Published on April 21st, 2026 by Bob Ciura

Dividend growth is a powerful signal of a company’s financial health, and commitment to long-term value creation.

Dividend growth stocks have historically generated superior returns with less volatility relative to stocks with flat dividends, stocks that reduce their dividend, and stocks that don’t pay dividends

The above fact should not be overlooked.

It’s especially rare to find an investing factor that has historically offered – and I believe is likely to continue offering – both superior returns and lower volatility.

And it stands to reason that dividend growth stocks would provide both stronger returns and lower volatility versus non-dividend growth stocks.

That’s where the Dividend Champions come in.

The Dividend Champions have increased their dividends for over 25 consecutive years. With this in mind, we created a downloadable list of over 130 Dividend Champions.

You can download your free copy of the Dividend Champions list, along with relevant financial metrics like price-to-earnings ratios, dividend yields, and payout ratios, by clicking on the link below:

Since dividends are paid with actual cash, they can’t be faked.

A company cannot pay dividends for any meaningful length of time without generating cash to support the dividend.

Of course, not all dividend growth stocks make equally good investments.

This article will list the 10 Dividend Champions with the highest expected dividend growth over the next five years.

Table of Contents

You can instantly jump to any specific section of the article by clicking on the links below:

Best Dividend Growth Stock #10: Automatic Data Processing (ADP)

Expected Annual Dividend Growth Rate: 9.0%

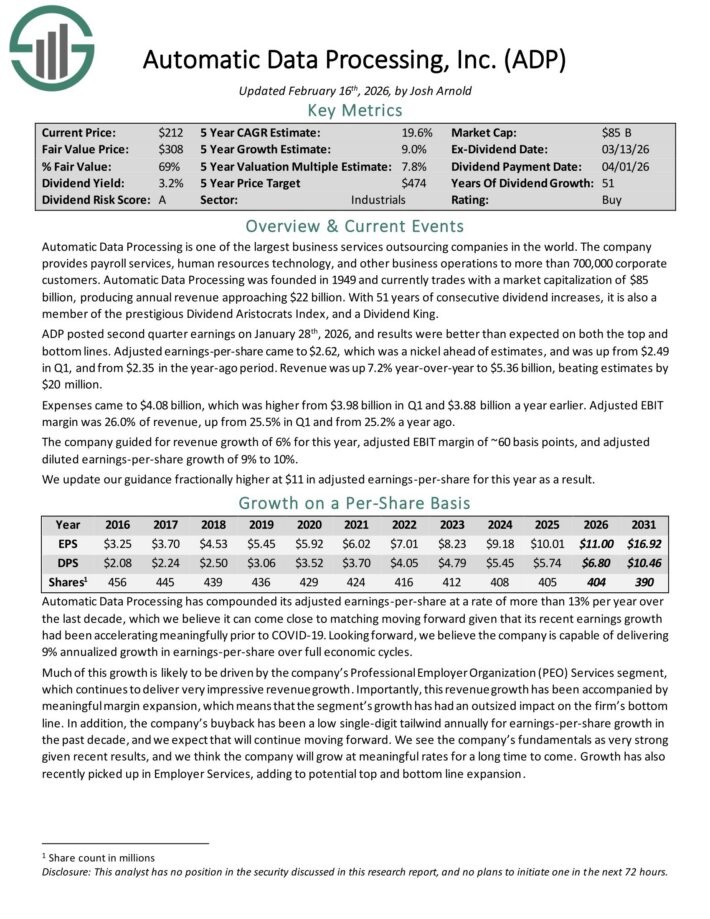

Automatic Data Processing is one of the largest business services outsourcing companies in the world. The company provides payroll services, human resources technology, and other business operations to more than 700,000 corporate customers.

ADP posted second quarter earnings on January 28th, 2026, and results were better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to $2.62, which was a nickel ahead of estimates, and was up from $2.49 in Q1, and from $2.35 in the year-ago period. Revenue was up 7.2% year-over-year to $5.36 billion, beating estimates by $20 million.

Expenses came to $4.08 billion, which was higher from $3.98 billion in Q1 and $3.88 billion a year earlier. Adjusted EBIT margin was 26.0% of revenue, up from 25.5% in Q1 and from 25.2% a year ago.

For 2026, ADP guided for revenue growth of 6%, adjusted EBIT margin of ~60 basis points, and adjusted diluted earnings-per-share growth of 9% to 10%.

