A personal loan is an unsecured, fixed-rate installment loan that gives you access to a lump sum of cash for real financial needs. Whether you’re looking to consolidate $10,000 of credit card debt, pay off a $7,500 medical bill, or fund a $12,000 home renovation project, a personal loan can provide predictable financing with a clear payoff date.

This guide focuses on consumer personal loans available in the U.S. with fixed terms typically ranging from 12 to 84 months and predictable fixed monthly payments. Most lenders let you check your estimated rates with only a soft credit inquiry, so you can shop around without hurting your credit score. According to the Consumer Financial Protection Bureau (CFPB), rate shopping within a short window generally counts as a single inquiry for credit scoring purposes, helping borrowers compare personal loan rates more safely.

Below, we’ll cover rates, terms, fees, funding speed, common uses of personal loan funds, and how loan approval and your actual APR are determined.

Personal Loans vs. Payday Loans: What’s the Difference?

When you’re short on cash, it’s easy to search for “payday loans near me” or “quick cash advance.” But payday loans and personal loans are dramatically different financial products.

Payday loans typically:

Require repayment in 2–4 weeks

Carry extremely high fees (often equivalent to 300%+ APR)

Can trap borrowers in a cycle of rollovers

In contrast, personal loans:

Offer fixed repayment terms (12–84 months)

Have structured monthly payments

Typically range from 7.99%–24.99% APR for qualified borrowers

Provide significantly lower long-term borrowing costs

For example, borrowing $1,000 through a payday loan could cost hundreds in fees within a month. A structured personal loan spreads repayment over time and often results in much lower overall cost.

If you’re considering payday loans because you need fast funding, it’s worth checking whether you qualify for a personal loan first.

👉 See how much you could qualify for in minutes — no fee to check and no obligation to accept an offer.

Even borrowers with fair credit may qualify for installment-based personal loans that are far safer than short-term payday lending.

No Fees on Many Modern Personal Loans

Many leading lenders now advertise “no fees” structures on qualifying personal loans. This means no application fee, no origination fee, and no prepayment penalties—features that can save you hundreds or even thousands of dollars over the life of your loan.

Here’s what borrowers can typically expect from fee-friendly lenders:

$0 origination fee — Unlike some lenders that charge 1%–8% of the loan amount upfront, many now waive this entirely

$0 prepayment penalty — Pay off a 60-month loan in 36 months without extra charges

Transparent late fee policy — Late fees, when applicable, are usually $15–$40 and clearly disclosed upfront

Keep in mind that some fees may still apply. Returned payment fees (for bounced checks) and late fees are common even among lenders with otherwise fee-free structures. Always review the fee schedule before signing.

When you check your estimated rate, most lenders use a soft credit pull that does not impact your FICO score. Submitting a full application triggers a hard credit inquiry, which may temporarily lower your score by a few points.

Estimated Monthly Payment and Rate Examples

Before you apply online, it’s smart to calculate your estimated monthly payments using a loan calculator. Most tools let you input your desired loan amount (commonly $2,500–$50,000), preferred term (12–84 months), and estimated APR range (such as 8.99%–24.99%) to preview what you’d pay each month.

Here are two concrete scenarios to illustrate how loan terms affect your payments:

Scenario 1: A $10,000 loan at 11.99% APR over 36 months results in an estimated monthly payment of about $332. If all payments are made on time, the total cost comes to roughly $11,952, meaning you’d pay approximately $1,952 in interest.

Scenario 2: That same $10,000 loan at 11.99% APR stretched over 60 months drops the monthly payment to about $222—but the total cost rises to approximately $13,320, with $3,320 going toward interest.

These examples are illustrations based on typical market data as of early 2026 rather than guaranteed offers. Your individual APR depends on your credit profile, income, and existing debts.

How Your Details Affect Payment and APR

Several borrower factors influence the annual percentage rate you’ll qualify for—and by extension, your monthly payment.

Credit score is the primary driver. Borrowers with scores in the 740–799 range might see APRs around 10%–14%, while someone at 680 could face rates of 18% or higher on the same $15,000, 60-month loan. Your debt to income ratio matters too; lenders want to see that your existing monthly debt payments don’t consume too much of your income. Employment stability and your stated loan purpose (debt consolidation versus home improvement, for example) can also shift your rate.

