AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Related Coverage

Earnings Flash

Ambiq Micro Posts Narrower Q1 2026 Loss of -$0.25, 30.6% Better Than Forecast

May 12, 2026

Breaking News

Ambiq Micro Releases Q1 2026 Financial Results

May 12, 2026

Q2 EPS guidance – adjusted -$0.29 – -$0.23|Stock $66.37 (+45.3%)

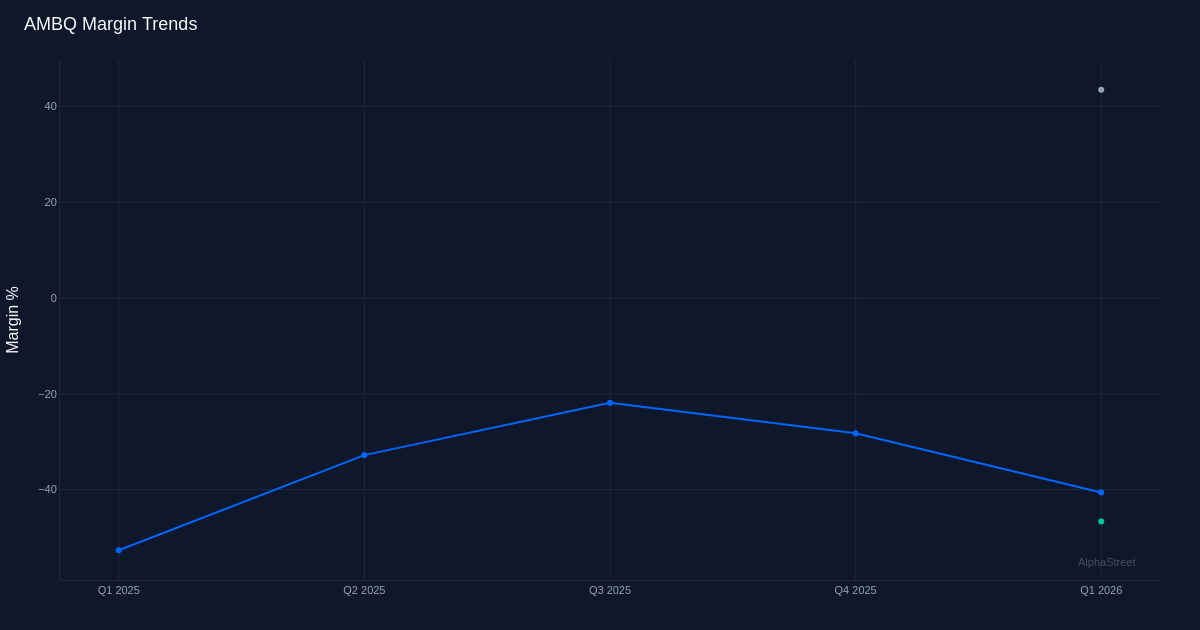

EPS YoY +98.7%|Rev YoY +59.3%|Net Margin -40.6%

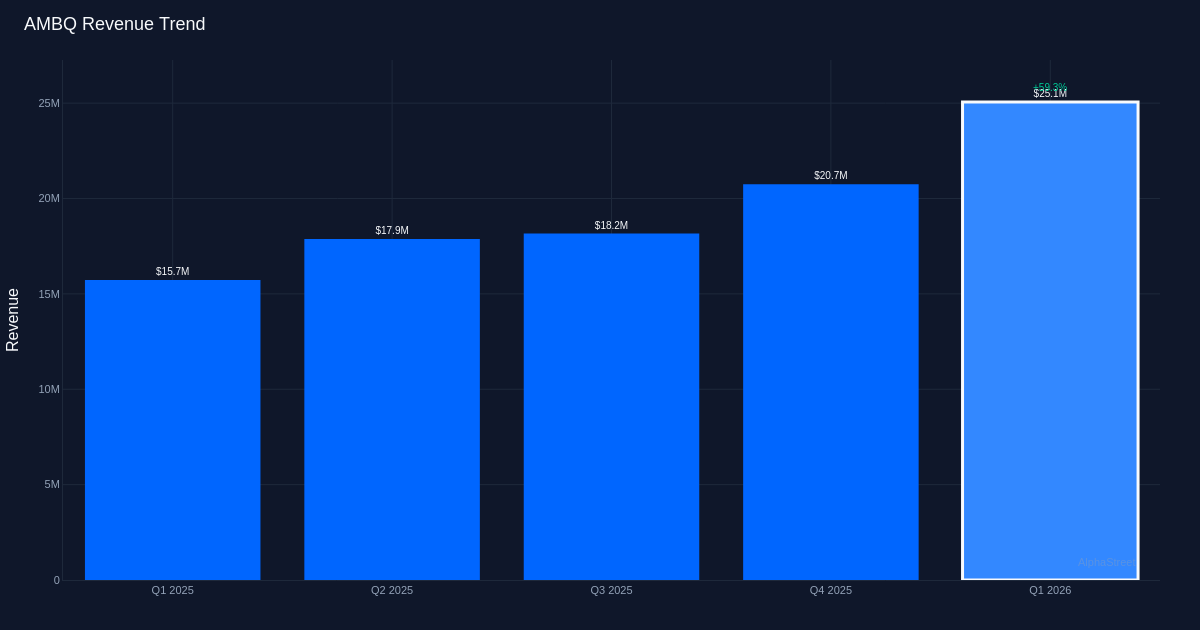

Ambiq Micro delivered a substantial beat in Q1 2026, posting a loss of $0.25 per share against expectations of $0.36, a 30.6% outperformance that sent shares soaring 45.3%. The semiconductor company’s revenue of $25.1M represented 59.3% year-over-year growth, marking the fourth consecutive quarter of sequential revenue expansion. At a current stock price of $66.37, investors are clearly betting that the company’s momentum in ultra-low-power semiconductors for AI applications represents a durable growth trajectory rather than a cyclical bump.

The quality of this beat reveals a company making meaningful progress on its path to profitability, though significant work remains. The net margin of -40.6% compares favorably to the year-ago figure of -52.9%, representing an improvement of 12.2 percentage points. This narrowing of losses occurred while revenue grew 59.9% year-over-year from $15.7M, indicating operational leverage is beginning to emerge in the model. The operating margin of -46.6% and gross margin of 43.4% paint a picture of a company with fundamentally sound unit economics at the product level, but still carrying substantial fixed costs that haven’t yet been absorbed by the revenue base. Management noted that spending runs approximately $21 million per quarter at current gross margin levels, highlighting the tension between investment in growth and near-term profitability.

The shift toward AI-enabled products represents the most strategically significant development in recent results. The company reported that 80.0% of units shipped are now running AI algorithms, a dramatic transformation in product mix that carries profound implications for both competitive positioning and pricing power. This isn’t incremental product evolution—it’s a wholesale pivot toward higher-value applications that should theoretically command premium pricing. Management’s commentary revealed particular strength in market diversification, noting “we grew 100% in a non wearable market” in Q1, suggesting the company is successfully breaking out of its historical concentration in wearables to address broader IoT and edge computing applications where AI functionality commands higher ASPs.