Click here to download our most recent Sure Analysis report on ADP (preview of page 1 of 3 shown below):

Best Dividend Growth Stock #9: Brown & Brown (BRO)

Expected Annual Dividend Growth Rate: 9.1%

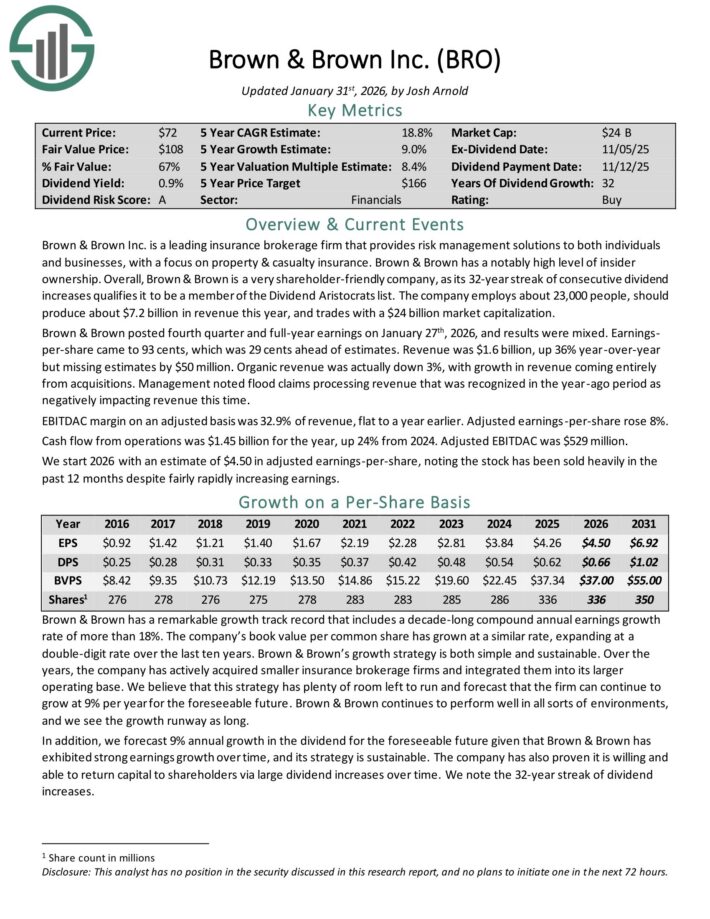

Brown & Brown Inc. is a leading insurance brokerage firm that provides risk management solutions to both individuals and businesses, with a focus on property & casualty insurance. Brown & Brown has a notably high level of insider ownership.

Brown & Brown posted fourth quarter and full-year earnings on January 27th, 2026, and results were mixed. Earnings-per-share came to 93 cents, which was 29 cents ahead of estimates.

Revenue was $1.6 billion, up 36% year-over-year but missing estimates by $50 million. Organic revenue was actually down 3%, with growth in revenue coming entirely from acquisitions.

Management noted flood claims processing revenue that was recognized in the year-ago period as negatively impacting revenue this time.

EBITDAC margin on an adjusted basis was 32.9% of revenue, flat to a year earlier. Adjusted earnings-per-share rose 8%.

Cash flow from operations was $1.45 billion for the year, up 24% from 2024. Adjusted EBITDAC was $529 million.

For 2026, we anticipate EPS of $4.50.

Click here to download our most recent Sure Analysis report on BRO (preview of page 1 of 3 shown below):

Best Dividend Growth Stock #8: Sherwin-Williams (SHW)

