.6%)

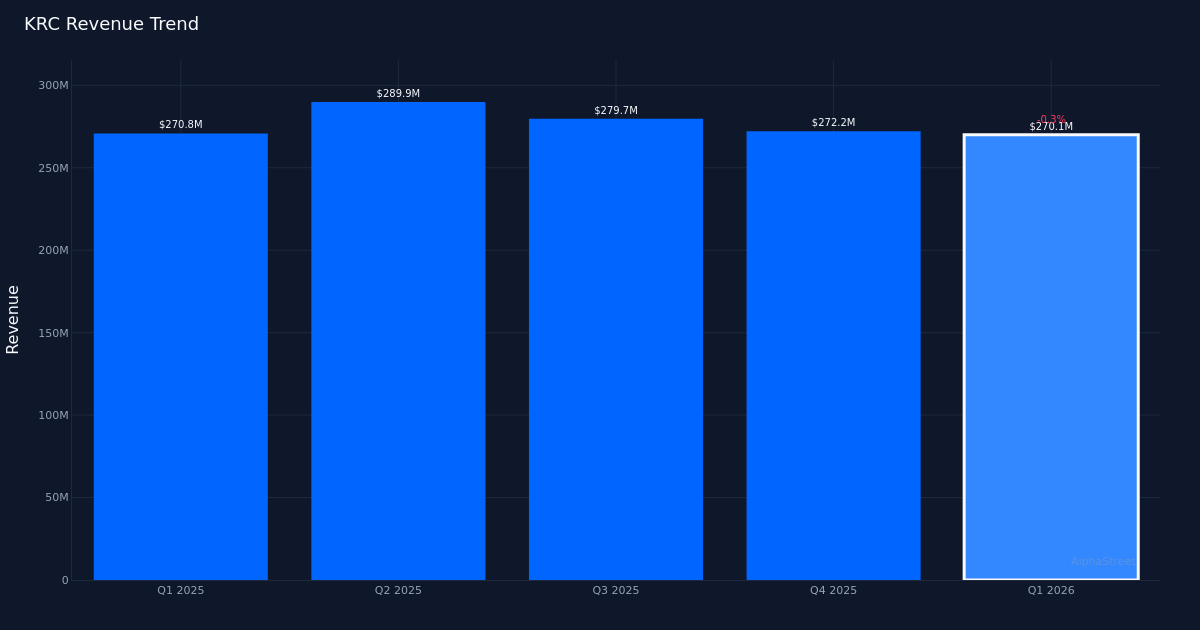

Disappointing Quarter. Kilroy Realty Corporation (NYSE: KRC) reported a net loss of $19.3M for Q1 2026, translating to a diluted loss per share of $0.16 compared to analyst expectations of $0.35 in earnings. The office REIT generated $270.1M in revenue for the quarter, representing a 0.3% decrease from the $270.8M recorded in Q1 2025. The company posted EPS of $0.33 in the prior-year period. The sharp swing from profitability to loss highlights the ongoing headwinds facing the office sector amid shifting workplace dynamics and elevated vacancy pressures.

Operational Footprint. The company’s stabilized office portfolio stood at 17,124,000 square feet at quarter end, reflecting its continued focus on premium office properties in key West Coast markets. While revenue remained relatively stable on a year-over-year basis with just a 0.3% decline, the inability to translate that top-line performance into profitability raises questions about margin pressure and operating expense management. Funds From Operations per common share/unit came in at $1 for the quarter, a critical metric for REIT investors that strips out non-cash charges and provides a clearer picture of the company’s cash-generating ability from its property operations.

Full-Year Outlook. Management provided FY 2026 adjusted EPS guidance of $3.49 to $3.63, signaling expectations for a significant improvement from the first quarter’s loss. This forward outlook suggests the company anticipates either materially stronger performance in the remaining quarters or that one-time items weighed particularly heavily on Q1 results. The guidance range implies management’s confidence in the portfolio’s ability to generate positive earnings despite the challenging start to the fiscal year, though investors will need clarity on the path to profitability and whether leasing momentum can support the optimistic projection.

Market Response. Shares rose 2.6% to $32.72 following the release, a counterintuitive reaction given the magnitude of the earnings miss and year-over-year deterioration. The positive stock movement may reflect either relief that results weren’t worse than feared, confidence in management’s full-year guidance, or technical buying after prolonged weakness in the office REIT sector. Wall Street sentiment remains cautious, with analyst consensus standing at 3 buy, 12 hold, and 2 sell ratings, reflecting the uncertain outlook for traditional office properties as hybrid work arrangements become entrenched.

What to Watch: The path to achieving management’s full-year adjusted EPS guidance of $3.49 to $3.63 will be critical, requiring substantial quarter-over-quarter improvement to offset the Q1 loss. Investors should monitor leasing velocity, tenant retention rates, and any portfolio repositioning efforts that could drive occupancy gains and margin expansion in subsequent quarters.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

")

")

")

{kind=link}