The Q2 guidance framework points to sustained momentum but requires careful interpretation. Management provided revenue guidance of $31.0M to $32.0M for Q2 2026, with a midpoint implying sequential growth from Q1’s $25.1M. The bottom line guidance of -$0.29 to -$0.23, with a midpoint of -$0.26, implies losses remain elevated relative to the Q1 actual of -$0.25, though this likely reflects typical seasonal patterns and investment timing. Management stated “For the second quarter, we expect net sales to grow approximately 75% year over year with momentum continuing in the second half of the year,” providing explicit conviction that growth rates will remain robust. The guidance translates to continued sequential revenue expansion, though at what appears to be a decelerating rate from recent quarterly gains.

Management’s confidence in the non-wearables expansion deserves particular scrutiny. The assertion that “we expect to continue to grow non wearable market as fast as we’ve been doing” following 100% growth in that segment suggests Ambiq is successfully executing on its strategy to diversify beyond its historical wearables concentration. This matters immensely for valuation—wearables represent a concentrated, mature market with established competitors, while broader IoT and edge AI applications offer far larger TAMs with less entrenched competition. The ability to maintain triple-digit growth in non-wearables while the overall business grows 59.3% year-over-year implies the wearables business is likely growing at a much slower rate, raising questions about long-term mix dynamics.

The cash generation profile shows early signs of improvement but remains challenged. Operating cash flow of $11.2M in Q1 compares to a net loss, suggesting working capital dynamics or non-cash charges are providing some cushion. However, with quarterly operating losses still substantial, the company’s ability to self-fund its growth trajectory without additional capital raises remains questionable. The 100% beat rate over the last quarter provides limited statistical comfort, though it does suggest management has adopted a conservative guidance philosophy following what was likely a challenging period of misses that preceded the available data.

The 45.3% stock surge reflects market conviction that inflection is real, but the valuation now embeds significant execution risk. At $66.37, investors are clearly pricing in successful execution on the AI-enabled product roadmap and continued share gains in non-wearables markets. The move also suggests the market views the narrowing losses and accelerating revenue as sustainable rather than transitory. However, this optimism creates little room for disappointment—any stumble in the growth trajectory or unexpected margin pressure could trigger sharp multiple compression.

What to Watch: The key forward catalyst is whether non-wearables can sustain triple-digit growth rates as the base scales, and whether the 80.0% mix shift toward AI-enabled products translates into gross margin expansion beyond the current 43.4%. Track whether Q2 results meet the high end of the revenue guidance range, which would confirm accelerating momentum.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

-1024x683.jpg "Strait Outta Hormuz: Getting the Iran Oil Story Straight")

-1024x683.jpg "Clinton vs Carville: Democrats Divided Over Socialism")

")

")

{kind=link}