Published on April 6th, 2026 by Bob Ciura

Investors have been spoiled in the past decade.

The S&P 500 Index has been on a nearly uninterrupted rally since the end of the Great Recession of 2008.

While there have been periodic selloffs in between, such as the market downturn in 2020 due to the coronavirus pandemic, markets have always recovered.

But investors should remember that bear markets happen, and recessions are inevitable in a cyclical economy. With persistent inflation, the war in Iran, and the uncertainty of tariffs, the S&P 500 Index is down 3.5% year-to-date.

What is most important is that investors keep their cool when the markets take a nosedive. Investors should resist the urge to sell their stocks, and continue to hold quality dividend stocks even though it is tempting to cash out when markets are in free-fall.

With this in mind, we created a downloadable list of over 130 Dividend Champions.

You can download your free copy of the Dividend Champions list, along with relevant financial metrics like price-to-earnings ratios, dividend yields, and payout ratios, by clicking on the link below:

Investors are likely familiar with the Dividend Aristocrats, a group of 69 stocks in the S&P 500 Index with 25+ consecutive years of dividend increases.

Meanwhile, investors should also familiarize themselves with the Dividend Champions, which have also raised their dividends for at least 25 years in a row, but do not need to be in the S&P 500.

These 10 Dividend Champions represent high-quality businesses that are able to generate strong profits and keep raising their dividends, even during bear markets.

Table of Contents

The below list includes only Dividend Champions based in the U.S., with Dividend Risk Scores of ‘C’ or higher in the Sure Analysis Research Database, and current yields of 1.2% or higher which is the average yield of the S&P 500 right now.

Lastly, the list includes stocks with market caps of $2 billion or higher, to exclude small-caps and focus on more stable businesses.

Stocks are ranked by expected total annual return over the next five years, from lowest to highest. You can instantly jump to any specific section of the article by clicking on the links below:

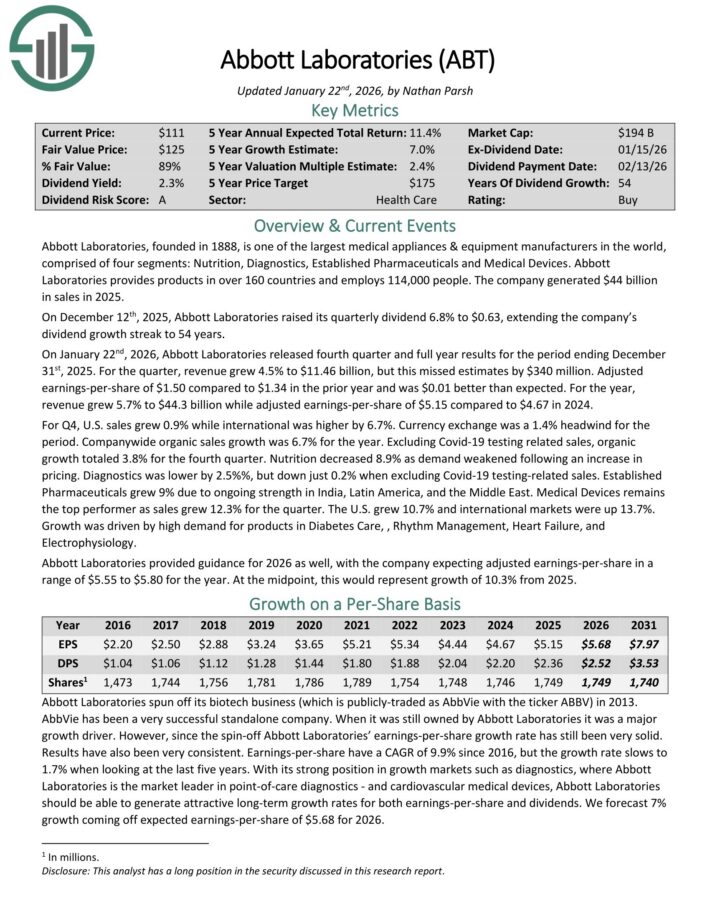

Bear Market Stock #10: Abbott Laboratories (ABT)

5-year expected returns: 13.2%

Abbott Laboratories, founded in 1888, is one of the largest medical appliances & equipment manufacturers in the world, comprised of four segments: Nutrition, Diagnostics, Established Pharmaceuticals and Medical Devices.

Abbott Laboratories provides products in over 160 countries and employs 114,000 people. The company generated $44 billion in sales in 2025.

On December 12th, 2025, Abbott Laboratories raised its quarterly dividend 6.8% to $0.63, extending the company’s dividend growth streak to 54 years.

On January 22nd, 2026, Abbott Laboratories released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue grew 4.5% to $11.46 billion, but this missed estimates by $340 million.

Adjusted earnings-per-share of $1.50 compared to $1.34 in the prior year and was $0.01 better than expected. For the year, revenue grew 5.7% to $44.3 billion while adjusted earnings-per-share of $5.15 compared to $4.67 in 2024.

