Updated on April 15th, 2026 by Josh Arnold

Real Estate Investment Trusts, or REITs, are a core holding for many income investors due to their high dividend yields.

The coronavirus pandemic was devastating for many REITs. It especially hit the hospitality industry hard, including REITs in that industry.

Apple Hospitality REIT Inc. (APLE) is a REIT that pays a monthly dividend. Monthly dividend stocks pay shareholders 12 dividends per year instead of the more typical quarterly payments.

We created a list of all 118 monthly dividend stocks (along with important financial metrics such as dividend yields and payout ratios). You can download the spreadsheet by clicking on the link below:

Apple Hospitality has a 7.7% dividend yield, which is high. The high current yield and monthly dividend payouts make APLE an appealing stock for income investors.

This article will discuss this REIT in greater detail.

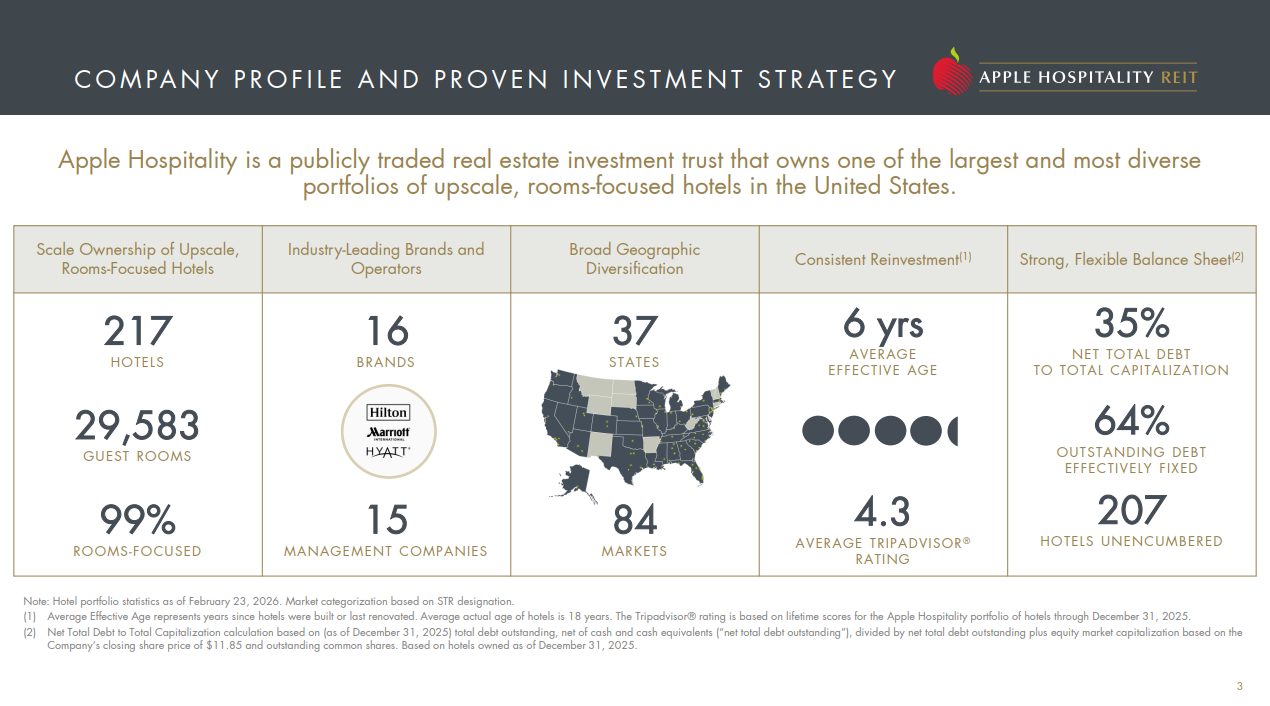

Business Overview

Apple Hospitality owns one of the largest and most diverse portfolios of upscale, rooms-focused hotels in the United States.

