Updated on May 8th, 2026 by Nathan Parsh

Whitecap Resources (WCPRF) has two appealing investment characteristics:

#1: It is offering an above-average dividend yield of 4.7%, which is more than four times the yield of the S&P 500.

#2: It pays dividends monthly instead of quarterly.Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

The combination of an above-average dividend yield and a monthly dividend makes Whitecap Resources an appealing option for individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about Whitecap Resources.

Business Overview

Whitecap Resources is an oil and gas company focused on acquiring, developing, and producing oil and gas in Western Canada. The company’s development programs focus on Northern Alberta and British Columbia, Central Alberta, and Saskatchewan. Whitecap Resources is headquartered in Calgary, Canada.

Whitecap Resources has some attractive characteristics. First of all, its assets are characterized by low decline rates. This is paramount in the oil and gas industry, as many producers suffer from high natural decline rates.

Source: Investor Presentation

As Whitecap Resources’ business is focused on oil and gas, it has exhibited a highly volatile performance record due to the dramatic cycles of oil and gas prices. The company has incurred material losses in three out of the last ten years. Therefore, investors should carefully identify the stage of the cycle in which this business operates before investing in this stock.

Like almost all oil and gas producers, Whitecap Resources incurred substantial losses ($3.55 per share) in 2020 due to the decline in oil and natural gas prices caused by the pandemic. However, thanks to the widespread distribution of vaccines worldwide, global oil and gas consumption recovered in 2021, and the company returned to high profitability that year.

Whitecap Resources reported first-quarter results on April 29th, 2026. For the period, petroleum and natural gas revenues increased to $1.49 billion from $687 million in the prior year. Funds flow was $748 million and capital spending totaled $493 million, which resulted in free funds flow of $254 million.

Net income of $16 million, or $0.01 per share, compared unfavorably to $119 million, or $0.20 per share, in the same period of 2025.

Operational activity remained high for the period, with peak utilization of 18 drilling rigs. This resulted in the drilling of 31 unconventional wells and 54 conventional wells. The company had realized losses of nearly $15 million on commodity contracts.

We project that Whitecap Resources will generate earnings-per-share of $1.00 for 2026, which would represent an improvement of 39% from 2025.

Growth Prospects

Whitecap Resources’ proved reserve lifetime is 16 years, which is above the industry’s average of about 10 years. In addition, thanks to the favorable characteristics of its development areas, Whitecap Resources is rapidly growing its reserve base.

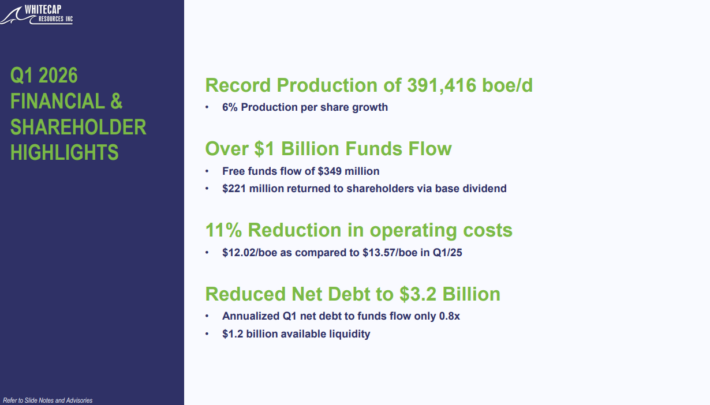

The company’s production growth rate has bene high in recent years, including 6% last quarter.

Source: Investor Presentation

This is extremely rare in the oil and gas industry. In fact, some oil majors have failed to grow their output for several years in a row. This is a key difference between Whitecap Resources and most oil and gas producers.

On the other hand, Whitecap Resources is sensitive to the cycles of the oil and gas industry. This is clearly reflected in the company’s volatile performance record. Over the last 10 years, Whitecap Resources has grown its earnings-per-share by an average annual rate of 7.7%, but this growth rate turns negative to nearly -16% over the past five years.

Whitecap Resources currently enjoys strong business momentum, not only due to its high production growth but also because of the Ukrainian crisis and the closing of the Strait of Hormuz due to the conflict in the Middle East. This has led to higher energy prices. As a result, Whitecap Resources is likely to continue thriving this year.

Given the positive business momentum, the cyclical nature of Whitecap Resources’ business, and the expected surge in results for this year, we project EPS will decline by 3% annually over the next five years.

Dividend & Valuation Analysis

Whitecap Resources is currently offering an above-average dividend yield of 4.7%, more than four times the yield of the S&P 500. The stock is thus an exciting candidate for income-oriented investors, but the latter should be aware that the dividend is not safe due to the cyclical nature of the oil and gas industry.

Whitecap Resources currently has a reasonable expected payout ratio of 54% for 2026 and a solid balance sheet, with a long-term debt-to-equity ratio of 0.34. As a result, the stock’s dividend has a margin of safety for the foreseeable future.

On the other hand, due to Whitecap Resources’ cyclical business, its dividend is not entirely safe. Additionally, U.S. investors should be aware that the dividend received from this stock is dependent on the exchange rate between the Canadian dollar and the U.S. dollar.

In reference to the valuation, Whitecap Resources is trading at 11.5 times times our earnings-per-share estimate for the year. We assume a fair price-to-earnings ratio of 8.0 for the stock. Therefore, the current earnings multiple is higher than our assumed fair price-to-earnings ratio. This means that multiple compression could reduce annual returns by 7% over the next five years if shares were to revert to our target P/E.

We project that Whitecap Resources will have a total annual return of -3.4% through 2031. This forecast is driven by the starting dividend yield, offset by negative EPS growth and a high single-digit headwind from multiple contraction.

Whitecap Resources earns a sell recommendation due to the negative total return estimate and a lack of dividend growth over the years

Final Thoughts

Whitecap Resources has decent prospects for growing its production and reserves than most of its peers and is offering an above-average dividend yield of almost 5%. Thanks to its healthy balance sheet, the company is not likely to cut its dividend in the near future, which is expected to entice some income-oriented investors.

However, the company’s performance record has been highly volatile due to its business cycles. Therefore, investors should wait for a more attractive entry point.

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

")

-1024x683.jpg "Strait Outta Hormuz: Getting the Iran Oil Story Straight")

{kind=link}