Robinhood Banking is Robinhood’s biggest push yet beyond stock trading — a full checking-and-savings experience that pays up to 4% APY, delivers physical cash to your door, and wraps your deposits in up to $2.5 million of FDIC coverage. Announced in early 2025 and rolling out through 2026, it’s designed to make your everyday cash work as hard as your investments.

But there’s a catch that trips up a lot of people: Robinhood isn’t a bank, and Robinhood Banking is only available to paying Robinhood Gold members. The accounts are held at an FDIC-insured partner bank, the best perks require a monthly direct deposit, and access is still rolling out by invitation. Whether it’s worth switching depends on how much cash you keep on hand and how deep you already are in the Robinhood ecosystem.

In this guide we’ll break down everything: the real APY, how the checking and savings accounts work, the headline-grabbing cash-delivery feature, the fees, who actually qualifies, and — most importantly — whether Robinhood Banking is safe. Robinhood unveiled the product alongside its wealth-management and AI tools in its official 2025 announcement, positioning it as a direct challenge to traditional banks.

Robinhood Banking — At a Glance

Details

Account Types

Checking & high-yield savings (individual, joint & kids’ accounts)

Savings APY

Up to 4.00% for Gold members (no cap, no minimum)

Monthly Fee

$0 account fee — but requires Robinhood Gold ($5/mo or $50/yr)

FDIC Coverage

Up to $2.5 million via partner-bank sweep network

Banking Partner

Coastal Community Bank, Member FDIC

Standout Feature

On-demand cash delivery to your door (fee & area limits apply)

Availability

Robinhood Gold members only — rolling out by invite

What Is Robinhood Banking?

Robinhood Banking is a set of full-featured deposit accounts — a checking account and a high-yield savings account — built directly into the Robinhood app. It’s offered through Robinhood Money, LLC, with the actual banking services and FDIC insurance provided by Coastal Community Bank, Member FDIC. In other words, Robinhood is the tech and interface; a chartered bank holds your money.

Robinhood first revealed Robinhood Banking in early 2025 at its “Lost City of Gold” event, alongside a wealth-management service (Robinhood Strategies) and an AI finance assistant (Robinhood Cortex). The banking product began rolling out to Gold members through late 2025 and into 2026. It’s aimed squarely at the “primary checking account” relationship that traditional banks like Chase and Bank of America have long owned — and it’s using a high APY, generous FDIC coverage, and some genuinely novel perks to pry customers away.

Unlike the older High-Yield Cash sweep program (which pays interest on uninvested brokerage cash), Robinhood Banking is a standalone banking relationship with a debit card, routing and account numbers, direct deposit, joint accounts, and even accounts for kids. If you’re new to the platform, our full Robinhood review covers how the brokerage side works.