For Q4, U.S. sales grew 0.9% while international was higher by 6.7%. Currency exchange was a 1.4% headwind for the period.

Abbott Laboratories provided guidance for 2026 as well, with the company expecting adjusted earnings-per-share in a range of $5.55 to $5.80 for the year. At the midpoint, this would represent growth of 10.3% from 2025.

Click here to download our most recent Sure Analysis report on ABT (preview of page 1 of 3 shown below):

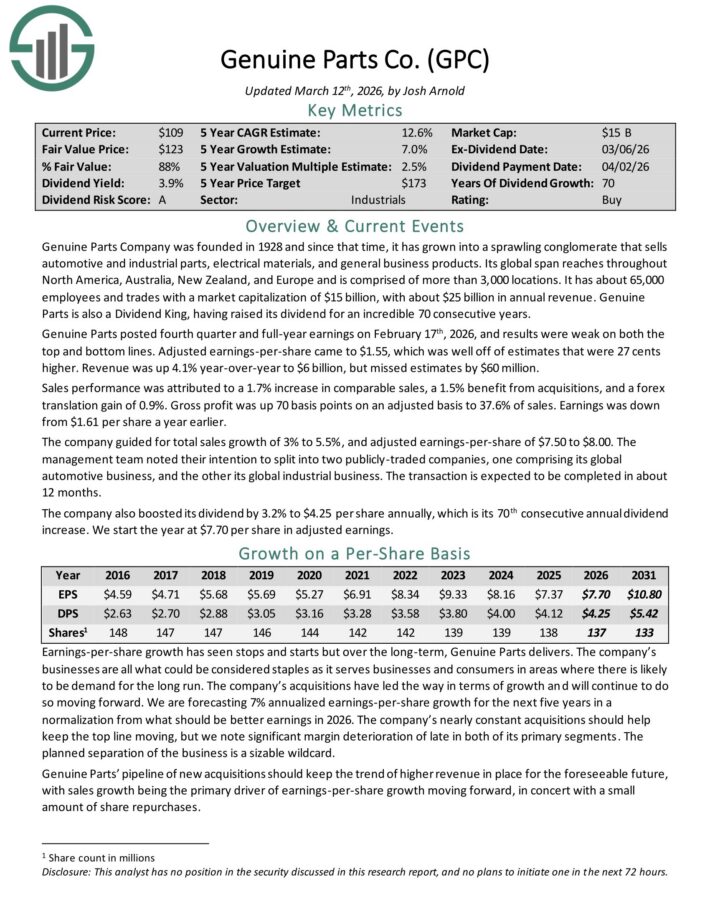

Bear Market Stock #9: Genuine Parts Co. (GPC)

5-year expected returns: 13.8%

Genuine Parts Company was founded in 1928 and since that time, it has grown into a sprawling conglomerate that sells automotive and industrial parts, electrical materials, and general business products.

Its global span reaches throughout North America, Australia, New Zealand, and Europe and is comprised of more than 3,000 locations. It has about 63,000 employees with about $24 billion in annual revenue.

Genuine Parts is also a Dividend King, having raised its dividend for an incredible 69 consecutive years.

Genuine Parts posted fourth quarter and full-year earnings on February 17th, 2026, and results were weak on both the top and bottom lines. Adjusted earnings-per-share came to $1.55, which was well off of estimates that were 27 cents higher. Revenue was up 4.1% year-over-year to $6 billion, but missed estimates by $60 million.

Sales performance was attributed to a 1.7% increase in comparable sales, a 1.5% benefit from acquisitions, and a forex translation gain of 0.9%. Gross profit was up 70 basis points on an adjusted basis to 37.6% of sales. Earnings was down from $1.61 per share a year earlier.

The company guided for total sales growth of 3% to 5.5%, and adjusted earnings-per-share of $7.50 to $8.00.

Click here to download our most recent Sure Analysis report on GPC (preview of page 1 of 3 shown below):