The top factors that move APR up or down include:

Credit score band (660–719 vs. 720–799 vs. 800+)

Debt to income ratio (lower is better)

Employment history and income stability

Loan amount and term length

Stated purpose of the loan

Estimates shown on prequalification tools are based on real lender data from late 2025–early 2026 but are not offers or commitments. A hard credit inquiry at full application can temporarily lower your credit score by a few points, but consistent on-time payments may help rebuild your credit history over time.

Typical APR Ranges and “Great Rate” Benchmarks

Current typical APR ranges for an unsecured personal loan fall between approximately 7.99% and 24.99%. Borrowers with excellent credit (typically 760+) sometimes see offers below 10% on loans of $10,000 or more with 36- or 48-month terms.

Example of a great rate: A $15,000 loan at 8.74% APR over 36 months produces a monthly payment of about $475. Total interest paid over the full term: approximately $2,100.

Example of a higher-APR scenario: A $5,000 loan at 19.99% APR over 60 months results in a monthly payment of about $132. Total interest paid: approximately $2,920—more than half the original loan amount.

The difference between an 8.74% APR and a 19.99% APR on a $10,000 loan over 48 months translates to roughly $2,400 in additional interest. That’s why improving your creditworthiness before applying—or shopping multiple lenders—can make a significant financial difference.

A fixed interest rate means your rate and monthly payment will not change over the life of the loan, which simplifies budgeting compared to variable-rate products like credit cards or adjustable-rate lines of credit.

Flexible Terms and Borrowing Limits

Typical loan amount ranges span $1,500 to $50,000, though some bank lenders cap unsecured loans at $20,000 while others offer higher loan amounts up to $50,000 for highly qualified borrowers with strong credit and income.

Common repayment term options include 12, 24, 36, 48, 60, and up to 84 months. A longer period reduces your monthly payment but increases total interest cost significantly.

Consider this comparison for a $20,000 loan at 13.99% APR:

36-month term: Monthly payment of approximately $683; total interest paid around $4,600

84-month term: Monthly payment of approximately $356; total interest paid around $9,900

The 84-month term cuts your payment nearly in half but more than doubles your interest expense. If you’re consolidating credit cards charging 24%–29% APR, choosing the shortest term you can comfortably afford maximizes your savings.

👉 Get a fast decision and review real loan terms online — approval could mean funding in as little as 24 hours.

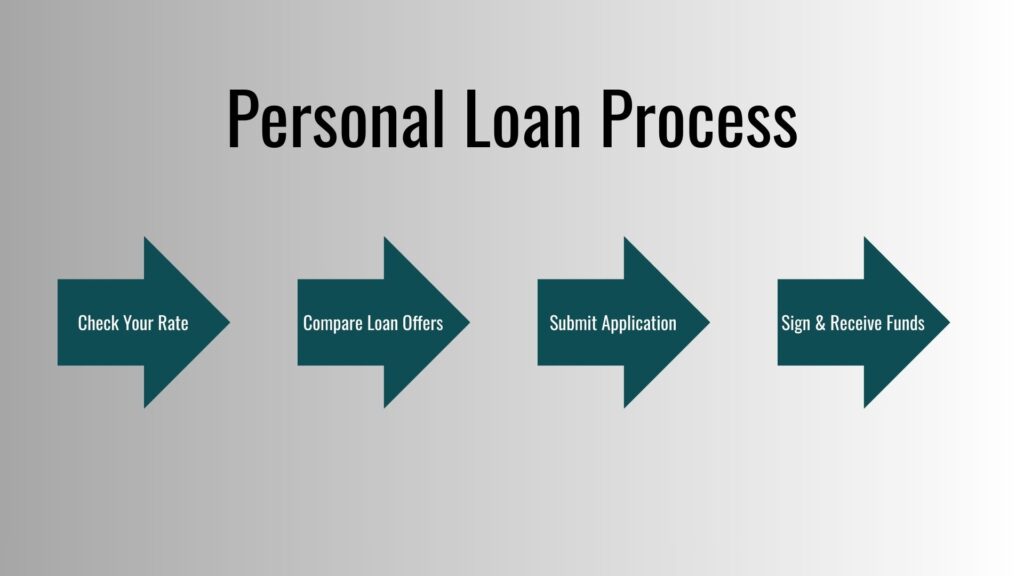

How Personal Loans Work from Application to Funding

The typical application process moves quickly with most online lenders. Here’s how it generally works:

Step 1: Check your rate. Enter basic information—your name, address, income, and last four digits of your SSN. The lender performs a soft inquiry to show your prequalified options without affecting your credit report.