Robinhood Banking APY: How Much You’ll Earn

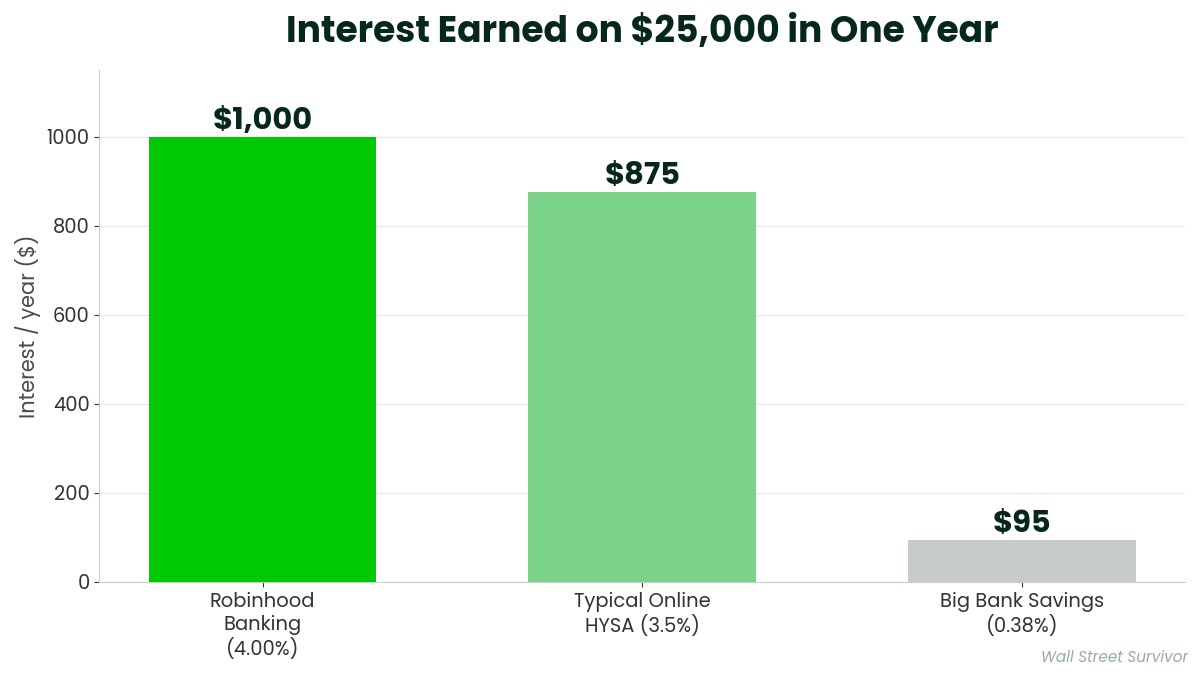

The headline number is the APY, and it’s aggressive. Robinhood Banking savings pays up to 4.00% APY for Gold members — several times the national savings average of roughly 0.38%. There’s no cap and no minimum balance to earn the rate, which is unusual; many “high-yield” accounts throttle the top rate above a certain balance.

A few important nuances on the rate:

The rate is variable. Like every high-yield account, the APY floats with the broader interest-rate environment and can change at any time.

Gold membership is required to earn the top rate. Drop Gold and the rate drops too.

Promotional boosts appear periodically. Robinhood has run limited-time APY-boost offers for new savings accounts, which can lift the first-year composite yield even higher.

To put the rate in perspective, here’s what $25,000 in savings earns in a year at a few common APYs:

Account

APY

Interest on $25,000/yr

Robinhood Banking (Gold)4.00%~$1,000

Typical online HYSA~3.5%~$875

Big-bank savings (national avg.)0.38%~$95

Even after subtracting the $50/year Gold membership, a saver with a healthy balance comes out well ahead of a traditional big-bank account. The math only breaks down if you keep very little cash on hand — in which case the Gold fee eats up most of the interest advantage.

Robinhood Banking Features & Perks

Beyond the APY, Robinhood Banking is loaded with features you don’t normally see bundled together — some practical, some almost theatrical.

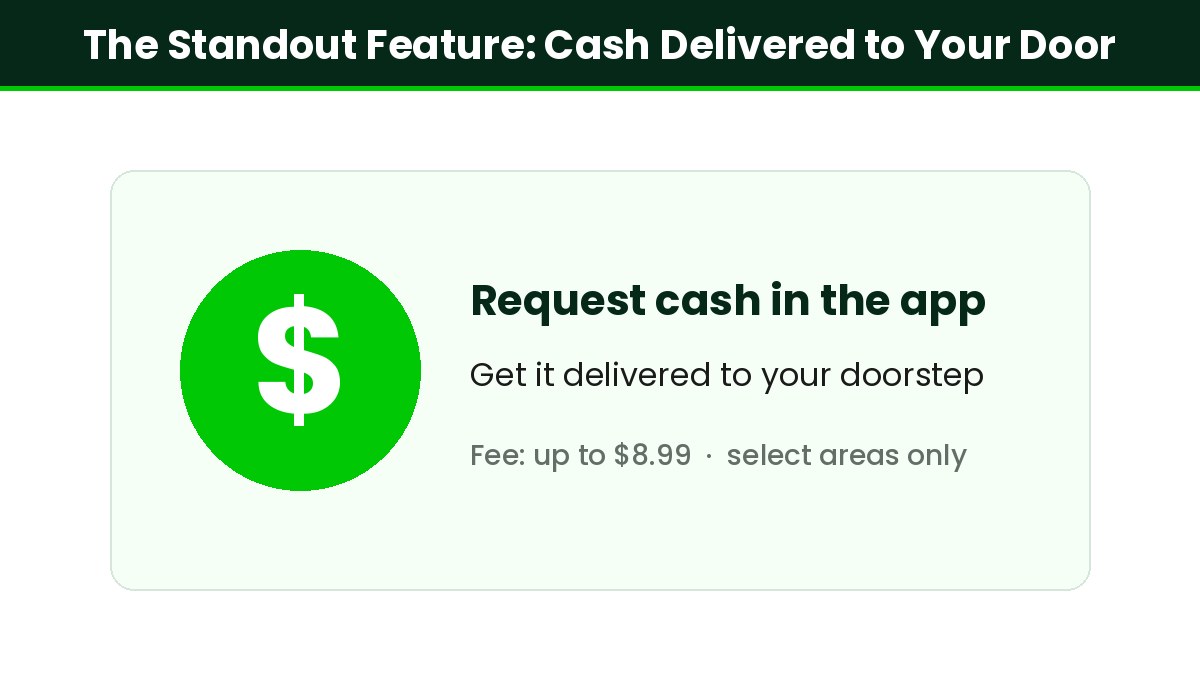

1. Cash Delivered to Your Door

The most talked-about feature: on-demand physical cash delivery. Instead of hunting for an ATM, you can request cash in the app and have it delivered to your door. Availability depends on your location, and the service carries a fee (up to about $8.99 per delivery). It’s a gimmick for some and a genuine convenience for others — but it’s exactly the kind of headline feature that gets people talking about a new bank.

