Published on May 13th, 2026 by Nathan Parsh

Chartwell Retirement Residences (CWSRF) has two appealing investment characteristics:

#1: It is offering an above-average dividend yield of 3.0%, which is nearly triple the average dividend yield of the S&P 500.

#2: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yields and payout ratios) by clicking on the link below:

The combination of an above-average dividend yield and a monthly dividend makes Chartwell Retirement Residences an attractive option for individual investors.

But there’s more to the trust than just these factors. Keep reading this article to learn more about Chartwell Retirement Residences.

Business Overview

Chartwell Retirement Residences is the largest operator of retirement residences in Canada, with a portfolio of 143 properties and 26,494 suites across Ontario, Quebec, British Columbia, and Alberta. About 97% of suites are private pay.

Its operations are focused on independent supportive living (ISL), independent living (IL), and assisted living (AL) communities, with limited exposure to long-term care.

Chartwell Retirement Residences targets middle-to-upper income seniors in urban and suburban markets, offering hospitality-driven housing with optional care services.

The open-ended, real estate trust operates a vertically integrated model, including development, leasing, and property management, which helps maintain consistency and control across its national platform.

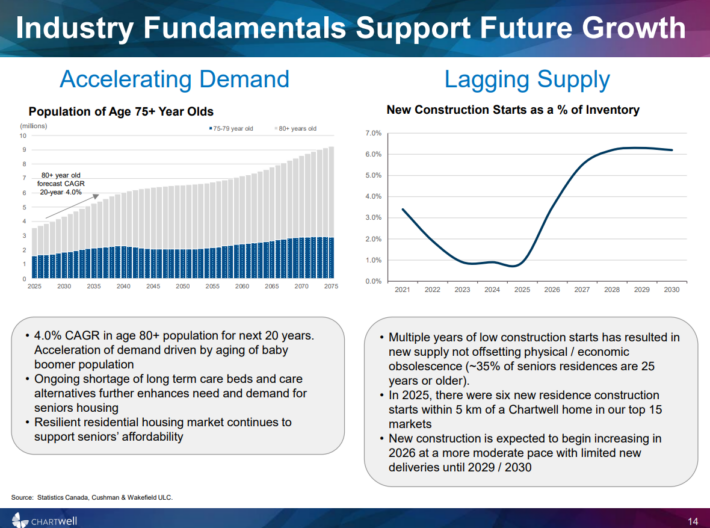

The business of Chartwell Retirement Residences is characterized by strong fundamentals, primarily thanks to an aging population.

Source: Investor Presentation

Housing demand for seniors is expected to double over the next 20 years. More than 200,000 new suites will be required to cover the growth of demand over the next decade. This is an excessive number of new suites, as more than 73,000 suites have been built over the last decade. About half of the current stock is more than 25 years old and recent construction has slowed.

Overall, the fundamentals of the business of Chartwell Retirement Residences appear highly favorable and may offer strong pricing power to the real estate trust.

In the first quarter of 2026, Chartwell Retirement Residences grew its revenue 24.4% over the prior year’s quarter thanks to higher occupancy, contributions from acquisitions, and solid same property performance. Funds from operations (FFO) surged 52.4% while FFO per share grew 33%, from $0.15 to $0.20.

While cost inflation took its toll on the operating margin of the trust, the solid improvement in occupancy and revenue more than offset this headwind. We expect the trust to grow its FFO per share 19% this year, from $0.69 to $0.82.

Growth Prospects

As mentioned above, the industry of Chartwell Retirement Residences has promising growth prospects over the long run thanks to an aging population. In addition, the trust is trying to achieve growth in many dimensions.

Source: Investor Presentation

It tries to grow its FFO per share by acquiring attractive properties and disposing those with low expected returns. It also develops and repositions some of its properties in order to enhance their returns.

However, investors should note that the trust has failed to grow its bottom line at a high rate over the last decade. Its FFO per share of $0.69 in 2025 was only 7.8% higher than its FFO per share of $0.64 in 2016. However, this lack of growth can at least partially be explained by a 65% increase in the share count over this period.

Chartwell Retirement Residences has been facing pressure in its business particularly in recent years due to high inflation, which has been exerting pressure on the operating margin of the trust.

Unfortunately, the pattern of promising industry fundamentals but weak business results has been observed in some U.S. REITs as well, such as Healthpeak Properties (DOC).

Therefore, we prefer to be conservative in our growth assumptions and assume FFO per share over growth of 1% annually for the next five years for Chartwell Retirement Residences.

Just like many real estate trusts, Chartwell Retirement Residences has a somewhat weak balance sheet. Due to the surge of interest rates since 2022, interest expense has increased 36% since that year and thus it now consumes 30% of the operating income of the trust.

Net debt is $2.1 billion, which is only 41% of the market capitalization of the stock. Under normal business conditions, the trust is not likely to have any problem servicing its debt.

On the other hand, in the event of a severe and prolonged downturn, Chartwell Retirement Residences may face some financial pressure due to its somewhat leveraged balance sheet.

Dividend & Valuation Analysis

Chartwell Retirement Residences is currently offering an above-average dividend yield of 3.0%, which is nearly triple the 1.1% yield of the S&P 500.

The stock is an interesting candidate for income investors, but they should be aware that the dividend has often been far from safe due to a high payout that is typical of the trust. That said, the payout ratio has declined in recent years and is projected to be a very reasonable 56% for 2026.

This means that, in the absence of a recession or another downturn, the trust is not likely to cut its dividend sharply.

In reference to the valuation, Chartwell Retirement Residences is currently trading for 18.7 times its expected FFO per share this year. Given the lackluster performance record of the trust, we assume a fair price-to-FFO ratio of 13.0.

Therefore, the current FFO multiple is much higher than our assumed fair price-to-FFO ratio. If the stock trades at its fair valuation level in five years, it will incur a 7.0% annualized drag on its returns.

Taking into account the expected FFO per share growth rate of 1%, the 3.0% current dividend yield, and a high single-digit headwind from multiple compression, Chartwell Retirement Residences could offer a -2.4% average annual total return over the next five years.

The expected return signals that the stock is far from attractive right now.

Final Thoughts

Chartwell Retirement Residences operates in an industry with promising growth prospects but it has exhibited a lackluster performance record. The stock is offering an above-average dividend yield of 3.0% but it is richly valued right now and therefore it is unattractive from a total return standpoint.

Therefore, investors should wait for a much lower entry point before buying the stock.

Additional Reading

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

{kind=link}