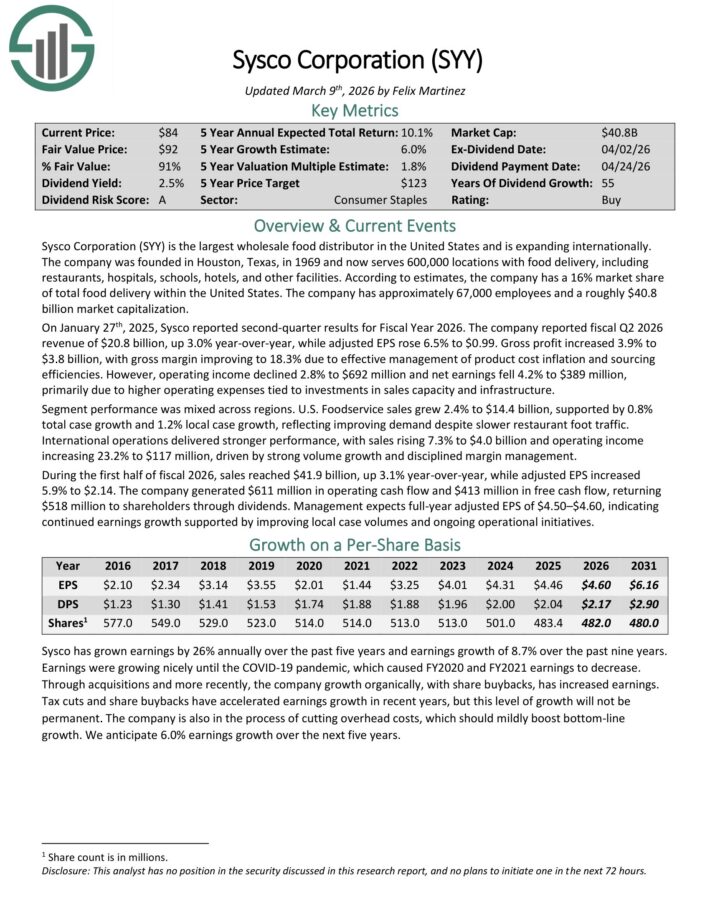

Bear Market Stock #8: Sysco Corp. (SYY)

5-year expected returns: 13.8%

Sysco Corporation (SYY) is the largest wholesale food distributor in the United States.

The company was founded in Houston, Texas, in 1969 and now serves 600,000 locations with food delivery, including restaurants, hospitals, schools, hotels, and other facilities.

On January 27th, 2026, Sysco reported second-quarter results for Fiscal Year 2026. The company reported fiscal Q2 2026 revenue of $20.8 billion, up 3.0% year-over-year, while adjusted EPS rose 6.5% to $0.99.

Gross profit increased 3.9% to $3.8 billion, with gross margin improving to 18.3% due to effective management of product cost inflation and sourcing efficiencies.

However, operating income declined 2.8% to $692 million and net earnings fell 4.2% to $389 million, primarily due to higher operating expenses tied to investments in sales capacity and infrastructure.

Segment performance was mixed across regions. U.S. Foodservice sales grew 2.4% to $14.4 billion, supported by 0.8% total case growth and 1.2% local case growth, reflecting improving demand despite slower restaurant foot traffic.

International operations delivered stronger performance, with sales rising 7.3% to $4.0 billion and operating income increasing 23.2% to $117 million, driven by strong volume growth and disciplined margin management.

On March 30th, 2026, Sysco announced it will acquire Jetro Restaurant Depot in a transaction valued at $29.1 billion. Jetro Restaurant Depot is described as the nation’s premier cash & carry food wholesaler and the acquisition will give Sysco a major entryway into this growing channel.

Click here to download our most recent Sure Analysis report on SYY (preview of page 1 of 3 shown below):

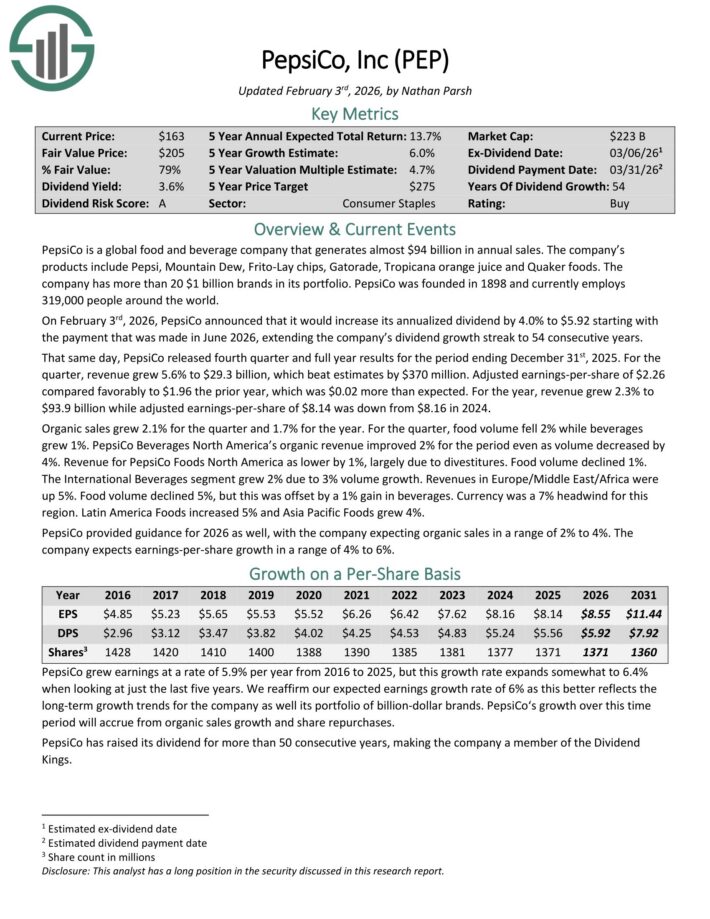

Bear Market Stock #7: PepsiCo Inc. (PEP)

5-year expected returns: 14.6%

PepsiCo is a global food and beverage company that generates almost $94 billion in annual sales. The company’s products include Pepsi, Mountain Dew, Frito-Lay chips, Gatorade, Tropicana orange juice and Quaker foods.