As of February 2026, Apple Hospitality owned 217 hotels with 29,583 guest rooms in 37 states, comprised of 84 markets.

APLE’s hotel portfolio consists of 16 different brands of hotels, with most being Hilton brands.

Source: Investor Presentation

Apple Hospitality posted fourth quarter and full-year results on February 23rd, 2026, and results were mixed. Revenue was $326.4 million for the quarter, off 2% year-over-year. Comparable hotels ADR was down 0.9% to $151.89, while occupancy was down 1.7% to 70.4%. With those in mind, RevPAR was off 2.6% to $106.90. Adjusted EBITDA fell 8.4% to $99.2 million as lower revenue deleveraged expenses. Modified FFO was $73.1 million, down 4.4% year-over-year. On a per-share basis, it was down from 32 cents to 31 cents.

We see $1.52 in adjusted FFO-per-share for 2026, which would be almost exactly what Apple produced in 2025, if achieved.

Growth Prospects

Since it first began reporting FFO/share in its annual reports (2011), Apple Hospitality initially generated very impressive annualized FFO/share growth thanks to its growing scale (due in large part to a merger in 2015), effective and efficient business model, and strong economic tailwinds in the United States during that period.

However, this growth rate has slowed dramatically recently, largely due to the Covid-19 outbreak and an accompanying downturn in the hotel industry that was further accelerated by the rise of companies like AirBnB.

We expect very modest growth to resume in the years ahead. Specifically, we forecast 1.0% compound annual growth of FFO-per-share over the next five years.

Apple Hospitality’s growth prospects will mostly come from an increase in rents. They were also selling less-profitable properties to acquire more beneficial properties.

Other growth drivers will come from long-term cost savings. The company has an expense reduction ratio target of 0.80 – 0.90. This is accomplished by increasing the cross-utilization of managers and associates.

Scaling to renegotiate vendor contracts and optimize labor management software that is already in place can also help reduce overall costs.

More locations and market diversification should help the company continue to grow its FFO for years to come. This will also allow the company to start increasing its dividends.

Source: Investor Presentation

Dividend Analysis

The company’s dividend history is not long, as it became public in 2015. The stock pays its dividend monthly, which is attractive to many income investors. In 2016, the company increased its annualized dividend substantially by 50%, from a $0.80 rate to a $1.20 rate.

However, in the following years, the dividend stayed at that same rate until 2020, when the COVID-19 pandemic forced the company to cut its dividend and freeze it to a $0.30 rate for the year.

The company resumed dividends in 2021. APLE currently pays a $0.08 monthly dividend, which equates to $0.96 per share annually.

The company’s healthy balance sheet helps support the dividend. APLE has some of the lowest debt-to-equity in the sector, plenty of liquidity, and a well-laddered debt maturity profile.

With an expected 2026 dividend payout ratio of approximately 64% in terms of FFO, we view the dividend as secure, although a steep recession would put the dividend at risk. We note the dividend has been at the same level for more than three years.

Apple does not have a recorded history as a public trust during a typical recession. Therefore, it is hard to judge its recession resilience, other than to compare it to hotel REITs.

Typically, during a recessionary period, hotel REITs experience significant income losses. Therefore, Apple is likely not very recession-resistant.

However, its concentration in strong brand names, excellent locations, strong balance sheet, franchising model, and emphasis on value should enable it to outperform its peers in a recession.

Final Thoughts

Apple Hospitality is one of the strongest players in the hotel sector due to its strong brand power, healthy balance sheet, and high-quality assets. The company has the potential to start increasing its dividends.

The dividend payout ratio is relatively low, and AFFO per share is expected to grow over the next five years. We have a sell rating on the stock given the lack of dividend increases, but Apple could have a place in the portfolio of investors that value a stable, market-beating yield over pure income growth.

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

{kind=link}