Expected Annual Dividend Growth Rate: 9.9%

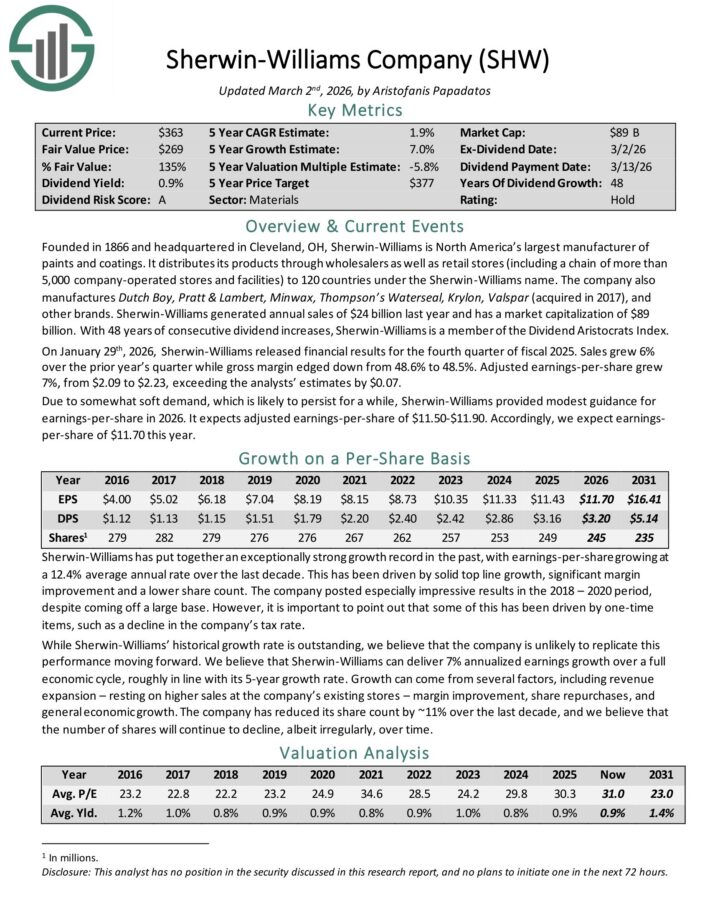

Sherwin-Williams is North America’s largest manufacturer of paints and coatings.

It distributes its products through wholesalers as well as retail stores (including a chain of more than 5,000 company-operated stores and facilities) to 120 countries under the Sherwin-Williams name.

The company also manufactures Dutch Boy, Pratt & Lambert, Minwax, Thompson’s Waterseal, Krylon, Valspar (acquired in 2017), and other brands.

Sherwin-Williams generated annual sales of $24 billion last year. With 48 years of consecutive dividend increases, it is a member of the Dividend Aristocrats.

On January 29th, 2026, Sherwin-Williams released financial results for the fourth quarter of fiscal 2025. Sales grew 6% over the prior year’s quarter while gross margin edged down from 48.6% to 48.5%.

Adjusted earnings-per-share grew 7%, from $2.09 to $2.23, exceeding the analysts’ estimates by $0.07.

Due to somewhat soft demand, which is likely to persist for a while, Sherwin-Williams provided modest guidance for earnings-per-share in 2026.

It expects adjusted earnings-per-share of $11.50-$11.90. Accordingly, we expect earnings-per-share of $11.70 this year.

Click here to download our most recent Sure Analysis report on SHW (preview of page 1 of 3 shown below):

Best Dividend Growth Stock #7: Nordson Corp. (NDSN)

Expected Annual Dividend Growth Rate: 10.0%

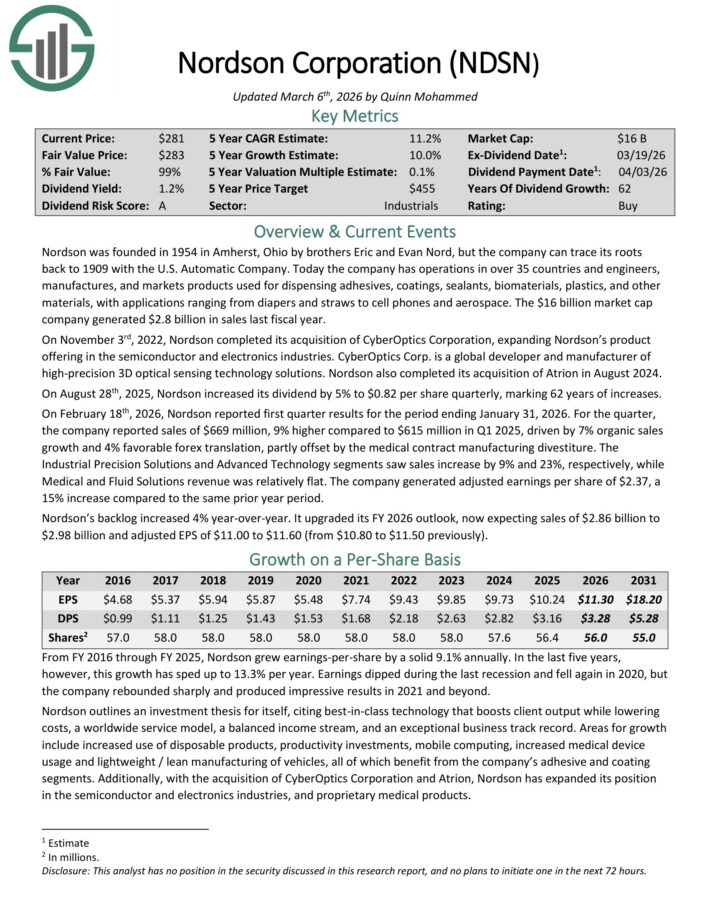

Nordson has operations in over 35 countries and manufactures products used for dispensing adhesives, coatings, sealants, biomaterials, plastics, and other materials.