The company has more than 20 $1 billion brands in its portfolio.

On February 3rd, 2026, PepsiCo announced that it would increase its annualized dividend by 4.0% to $5.92 starting with the payment that was made in June 2026, extending the company’s dividend growth streak to 54 consecutive years.

That same day, PepsiCo released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue grew 5.6% to $29.3 billion, which beat estimates by $370 million.

Adjusted earnings-per-share of $2.26 compared favorably to $1.96 the prior year, which was $0.02 more than expected.

For the year, revenue grew 2.3% to $93.9 billion while adjusted earnings-per-share of $8.14 was down from $8.16 in 2024. Organic sales grew 2.1% for the quarter and 1.7% for the year.

For the quarter, food volume fell 2% while beverages grew 1%. PepsiCo Beverages North America’s organic revenue improved 2% for the period even as volume decreased by 4%.

Revenue for PepsiCo Foods North America as lower by 1%, largely due to divestitures. Food volume declined 1%.

The International Beverages segment grew 2% due to 3% volume growth. Revenues in Europe/Middle East/Africa were up 5%. Food volume declined 5%, but this was offset by a 1% gain in beverages.

Currency was a 7% headwind for this region. Latin America Foods increased 5% and Asia Pacific Foods grew 4%.

PepsiCo provided guidance for 2026 as well, with the company expecting organic sales in a range of 2% to 4%. The company expects earnings-per-share growth in a range of 4% to 6%.

Click here to download our most recent Sure Analysis report on PEP (preview of page 1 of 3 shown below):

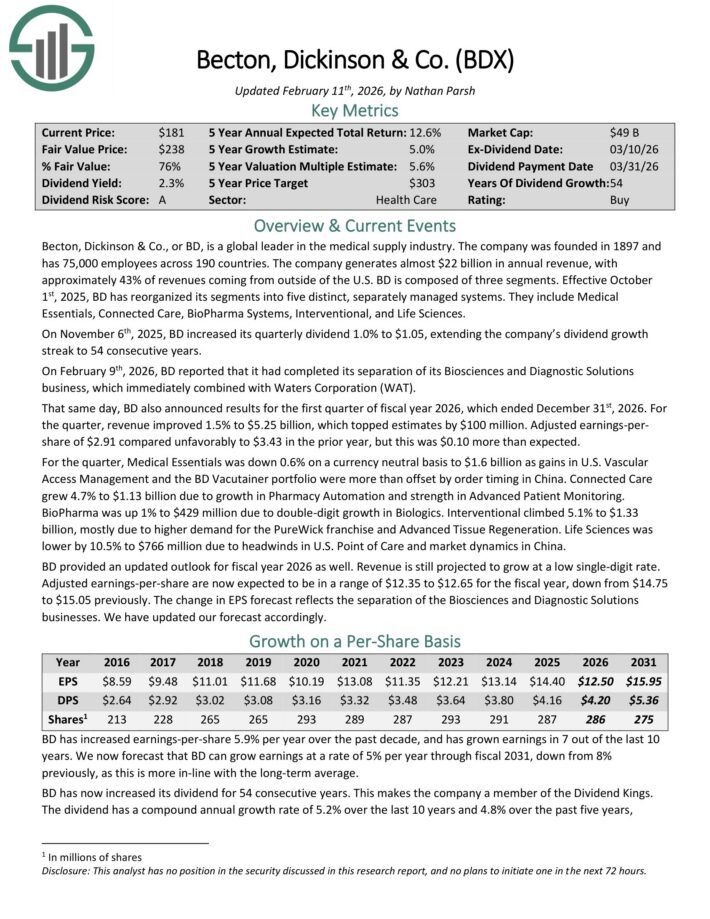

Bear Market Stock #6: Becton, Dickinson & Co. (BDX)

Annual expected returns: 16.3%

Becton, Dickinson & Co. is a global leader in the medical supply industry. The company was founded in 1897 and has 75,000 employees across 190 countries.

The company generates about $20 billion in annual revenue, with approximately 43% of revenues coming from outside of the U.S.

On November 6th, 2025, BD increased its quarterly dividend 1.0% to $1.05, extending the company’s dividend growth streak to 54 consecutive years.

BD also announced results for the first quarter of fiscal year 2026, which ended December 31st, 2026. For the quarter, revenue improved 1.5% to $5.25 billion, which topped estimates by $100 million.