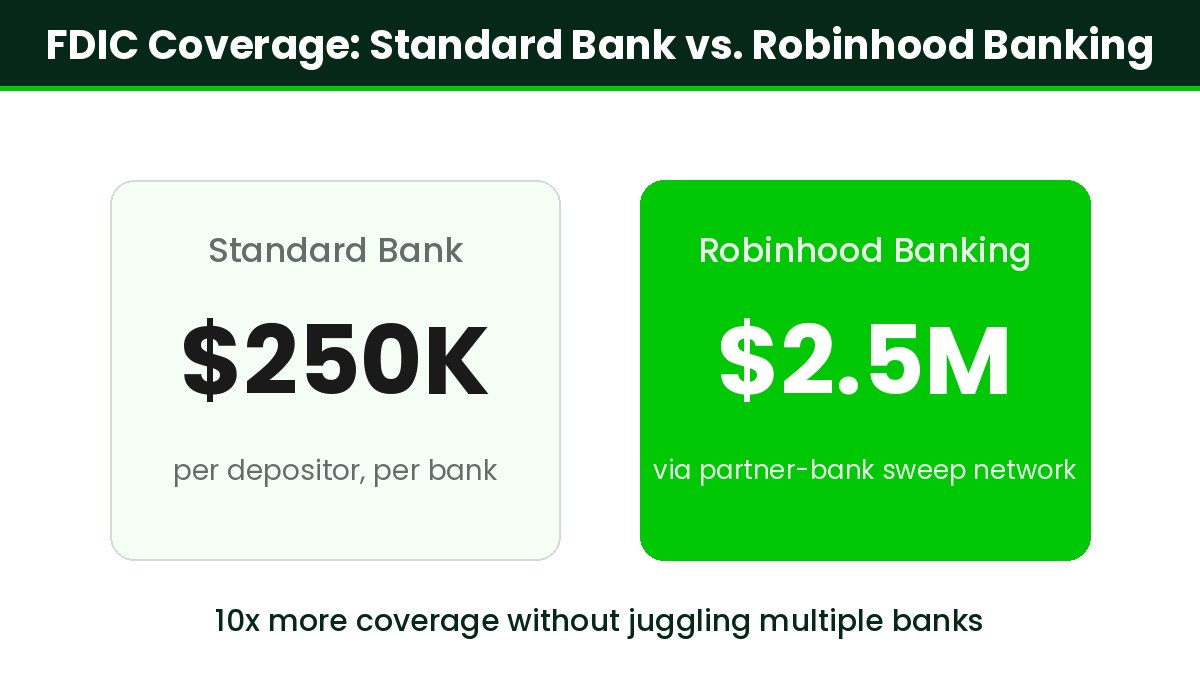

2. Up to $2.5 Million in FDIC Coverage

Standard FDIC insurance covers $250,000 per depositor, per bank. Robinhood Banking uses a sweep network of partner banks to spread your deposits across multiple institutions, extending coverage up to $2.5 million. That’s a serious selling point for anyone holding large cash balances who would otherwise have to open accounts at ten different banks to stay insured.

3. Checking, Joint & Kids’ Accounts

Robinhood Banking supports individual, joint, and children’s accounts, plus a debit card, direct deposit, and standard bill-pay and transfer functions. The ability to open family and kids’ accounts moves Robinhood from a solo-investor app toward a household banking hub.

4. Private Banking & Luxury Perks

For higher-balance customers, Robinhood has teased a private banking tier with estate planning, tax advice, and eyebrow-raising luxury perks — think access to private jet travel, global chauffeurs, and helicopter rides. These are aimed at the wealth-management end of the market and won’t apply to most users, but they signal Robinhood’s ambition to compete with private banks, not just online savings apps.

5. Bonus Perks for Gold Members

Because Robinhood Banking is bundled into Gold, members also get the wider Gold benefit stack: a boost on IRA contributions, higher interest on brokerage cash, and access to the Robinhood Gold Card with 3% cash back. The banking accounts are really one piece of a larger membership.