Applications range from diapers and straws, to cell phones and aerospace. The company generated $2.8 billion in sales last fiscal year.

On August 28th, 2025, Nordson increased its dividend by 5% to $0.82 per share quarterly, marking 62 years of increases.

On February 18th, 2026, Nordson reported first quarter results. For the quarter, the company reported sales of $669 million, 9% higher compared to $615 million in Q1 2025.

Growth was driven by 7% organic sales growth and 4% favorable forex translation, partly offset by the medical contract manufacturing divestiture.

The Industrial Precision Solutions and Advanced Technology segments saw sales increase by 9% and 23%, respectively, while Medical and Fluid Solutions revenue was relatively flat.

The company generated adjusted earnings per share of $2.37, a 15% increase compared to the same prior year period.

Nordson’s backlog increased 4% year-over-year. It upgraded its FY 2026 outlook, now expecting sales of $2.86 billion to $2.98 billion and adjusted EPS of $11.00 to $11.60.

Click here to download our most recent Sure Analysis report on NDSN (preview of page 1 of 3 shown below):

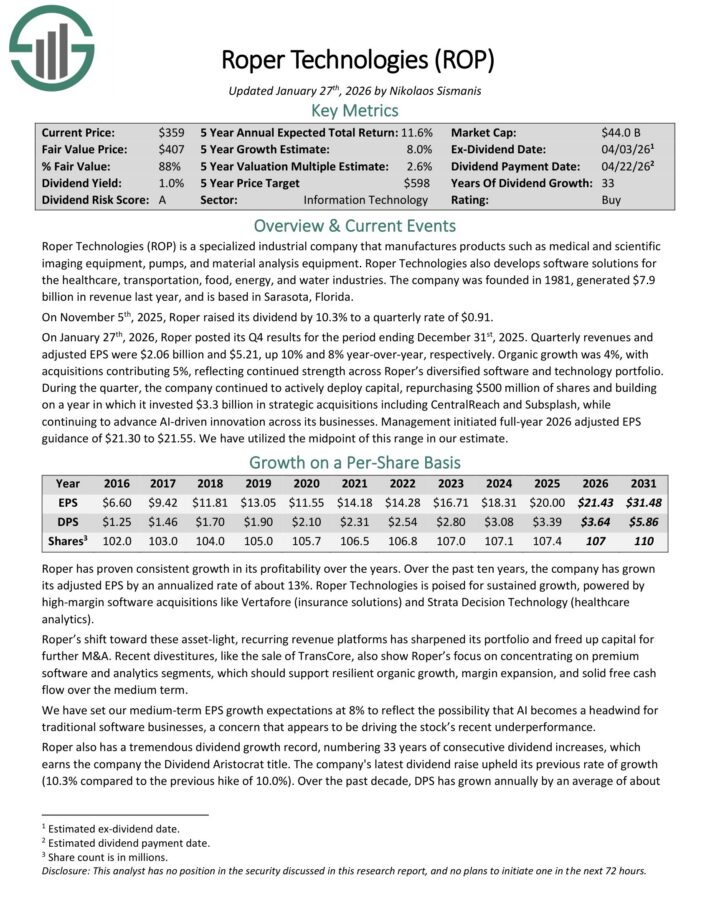

Best Dividend Growth Stock #6: Roper Technologies (ROP)

Expected Annual Dividend Growth Rate: 10.0%

Roper Technologies is a specialized industrial company that manufactures products such as medical and scientific imaging equipment, pumps, and material analysis equipment.

The company also develops software solutions for the healthcare, transportation, food, energy, and water industries. It generated $7.9 billion in revenue last year, and is based in Sarasota, Florida.

On November 5th, 2025, Roper raised its dividend by 10.3% to a quarterly rate of $0.91. The company has increased its dividend for 33 consecutive years.

On January 27th, 2026, Roper posted its Q4 results. Quarterly revenue and adjusted EPS were $2.06 billion and $5.21, up 10% and 8% year-over-year, respectively.

Organic growth was 4%, with acquisitions contributing 5%, reflecting continued strength across Roper’s diversified software and technology portfolio.

During the quarter, the company continued to actively deploy capital, repurchasing $500 million of shares and building on a year in which it invested $3.3 billion in strategic acquisitions including CentralReach and Subsplash, while continuing to advance AI-driven innovation across its businesses.