Adjusted earnings-per-share of $2.91 compared unfavorably to $3.43 in the prior year, but this was $0.10 more than expected.

For the quarter, Medical Essentials was down 0.6% on a currency neutral basis to $1.6 billion as gains in U.S. Vascular Access Management and the BD Vacutainer portfolio were more than offset by order timing in China.

Connected Care grew 4.7% to $1.13 billion due to growth in Pharmacy Automation and strength in Advanced Patient Monitoring.

BioPharma was up 1% to $429 million due to double-digit growth in Biologics. Interventional climbed 5.1% to $1.33 billion, mostly due to higher demand for the PureWick franchise and Advanced Tissue Regeneration.

Click here to download our most recent Sure Analysis report on BDX (preview of page 1 of 3 shown below):

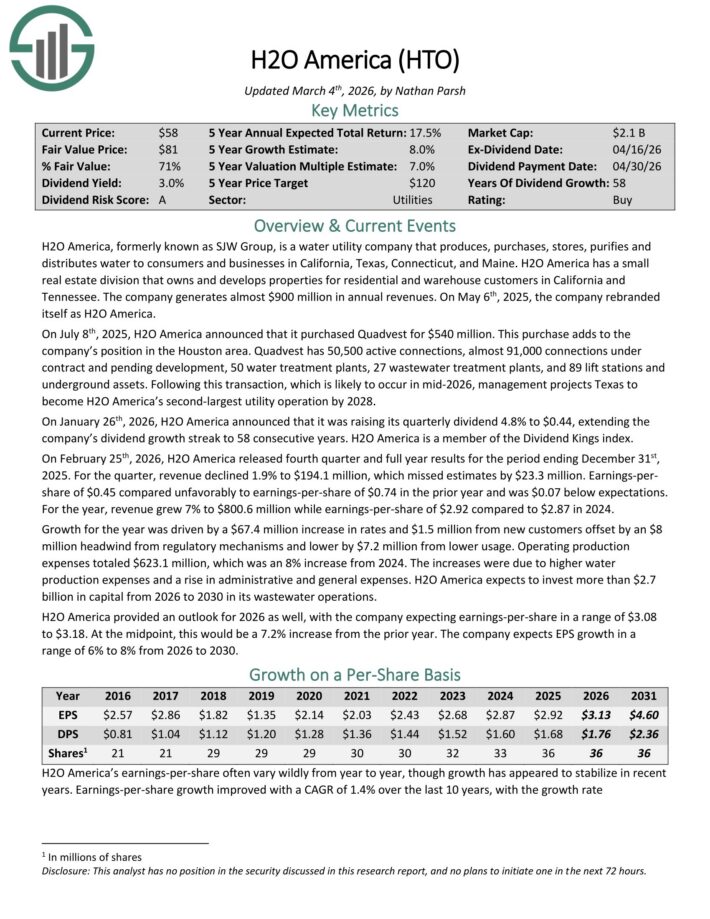

Bear Market Stock #5: H2O America (HTO)

Annual expected returns: 17.0%

H2O America, formerly known as SJW Group, is a water utility company that produces, purchases, stores, purifies and distributes water to consumers and businesses in the Silicon Valley area of California, the area north of San Antonio, Texas, Connecticut, and Maine.

It also has a small real estate division that owns and develops properties for residential and warehouse customers in California and Tennessee. The company generates about $670 million in annual revenues.

On July 8th, 2025, H2O America announced that it purchased Quadvest for $540 million. This purchase adds to the company’s position in the Houston area.

Quadvest has 50,500 active connections, almost 91,000 connections under contract and pending development, 50 water treatment plants, 27 wastewater treatment plants, and 89 lift stations and underground assets.

On January 26th, 2026, H2O America raised its quarterly dividend 4.8% to $0.44, extending the company’s dividend growth streak to 58 consecutive years.

On February 25th, 2026, H2O America released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue declined 1.9% to $194.1 million, which missed estimates by $23.3 million.

Earnings-per-share of $0.45 compared unfavorably to earnings-per-share of $0.74 in the prior year and was $0.07 below expectations.

For the year, revenue grew 7% to $800.6 million while earnings-per-share of $2.92 compared to $2.87 in 2024.

Growth for the year was driven by a $67.4 million increase in rates and $1.5 million from new customers offset by an $8 million headwind from regulatory mechanisms and lower by $7.2 million from lower usage.