Step 2: Review and select an offer. Compare available loan amounts, terms, and estimated APRs. Choose the option that fits your budget and needs.

Step 3: Submit your full application. Provide supporting documentation such as recent pay stubs, bank statements, or tax returns. This triggers a hard credit inquiry.

Step 4: Sign and receive funds. Once approved, you’ll sign electronically. Many lenders can deposit funds directly into your linked checking or savings account as soon as the next business day—sometimes within a few hours of closing.

For debt consolidation loans, some lenders offer to send your personal loan funds directly to creditors on your behalf, paying off credit cards without the money ever hitting your account.

What Is a Personal Loan?

A personal loan is an unsecured installment loan with a fixed interest rate and fixed monthly payments over a set loan term, usually 1–7 years. Unlike auto loans or mortgages, no collateral is required—you don’t risk losing your car or house if you default.

However, missed payments can still lead to collection actions, late fees, and negative marks on your credit report. Most personal loans are disbursed as a single lump sum into a checking or savings account, which you can then use for approved purposes.

Unsecured vs. secured borrowing: An unsecured loan relies entirely on your creditworthiness for approval, typically resulting in higher interest rates compared to secured products. A home equity loan or auto loan uses your property as collateral, offering lower rates but putting your asset at risk. If you have limited assets or prefer not to pledge collateral, an unsecured personal loan may be the more accessible choice.

Eligibility, Credit Checks, and Documentation

Standard eligibility criteria for most mainstream lenders include:

You must be at least 18 years old (21+ in Puerto Rico), a U.S. citizen or permanent resident, and able to verify your income through documentation. Most lenders look for a minimum credit score in the mid-600s, though some cater to borrowers with fair credit while others target only excellent-credit applicants.

A soft inquiry is used during prequalification and does not impact your credit score. When you submit a full application, the lender performs a hard credit inquiry, which may lower your score by a few points temporarily. Multiple hard inquiries in a short period can compound this effect, so try to complete your loan shopping within a 14-day window.

Typical documents requested include a government-issued ID, recent pay stubs or tax returns for income verification, proof of address (utility bill or lease), and sometimes bank statements if your income is variable or self-employment based. Note that some lenders don’t accept joint or co-applications for unsecured personal loans.

What You Can Use a Personal Loan for

Personal loans are flexible and can cover a wide range of personal expenses, subject to each lender’s restrictions.

Common approved uses include:

Consolidating debt: Pay off $8,000–$25,000 of high-interest credit card balances

Home improvements: Finance a $5,000–$20,000 kitchen remodel or roof replacement

Medical expenses: Cover a $6,000 outpatient surgery or ongoing treatments

Auto repairs: Handle a $3,000 transmission replacement or car repairs

Life events: Fund a $10,000–$25,000 wedding, adoption, or cross-country relocation

Some lenders prohibit using personal loan funds for post-secondary education tuition, business working capital, or certain real-estate transactions. Always confirm your intended use is allowed before applying.

Match your loan term to the expected life of the expense. A 3-year term makes sense for a $9,000 car repair, while a 5-year term might better suit a major home renovation with lasting value.

Debt Consolidation and Credit Card Payoff

Using a personal loan to consolidate debt is one of the most strategic applications. If you’re carrying $15,000 across multiple credit cards at 24%–29% APR, a consolidation loan at 13.99% APR over 48 months could save you thousands in interest and give you a clear payoff date.

Example comparison:

Minimum payments on $15,000 at 24% APR: Paying $375/month, it takes over 5 years to pay off with approximately $7,500+ in total interest

Personal loan at 13.99% APR over 48 months: Fixed payment of about $407/month, paid off in exactly 4 years with approximately $4,500 in total interest

That’s roughly $3,000 in potential savings—plus the psychological benefit of knowing exactly when you’ll be debt-free.