Management initiated full-year 2026 adjusted EPS guidance of $21.30 to $21.55.

Click here to download our most recent Sure Analysis report on ROP (preview of page 1 of 3 shown below):

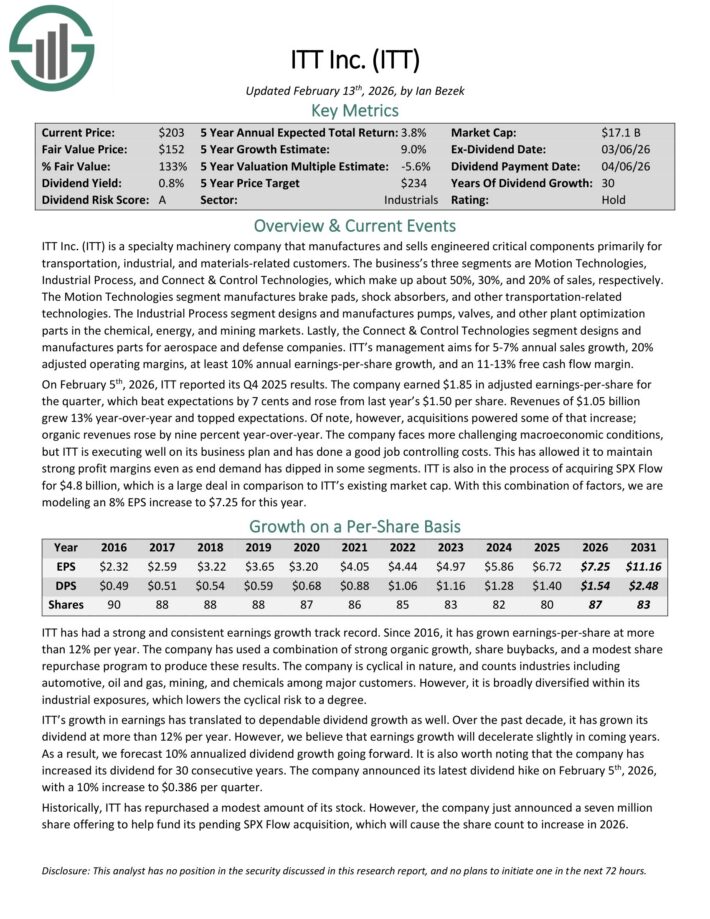

Best Dividend Growth Stock #5: ITT Inc. (ITT)

Expected Annual Dividend Growth Rate: 10.0%

ITT is a specialty machinery company that manufactures and sells engineered critical components primarily for transportation, industrial, and materials-related customers.

The business’s three segments are Motion Technologies, Industrial Process, and Connect & Control Technologies, which make up about 50%, 30%, and 20% of sales, respectively.

The Motion Technologies segment manufactures brake pads, shock absorbers, and other transportation-related technologies.

The Industrial Process segment designs and manufactures pumps, valves, and other plant optimization parts in the chemical, energy, and mining markets.

Lastly, the Connect & Control Technologies segment designs and manufactures parts for aerospace and defense companies.

ITT’s management aims for 5-7% annual sales growth, 20% adjusted operating margins, at least 10% annual earnings-per-share growth, and an 11-13% free cash flow margin.

On February 5th, 2026, ITT reported its Q4 2025 results. The company earned $1.85 in adjusted earnings-per-share for the quarter, which beat expectations by 7 cents and rose from last year’s $1.50 per share.

Revenue of $1.05 billion grew 13% year-over-year and topped expectations. Of note, however, acquisitions powered some of that increase; organic revenues rose by 9% year-over-year.

ITT is also in the process of acquiring SPX Flow for $4.8 billion, which is a large deal in comparison to ITT’s existing market cap.

With this combination of factors, we are modeling an 8% EPS increase to $7.25 for 2026.

Click here to download our most recent Sure Analysis report on ITT (preview of page 1 of 3 shown below):