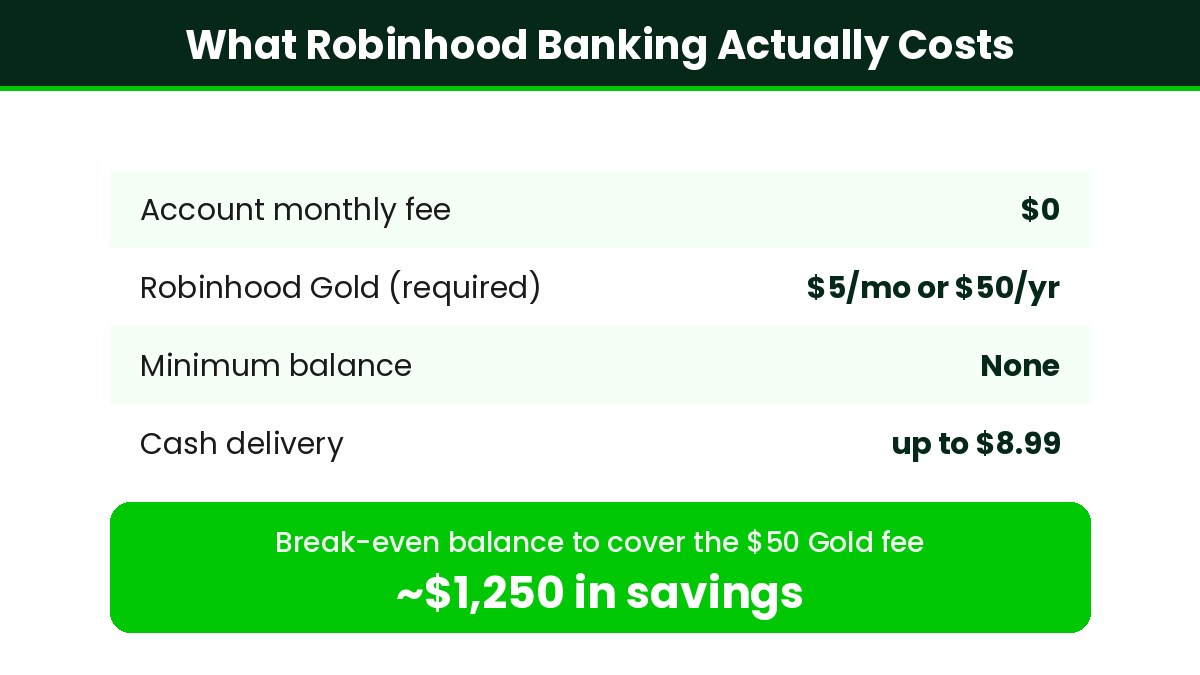

Robinhood Banking Cost: What You’ll Actually Pay

The accounts themselves have no monthly maintenance fee, but you can’t get Robinhood Banking without a Robinhood Gold subscription. Here’s the real cost breakdown:

Cost Component

Amount

Account monthly fee$0

Robinhood Gold (required)$5/month or $50/year

Minimum balanceNone

Cash deliveryUp to ~$8.99 per delivery

Effective annual cost$50–$60 (Gold)

At 4% APY, you only need to keep about $1,250 in savings to earn back the $50 annual Gold fee ($50 ÷ 4% = $1,250). Above that, the membership pays for itself and the rest is upside. If you’d already pay for Gold for the brokerage perks or the Gold Card, the banking accounts are effectively free. Want to see if Gold makes sense overall? Read Is Robinhood Gold Worth It?

Is Robinhood Banking Safe?

This is the question that stops most people, and the honest answer is: your deposits are protected, but understand how.

Robinhood itself is not a bank. Robinhood Banking is offered by Robinhood Money, LLC, a fintech company. Your money is actually held at Coastal Community Bank, Member FDIC, and swept across a network of partner banks. FDIC insurance applies as pass-through coverage at those insured banks (up to $2.5 million total), provided the program’s conditions are met. So the underlying dollars sit in FDIC-insured institutions — but the protection flows through the partner banks, not from Robinhood directly.

Key distinction: FDIC insurance protects you if the partner bank fails — it does not protect against investment losses or against a fintech operational failure. This is the same pass-through model used by most modern neobanks.

For a deeper look at how Robinhood’s insurance and account protections work across its brokerage and cash products, see our overview of whether Robinhood is safe. Bottom line: Robinhood Banking is as safe as other reputable neobanks, as long as you keep balances within the insured limits and treat it as a pass-through fintech account rather than a chartered bank.