Click here to download our most recent Sure Analysis report on HTO (preview of page 1 of 3 shown below):

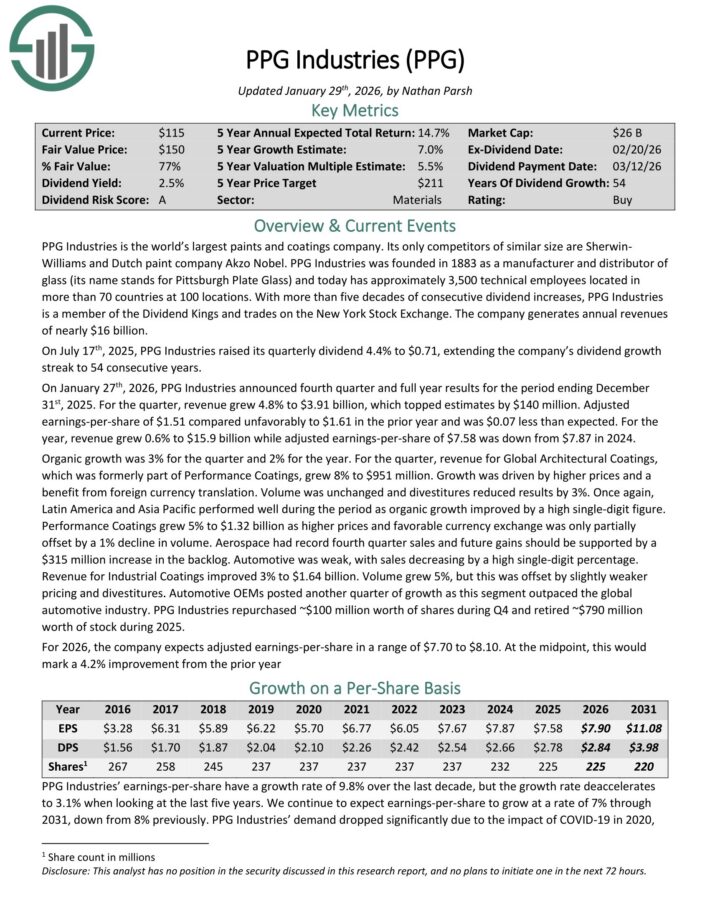

Bear Market Stock #4: PPG Industries (PPG)

Annual expected returns: 17.1%

PPG Industries is the world’s largest paints and coatings company. Its only competitors of similar size are Sherwin-Williams and Dutch paint company Akzo Nobel.

On January 27th, 2026, PPG Industries announced fourth quarter and full year results. For the quarter, revenue grew 4.8% to $3.91 billion, which topped estimates by $140 million. Adjusted earnings-per-share of $1.51 compared unfavorably to $1.61 in the prior year and was $0.07 less than expected.

For the year, revenue grew 0.6% to $15.9 billion while adjusted earnings-per-share of $7.58 was down from $7.87 in 2024. Organic growth was 3% for the quarter and 2% for the year.

For the quarter, revenue for Global Architectural Coatings, which was formerly part of Performance Coatings, grew 8% to $951 million.

Growth was driven by higher prices and a benefit from foreign currency translation. Volume was unchanged and divestitures reduced results by 3%.

Once again, Latin America and Asia Pacific performed well during the period as organic growth improved by a high single-digit figure.

Performance Coatings grew 5% to $1.32 billion as higher prices and favorable currency exchange was only partially offset by a 1% decline in volume.

Aerospace had record fourth quarter sales and future gains should be supported by a $315 million increase in the backlog. Automotive was weak, with sales decreasing by a high single-digit percentage.

Revenue for Industrial Coatings improved 3% to $1.64 billion. Volume grew 5%, but this was offset by slightly weaker pricing and divestitures. Automotive OEMs posted another quarter of growth as this segment outpaced the global automotive industry.

PPG Industries repurchased ~$100 million worth of shares during Q4 and retired ~$790 million worth of stock during 2025.

Click here to download our most recent Sure Analysis report on PPG (preview of page 1 of 3 shown below):