One important caution: if you consolidate credit card debt but continue using those cards, you can end up with both loan payments and new card balances. Many lenders offer to pay your creditors directly, which can help you avoid this trap by ensuring the cards get paid off immediately.

Other Common Uses: Home, Medical, and Life Events

Personal loans work well for specific home projects when a home equity loan isn’t available or would take too long to close. A $12,000 kitchen refresh or $7,500 roof repair can be funded quickly and paid off over 3–5 years.

Medical expenses are another common use. A $6,000 outpatient surgery, orthodontic work, or ongoing IVF treatments totaling $15,000–$20,000 can be more manageable with a fixed rate personal loan than revolving medical credit cards that often have deferred-interest traps.

For significant life events—a $10,000–$25,000 wedding, international adoption, or major relocation—a personal loan provides predictable payments. Just balance the emotional importance of the event against the long-term cost of borrowing.

Before committing, compare alternatives: 0% intro APR credit cards (if you can pay off within the promotional period), in-house medical payment plans, or simply saving up. A personal loan makes sense when you need funds now and the math works in your favor.

Where to Get a Personal Loan

There are three main places borrowers typically get personal loans:

Traditional banks

Credit unions

Online lenders

Banks and credit unions can offer competitive personal loan rates, especially if you already have an existing relationship. However, their approval process can sometimes take longer, and qualification standards may be stricter.

Online lenders have become increasingly popular because they:

Offer faster approvals (sometimes same-day funding)

Allow you to prequalify online

Often accept a wider range of credit scores

Make it easy to compare loan options

If speed, convenience, and rate comparison matter to you, online platforms tend to provide the most flexibility.

👉 Need money fast? Submit your information and see if you’re approved for up to $50,000 — funds could arrive as soon as tomorrow.

Instead of guessing which lender might approve you, you can check multiple options at once and choose the offer that fits your budget.

Best Lenders for Personal Loans in 2026

If you’re serious about finding the lowest personal loan rates, the smartest move isn’t applying with just one lender — it’s comparing multiple offers at once.

Different lenders evaluate borrowers differently. One bank might quote you 17.99% APR, while another could offer 12.49% for the exact same credit profile. Over a $15,000 loan, that difference can mean thousands of dollars in interest.

Instead of filling out five separate applications (and risking multiple hard credit pulls), many borrowers now use loan comparison platforms to see real offers in minutes.

These platforms allow you to:

Compare personal loan rates from multiple lenders

See estimated APR ranges without hurting your credit

Filter by loan amount, term, and credit profile

Find options beyond traditional banks

If you’re shopping for personal loans between $2,000 and $50,000, comparing offers side-by-side is one of the easiest ways to lower your total borrowing cost.

Comparing Personal Loan Offers

When evaluating offers from multiple banks, credit unions, and online lenders, look beyond the advertised “as low as” rate. That headline number often applies only to borrowers with exceptional credit and may not reflect your actual offer.

Key comparison criteria:

APR (not just interest rate): APR includes both the interest rate and any fees, giving you the true cost of borrowing

Origination fees: Some lenders charge 1%–8% upfront; others charge $0

Late fee policies: Typically $15–$40 per missed payment

Available terms: Does the lender offer 36, 60, and 84 months, or limited options?

Funding speed: Same-day or next business day vs. 3–5 business days

Obtain at least 2–3 prequalified offers on the same day using the same loan amount and term (for example, $10,000 at 48 months) to make side-by-side comparisons fair. Check lender reputation through independent customer reviews—a lender averaging 4.7–4.9 out of 5 across tens of thousands of reviews typically indicates consistent service quality.

Understanding Disclosures and Restrictions

Lenders are legally required to provide key disclosures before you sign, including the APR range, payment schedule, total of payments, and any applicable fees. These disclosures give you the full picture of what you’re agreeing to.

Terms can vary by state and may change at any time, so always rely on current disclosures provided at the time of application rather than older marketing materials. What you see during prequalification is an estimate; the loan agreement contains the binding terms.