Robinhood Banking vs. Traditional & Online Banks

Feature

Robinhood Banking

Typical Online Bank

Big Traditional Bank

Savings APYUp to 4.00%~3.5%~0.38%

FDIC coverageUp to $2.5M (sweep)$250K$250K

Monthly cost$5 Gold (or $50/yr)$0$0–$25

Cash deliveryYes (fee)NoBranch/ATM only

Physical branchesNoNoYes

The trade-off is clear: Robinhood Banking wins on yield, insured limits, and novelty, but you pay for Gold and there are no branches. If you value in-person service or want a truly free account, a standalone online HYSA or a big bank may fit better. If you keep meaningful cash and are already paying for Gold, Robinhood is hard to beat.

How to Get Robinhood Banking

Open a Robinhood account. Free and takes about 10 minutes. If you don’t have one yet, sign up here.

Subscribe to Robinhood Gold ($5/month or $50/year). New users typically get the first 30 days free.

Join the Robinhood Banking waitlist from inside the app. Access is rolling out by invitation, so timing varies.

Open your checking and/or savings account when you’re invited, then set up direct deposit to unlock the best perks.

Order your debit card and start earning up to 4% APY on your savings.

Robinhood Banking: Pros & Cons

Pros

Cons

✅ Up to 4% APY with no cap or minimum✅ Up to $2.5M FDIC coverage via sweep✅ Cash delivered to your door✅ Checking, joint & kids’ accounts✅ Integrated with investing & the Gold Card✅ No monthly account fee

❌ Requires paid Robinhood Gold membership❌ Robinhood is not itself a bank (pass-through FDIC)❌ No physical branches❌ Invite-only rollout❌ Best perks require monthly direct deposit❌ APY is variable and can change

Is Robinhood Banking Worth It?

Robinhood Banking is worth it if most of the following are true:

You keep at least a few thousand dollars in cash (enough to clear the Gold fee and then some)

You already pay for Robinhood Gold, or want its wider perks

You want high FDIC coverage without juggling multiple banks

You’re comfortable with a branchless, app-first bank

It’s not worth it if you keep very little cash (the Gold fee erodes your interest), you want a completely free account with no membership, or you rely on in-person branch service. In those cases, a standalone high-yield savings account will get you a comparable rate with no subscription attached.

Frequently Asked Questions

No. Robinhood is a financial technology company, not a bank. Robinhood Banking is offered through Robinhood Money, LLC, and the actual banking services and FDIC insurance are provided by Coastal Community Bank, Member FDIC, along with a network of partner banks.

Robinhood Banking savings pays up to 4.00% APY for Robinhood Gold members, with no cap and no minimum balance. The rate is variable and can change with market conditions. Promotional boosts for new accounts can temporarily raise the effective first-year yield.

Yes, through pass-through coverage. Deposits are held at Coastal Community Bank and swept across partner banks, extending FDIC insurance up to $2.5 million total. The coverage comes from the insured partner banks, not from Robinhood itself, and applies when the program’s conditions are met.

Yes. Robinhood Banking is available only to Robinhood Gold members, which costs $5/month or $50/year. If you cancel Gold, you lose access to the banking accounts and the top APY.

Yes. Robinhood Banking offers on-demand cash delivery in supported areas. You request cash in the app and it’s delivered to you, typically for a fee of up to about $8.99 per delivery. Availability depends on your location.

Open a Robinhood account, subscribe to Robinhood Gold, and join the Robinhood Banking waitlist inside the app. Access is rolling out by invitation, so wait times vary. Once invited, you can open checking and savings accounts and set up direct deposit.

It can be, if you keep enough cash to justify the Gold fee and value the extra FDIC coverage and features. A standalone high-yield savings account offers a similar rate with no membership required, so the best choice depends on your balance and whether you want Robinhood’s other perks.

The Bottom Line

Robinhood Banking is one of the most aggressive attempts yet by a fintech to become your primary bank. Up to 4% APY, up to $2.5 million in FDIC coverage, cash delivered to your door, and tight integration with investing and the Gold Card make it a genuinely compelling package — especially if you’re already paying for Robinhood Gold.

The caveats are just as important. Robinhood isn’t a bank, the best rate is locked behind a paid membership, and there are no branches if you need in-person help. For savers with real cash balances who live in the app already, Robinhood Banking is a strong upgrade over a big-bank checking account. For everyone else, a free standalone high-yield savings account may deliver most of the benefit without the subscription.

Either way, Robinhood Banking raises the bar for what a modern account should offer — and it’s putting real pressure on the legacy banks that have coasted on 0.38% savings rates for years.

-1024x683.jpg "Strait Outta Hormuz: Getting the Iran Oil Story Straight")

{kind=link}