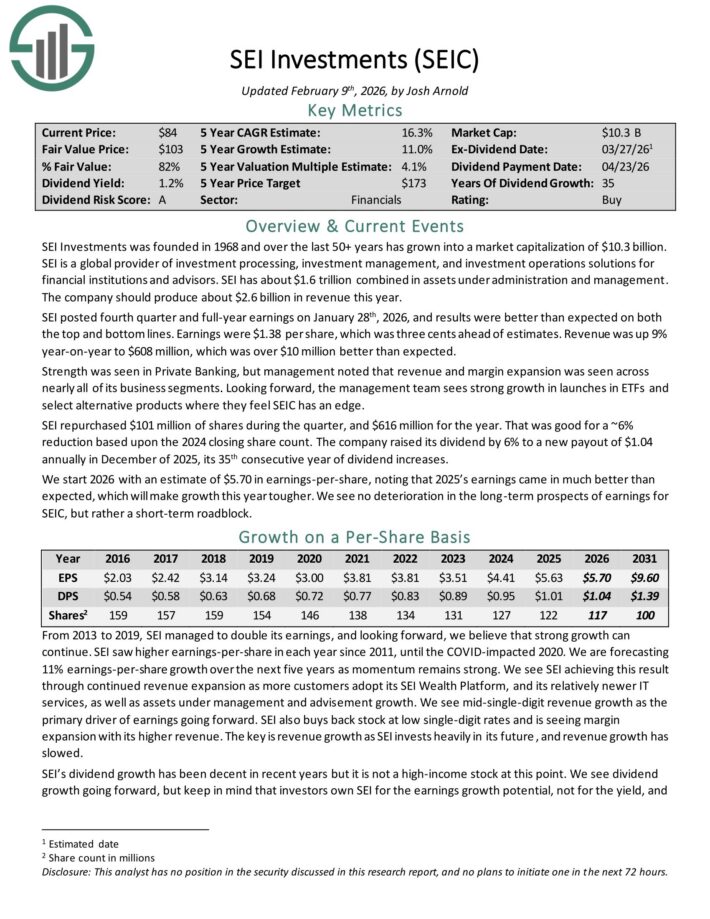

Bear Market Stock #3: SEI Investments Co. (SEIC)

Annual expected returns: 18.5%

SEI Investments was founded in 1968 and over the last 50+ years has grown into a global provider of investment processing, investment management, and investment operations solutions for financial institutions and advisors.

SEI has about $1.6 trillion combined in assets under administration and management. The company should produce about $2.6 billion in revenue this year.

SEI posted fourth quarter and full-year earnings on January 28th, 2026, and results were better than expected on both the top and bottom lines. Earnings were $1.38 per share, which was three cents ahead of estimates.

Revenue was up 9% year-on-year to $608 million, which was over $10 million better than expected. Strength was seen in Private Banking, but management noted that revenue and margin expansion was seen across nearly all of its business segments.

Looking forward, the management team sees strong growth in launches in ETFs and select alternative products where they feel SEIC has an edge.

SEI repurchased $101 million of shares during the quarter, and $616 million for the year. That was good for a ~6% reduction based upon the 2024 closing share count.

The company raised its dividend by 6% to a new payout of $1.04 annually in December of 2025, its 35th consecutive year of dividend increases.

We start 2026 with an estimate of $5.70 in earnings-per-share, noting that 2025’s earnings came in much better than expected, which will make growth this year tougher.

Click here to download our most recent Sure Analysis report on SEIC (preview of page 1 of 3 shown below):

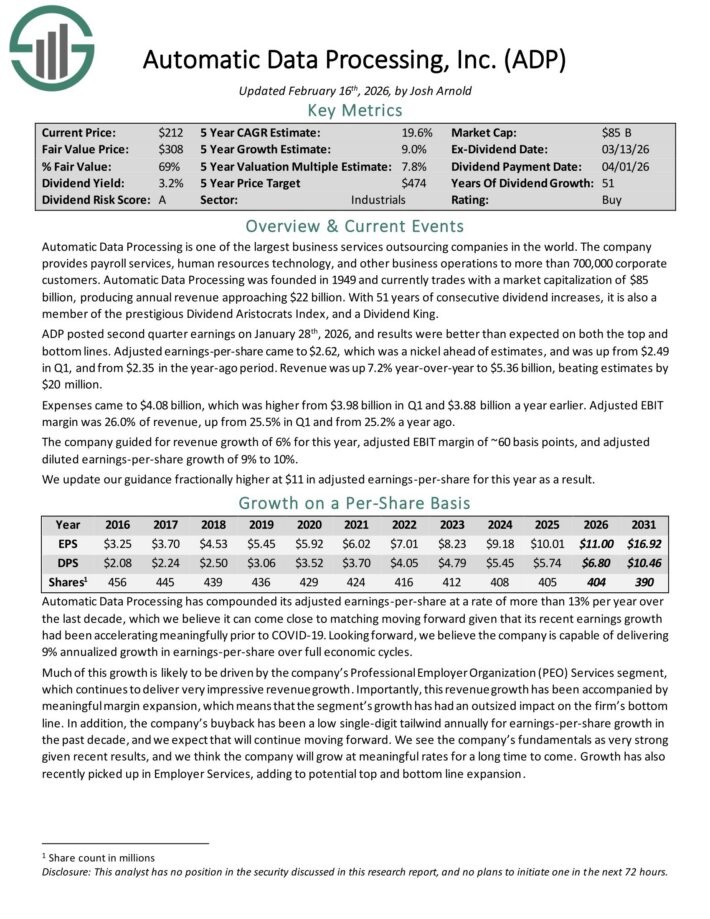

Bear Market Stock #2: Automatic Data Processing (ADP)

Annual expected returns: 20.5%

Automatic Data Processing is one of the largest business services outsourcing companies in the world. The company provides payroll services, human resources technology, and other business operations to more than 700,000 corporate customers.

ADP posted second quarter earnings on January 28th, 2026, and results were better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to $2.62, which was a nickel ahead of estimates, and was up from $2.49 in Q1, and from $2.35 in the year-ago period. Revenue was up 7.2% year-over-year to $5.36 billion, beating estimates by $20 million.