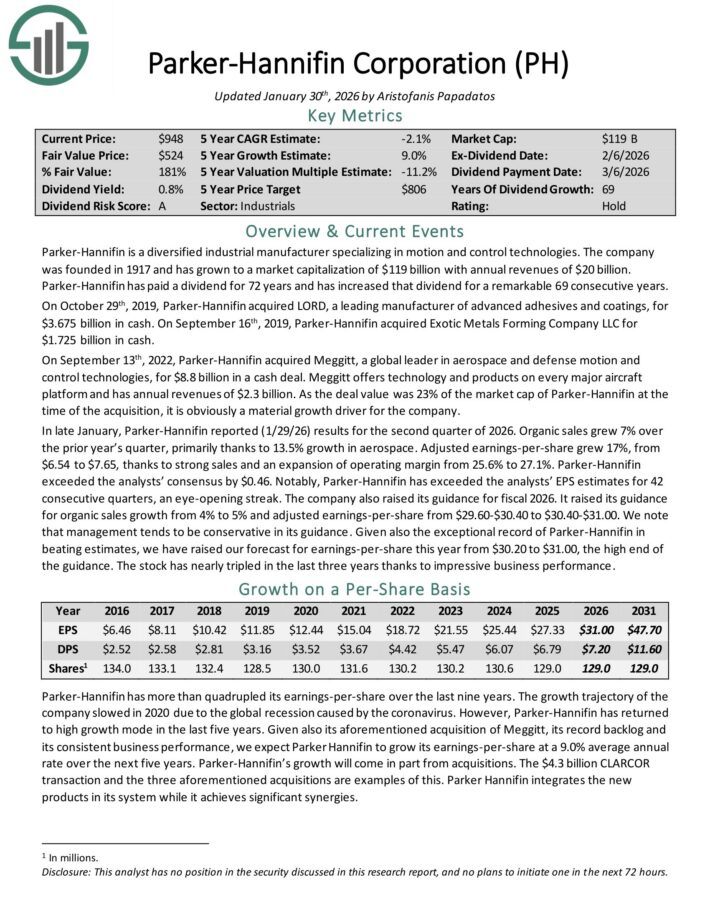

Best Dividend Growth Stock #4: Parker-Hannifin Corp. (PH)

Expected Annual Dividend Growth Rate: 10.0%

Parker-Hannifin is a diversified industrial manufacturer specializing in motion and control technologies.

The company was founded in 1917 and has grown to generate annual revenue of $20 billion.

Parker-Hannifin has paid a dividend for 72 years and has increased that dividend for a remarkable 69 consecutive years.

In late January, Parker-Hannifin reported (1/29/26) results for the second quarter of 2026. Organic sales grew 7% over the prior year’s quarter, primarily thanks to 13.5% growth in aerospace.

Adjusted earnings-per-share grew 17%, from $6.54 to $7.65, thanks to strong sales and an expansion of operating margin from 25.6% to 27.1%.

Parker-Hannifin exceeded the analysts’ consensus by $0.46.

The company also raised its guidance for fiscal 2026. It now expects organic sales growth of 4% to 5% and adjusted earnings-per-share from $29.60-$30.40 to $30.40-$31.00.

Parker-Hannifin has more than quadrupled its earnings-per-share over the last nine years. Given its acquisition of Meggitt, its record backlog and its consistent business performance, we expect Parker Hannifin to grow its earnings-per-share at a 9.0% average annual rate over the next five years.

We expect annual dividend growth of 10% per year going forward.

Click here to download our most recent Sure Analysis report on PH (preview of page 1 of 3 shown below):

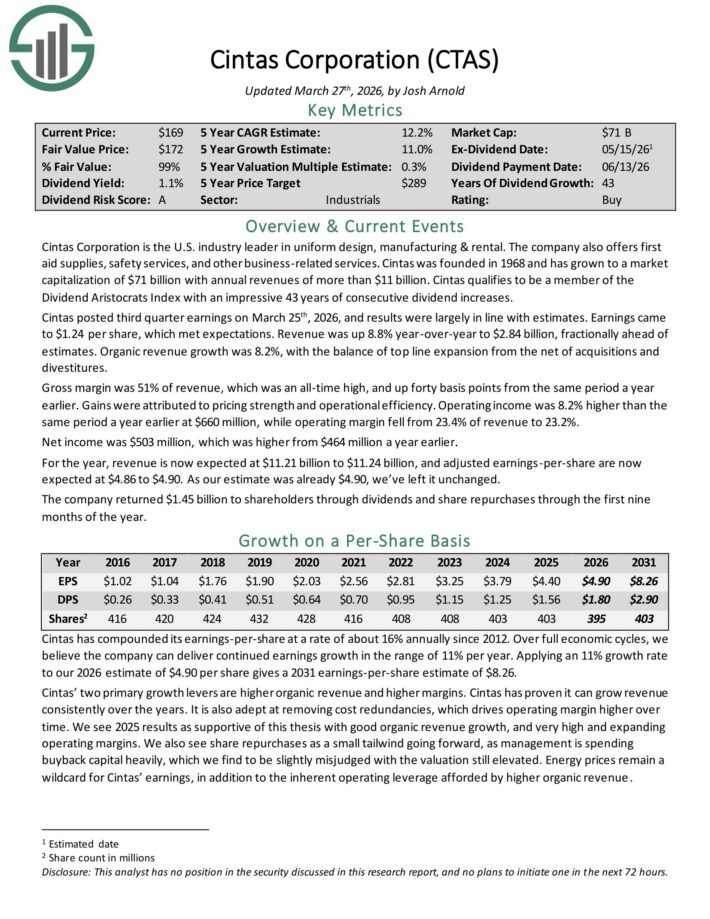

Best Dividend Growth Stock #3: Cintas Corporation (CTAS)