Common restrictions spelled out in loan agreements include:

No use for post-secondary education expenses

No use for business working capital

No use for certain real-estate investments or purchases

Maximum amount limits based on creditworthiness

The Military Lending Act provides additional protections for active-duty servicemembers and their dependents, including caps on APR. All lenders must comply with applicable state and federal regulations, including equal housing lender requirements where applicable.

Read the promissory note carefully. If anything is unclear, contact customer service or consult a financial professional before e-signing. Hidden fees or confusing terms are red flags—reputable lenders maintain transparency throughout the process.

Is a Personal Loan Right for You?

Personal loans offer several advantages: fast access to $1,500–$50,000, fixed payments that fit your budget, no collateral required, and often no origination fees or prepayment penalties. For the right borrower and the right purpose, they’re a powerful financial tool.

The main risks include taking on new debt, potentially higher rates if your credit is only fair (APR above 20% is common for scores below 670), and the possibility of missed payments damaging your credit score. If you’re already stretched thin financially, adding another payment may not be wise.

A personal loan can be especially helpful when you’re:

Replacing high-interest credit card debt with a lower fixed rate

Covering unexpected expenses like emergency auto repairs or medical bills

Financing a one-time significant expense with a clear repayment plan

It may be less appropriate when you could save up for the expense, qualify for a 0% intro APR credit card, or would struggle to fit the payment into your monthly budget.

Run the numbers with your own income, existing debts, and budget. Use the payment scenarios above as a starting point, then factor in your specific situation. A new fixed monthly payment should fit comfortably within your cash flow—not create financial stress.

Consider prequalifying with 2–3 reputable lenders to see your estimated rates without impacting your credit. Compare offers side by side, read all disclosures carefully, and choose the option that aligns with your long-term financial goals. The right personal loan can simplify your finances and save you money—just make sure it’s the right fit before you borrow.

👉 Ready to see your options? Submit your information now and get matched with lenders offering personal, installment, and emergency loans.

FAQs

Most lenders require a minimum credit score between 600 and 660 to qualify for unsecured personal loans. However, borrowers with scores above 720 typically qualify for the lowest personal loan rates.

If your score is below 670, you may still be approved, but your annual percentage rate (APR) will likely be higher. Improving your credit score before applying — even by 20–30 points — can significantly reduce your borrowing cost.

As of early 2026, personal loan rates generally range from approximately 7.99% to 24.99% APR.

Borrowers with excellent credit (760+) may qualify for rates under 10%, while fair-credit borrowers often see APRs between 18% and 25%. Your exact rate depends on:> Credit score> Debt-to-income ratio> Loan amount> Loan term

Comparing multiple lenders is one of the most effective ways to secure a lower rate.

Many online lenders provide approval decisions within minutes and can fund loans as soon as the next business day. Some lenders even offer same-day funding, depending on verification requirements and banking cut-off times.

Traditional banks and credit unions may take longer — sometimes several days to a week.

If speed matters, online personal loans typically offer the fastest turnaround.

In most cases, yes.

Payday loans are short-term loans that usually must be repaid within two to four weeks and often carry extremely high fees — sometimes equivalent to 300% APR or more.

Personal loans offer:> Fixed monthly payments> Structured repayment terms (12–84 months)> Significantly lower interest rates> More predictable total costs

If you qualify for a personal loan, it is almost always a safer and more affordable option than a payday loan.

Prequalifying for personal loans typically uses a soft credit inquiry, which does not affect your credit score.

Submitting a full application triggers a hard credit inquiry, which may temporarily lower your score by a few points. To minimize impact, complete your rate shopping within a short window (usually 14 days), so credit scoring models treat multiple inquiries as one.

Personal loans can be used for many legitimate personal expenses, including:> Debt consolidation> Medical bills> Home improvements> Emergency expenses> Major life events

However, most lenders prohibit using personal loan funds for post-secondary education, business capital, or certain real estate investments. Always confirm approved uses before signing your loan agreement.

Both can be good options.

Banks and credit unions may offer competitive personal loan rates to existing customers. Online lenders often provide faster approvals, easier comparison tools, and more flexible qualification standards.

Comparing multiple lenders side-by-side is usually the best strategy for finding the most competitive offer.

")

")

{kind=link}