Expenses came to $4.08 billion, which was higher from $3.98 billion in Q1 and $3.88 billion a year earlier. Adjusted EBIT margin was 26.0% of revenue, up from 25.5% in Q1 and from 25.2% a year ago.

The company guided for revenue growth of 6% for this year, adjusted EBIT margin of ~60 basis points, and adjusted diluted earnings-per-share growth of 9% to 10%.

Click here to download our most recent Sure Analysis report on ADP (preview of page 1 of 3 shown below):

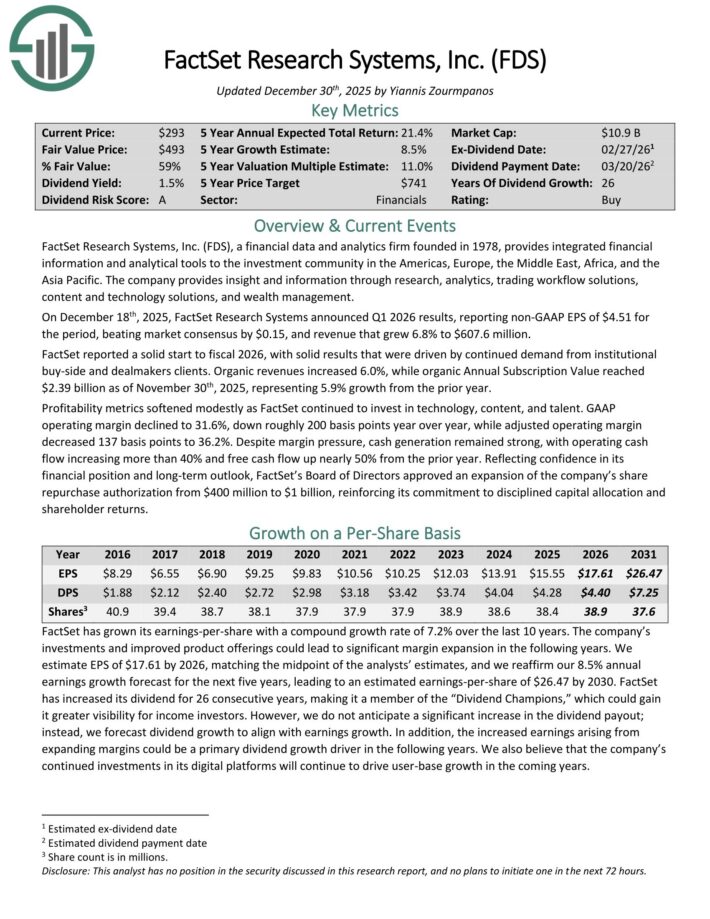

Bear Market Stock #1: Factset Research Systems (FDS)

Annual expected returns: 27.7%

FactSet Research Systems, a financial data and analytics firm founded in 1978, provides integrated financial information and analytical tools to the investment community in the Americas, Europe, the Middle East, Africa, and Asia-Pacific.

The company provides insight and information through research, analytics, trading workflow solutions, content and technology solutions, and wealth management.

On December 18th, 2025, FactSet Research Systems announced Q1 2026 results, reporting non-GAAP EPS of $4.51 for the period, beating market consensus by $0.15, and revenue that grew 6.8% to $607.6 million.

FactSet reported a solid start to fiscal 2026, with solid results that were driven by continued demand from institutional buy-side and dealmakers clients.

Organic revenues increased 6.0%, while organic Annual Subscription Value reached $2.39 billion as of November 30th, 2025, representing 5.9% growth from the prior year.

Profitability metrics softened modestly as FactSet continued to invest in technology, content, and talent. GAAP operating margin declined to 31.6%, down roughly 200 basis points year over year, while adjusted operating margin decreased 137 basis points to 36.2%.

Despite margin pressure, cash generation remained strong, with operating cash flow increasing more than 40% and free cash flow up nearly 50% from the prior year.

Reflecting confidence in its financial position and long-term outlook, FactSet’s Board of Directors approved an expansion of the company’s share repurchase authorization from $400 million to $1 billion.

Click here to download our most recent Sure Analysis report on FDS (preview of page 1 of 3 shown below):

Final Thoughts

The various lists of stocks by length of dividend history are a good resource for investors who focus on high-quality dividend stocks.

In order for a company to raise its dividend for at least 25 years, it must have durable competitive advantages, highly profitable businesses, and leadership positions in their respective industries.

They also have long-term growth potential and the ability to navigate recessions while continuing to raise their dividends.

The top 7 Dividend Champions presented in this article have long histories of dividend growth, and the combination of high dividend yields, low valuations, and future earnings growth potential make them attractive buys right now.

Additional Reading

The Dividend Champions list is not the only way to quickly screen for stocks that regularly pay rising dividends.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

(Rookie Reply)")

{kind=link}