Expected Annual Dividend Growth Rate: 10.0%

Cintas Corporation is the U.S. industry leader in uniform design, manufacturing & rental. The company also offers first aid supplies, safety services, and other business-related services.

Cintas qualifies to be a member of the Dividend Aristocrats Index with an impressive 43 years of consecutive dividend increases.

Cintas posted third quarter earnings on March 25th, 2026. Earnings came to $1.24 per share, which met expectations. Revenue was up 8.8% year-over-year to $2.84 billion, fractionally ahead of estimates.

Organic revenue growth was 8.2%, with the balance of top line expansion from the net of acquisitions and divestitures.

Gross margin was 51% of revenue, which was an all-time high, and up forty basis points from the same period a year earlier.

Operating income was 8.2% higher than the same period a year earlier at $660 million, while operating margin fell from 23.4% of revenue to 23.2%.

Net income was $503 million, which was higher from $464 million a year earlier.

For 2026, revenue is now expected at $11.21 billion to $11.24 billion, and adjusted earnings-per-share are now expected at $4.86 to $4.90.

Click here to download our most recent Sure Analysis report on CTAS (preview of page 1 of 3 shown below):

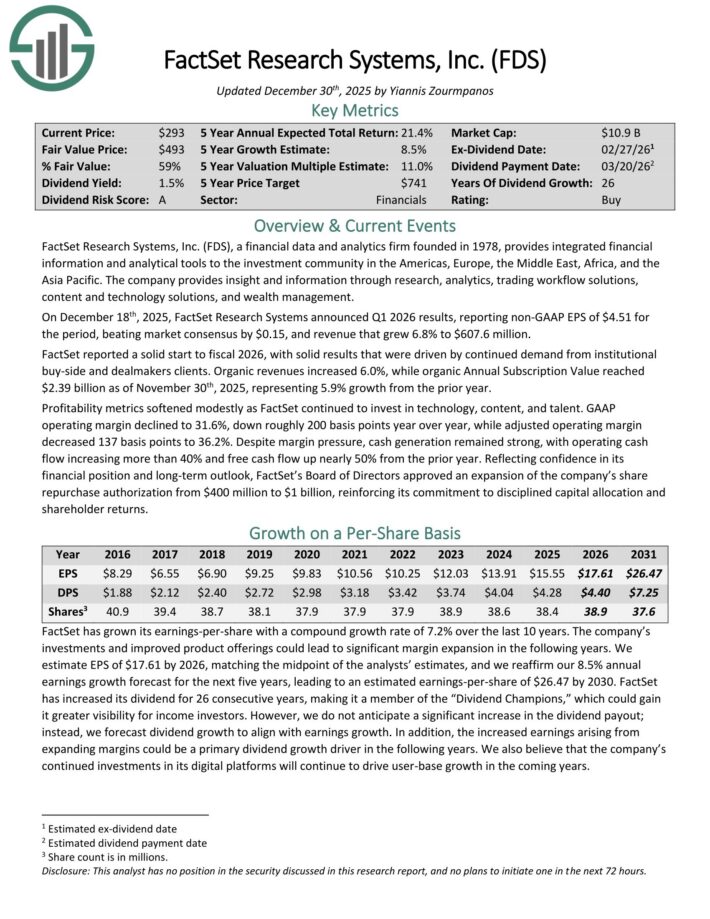

Best Dividend Growth Stock #2: Factset Research Systems (FDS)

Expected Annual Dividend Growth Rate: 10.5%

FactSet Research Systems, a financial data and analytics firm founded in 1978, provides integrated financial information and analytical tools to the investment community in the Americas, Europe, the Middle East, Africa, and Asia-Pacific.

The company provides insight and information through research, analytics, trading workflow solutions, content and technology solutions, and wealth management.

On December 18th, 2025, FactSet Research Systems announced Q1 2026 results, reporting non-GAAP EPS of $4.51 for the period, beating market consensus by $0.15, and revenue that grew 6.8% to $607.6 million.

