Updated on March 18th, 2026 by Nathan Parsh

The Dividend Aristocrats are 69 companies in the S&P 500 Index that have raised their dividends for at least 25 years in a row. Over the decades, many of these companies have become huge multi-national corporations.

You can see the full list of all 69 Dividend Aristocrats here.

We created a full list of all Dividend Aristocrats and important financial metrics like price-to-earnings ratios and dividend yields. You can download your copy of the Dividend Aristocrats list by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Kenvue Inc. (KVUE) is a recent addition to the Dividend Aristocrats list, having been spun off from former parent company Johnson & Johnson (JNJ) in 2023.

As a spin-off, Kenvue carries its former parent company’s dividend growth history, and is a Dividend Aristocrat.

This article will analyze Kenvue’s business model, future growth catalysts, and expected returns.

Business Overview

Kenvue operates in the healthcare sector as a consumer products manufacturer. In May 2023, Kenvue was spun off from Johnson & Johnson. Now, Kenvue operates three segments: Self Care, Skin Health & Beauty, and Essential Health.

Self-care’s product portfolio includes cough, cold, allergy, smoking cessation, and pain care products, among others. Skin Health & Beauty holds products for the face, body, hair, and sun.

Essential Health contains products for women’s health, wound care, oral care, and baby care. Kenvue’s well-known brands include Tylenol, Listerine, Band-Aid, Neutrogena, Nicorette, and Zyrtec.

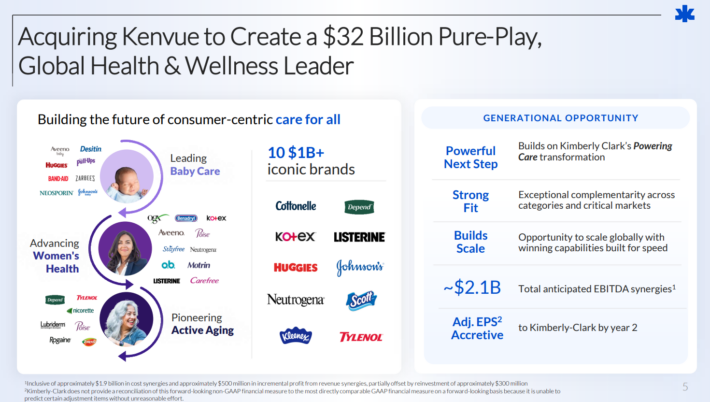

On November 3rd, 2025, it was announced that Kimberly-Clark Corporation (KMB) had agreed to purchase Kenvue.

Source: Investor Presentation

The enterprise value of the acquisition is $48.7 billion. Shareholders approved the deal on January 29th, 2026 and thedeal is still expected to close in the second half of this year.

On February 17th, 2026, Kenvue reported fourth-quarter and full year earnings results.

For the quarter, revenue increased 3.3% to $3.78 billion, which was $90 million better than expected. Adjusted earnings-per-share of $0.27 compared favorably to $0.26 last year and was $0.05 ahead of estimates. For the year, revenue declined 2.1% to $15.1 billion while adjusted earnings-per-share of $1.08 fell from $1.14 in 2024.

Organic sales increased 1.2% for the quarter, but was down 2.2% for the year. For the quarter, currency exchange added 2.1% to results while volume fell 1.1% and favorable value realization acted as a 2.3% tailwind to results. Organic revenue for Self-Care grew 1.5%, Skin Health and Beauty improved 2.9%, and Essential Health was higher by 6.1%. Gross profit margin improved 10 basis points to 58.8%.

Kenvue did not provide guidance for 2026 due to the pending transaction with Kimberly-Clark. We forecast that the company would earn $1.12 per share this year.

Growth Prospects

Prior to the spin-off, Johnson & Johnson produced annual earnings growth of 7% from 2013 to 2022, as the company’s diversification allowed it to be one of the more stable companies in the marketplace.

Today, Kenvue consists of just the consumer products businesses, which have often produced the lowest growth rates.

For its part, Kenvue management expects the company to generate organic revenue growth around 3%- 4% per year over the long term. Therefore, we expect Kenvue to grow earnings-per-share by 3% annually through 2031.

Johnson & Johnson’s dividend growth streak of more than six decades is one of the longest in the marketplace. Including the company’s dividend increase announced last summer, Kenvue has a dividend growth streak of 63 years. This qualifies Kenvue as both a Dividend King and a Dividend Aristocrat.

We believe that the penchant for dividend growth is part of Kenvue’s business DNA.

Competitive Advantages & Recession Performance

Kenvue’s former parent company Johnson & Johnson has proven to be one of the most successful companies at navigating recessions.

Though Kenvue no longer benefits from its parent company’s diversification, we believe that it would prove equally effective at handling economic downturns.

Since Kenvue was a subsidiary of Johnson & Johnson during the Great Recession of 2008-2009, there is no data on its earnings-per-share performance during that time.

However, investors can reasonably infer that Kenvue would display a similar degree of resilience during recessions as its former parent company.

The company’s products, such as Band-Aid and Tylenol, are needed regardless of the state of the economy as they directly affect consumers’ health and well-being. As trusted products, they would like to continue to perform well even under adverse conditions.

Overall, Kenvue should continue to raise its dividend for many more years thanks to its low payout ratio, decent recessions resilience, and healthy balance sheet.

Valuation & Expected Returns

We expect Kenvue to generate adjusted earnings-per-share of $1.12 for 2026. Therefore, shares of Kenvue currently trade for a price-to-earnings ratio of 15.7.

For context, Johnson & Johnson shares have an average price-to-earnings ratio of close to 19 since 2013.

Countering the fact that Kenvue holds some of the industry-leading brands and that its products were lower-margin businesses within the parent company, we have a target price-to-earnings ratio of 14 for the stock.

This implies a future headwind from P/E multiple contraction. Therefore, if the stock were to reach our target multiple by 2031, valuation could reduce annual returns by 2.2%. EPS growth (estimated at 3% per year) and the dividend yield (4.7% currently) will generate positive returns.

Putting it all together, total returns would be 5.3% annually through 2031, which earns Kenvue a hold rating.

Final Thoughts

Kenvue is a relatively new addition to the Dividend Aristocrats list. After decades as part of Johnson & Johnson, Kenvue became an independent entity in 2023.

While we find the legacy business recession-resistant and the high dividend yield attractive for income investors, the total return profile results in a hold rating for shares of Kenvue. However, these returns are speculative as Kimberly-Clark’s purchase of the company will likely close later this year.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

{kind=link}