FactSet reported a solid start to fiscal 2026, with solid results that were driven by continued demand from institutional buy-side and dealmakers clients.

Organic revenues increased 6.0%, while organic Annual Subscription Value reached $2.39 billion as of November 30th, 2025, representing 5.9% growth from the prior year.

Profitability metrics softened modestly as FactSet continued to invest in technology, content, and talent. GAAP operating margin declined to 31.6%, down roughly 200 basis points year over year, while adjusted operating margin decreased 137 basis points to 36.2%.

Despite margin pressure, cash generation remained strong, with operating cash flow increasing more than 40% and free cash flow up nearly 50% from the prior year.

Reflecting confidence in its financial position and long-term outlook, FactSet’s Board of Directors approved an expansion of the company’s share repurchase authorization from $400 million to $1 billion.

Click here to download our most recent Sure Analysis report on FDS (preview of page 1 of 3 shown below):

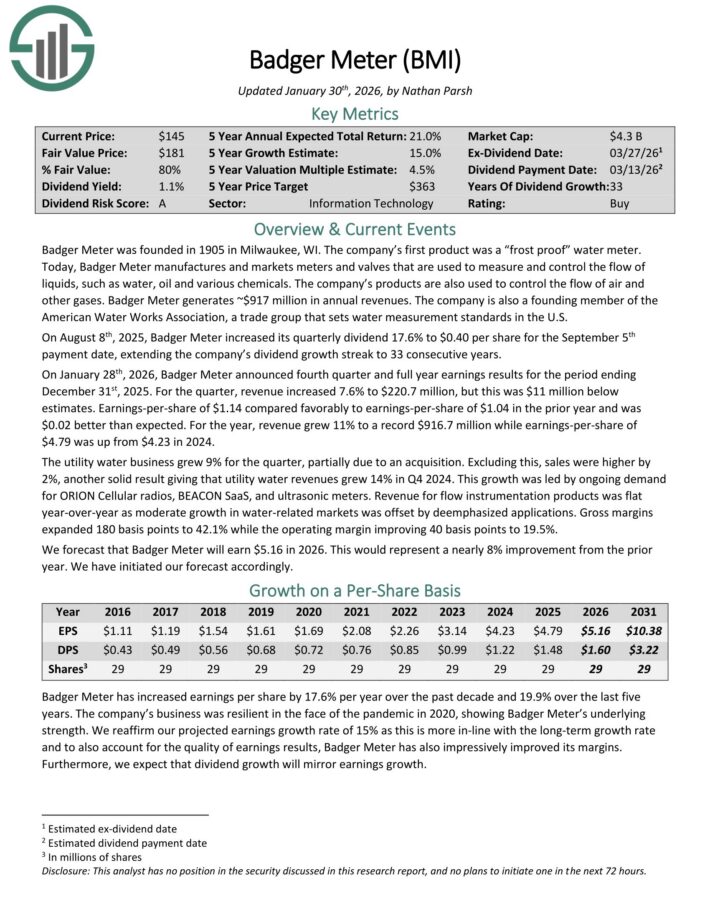

Best Dividend Growth Stock #1: Badger Meter Inc. (BMI)

Expected Annual Dividend Growth Rate: 15.0%

Badger Meter manufactures and markets meters and valves that are used to measure and control the flow of liquids, such as water, oil and various chemicals.

The company’s products are also used to control the flow of air and other gases. Badger Meter generates ~$917 million in annual revenues.

On January 28th, 2026, Badger Meter announced fourth quarter and full year earnings results. For the quarter, revenue increased 7.6% to $220.7 million, but this was $11 million below estimates.

Earnings-per-share of $1.14 compared favorably to earnings-per-share of $1.04 in the prior year and was $0.02 better than expected. For the year, revenue grew 11% to a record $916.7 million while earnings-per-share of $4.79 was up from $4.23 in 2024.

The utility water business grew 9% for the quarter, partially due to an acquisition. Excluding this, sales were higher by 2%, another solid result giving that utility water revenues grew 14% in Q4 2024. This growth was led by ongoing demand for ORION Cellular radios, BEACON SaaS, and ultrasonic meters.

Revenue for flow instrumentation products was flat year-over-year as moderate growth in water-related markets was offset by deemphasized applications.

Click here to download our most recent Sure Analysis report on BMI (preview of page 1 of 3 shown below):

Additional Reading

The Dividend Champions list is not the only way to quickly screen for stocks that regularly pay rising dividends.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

{kind=link}