Updated on March 12th, 2026 by Nathan Parsh

When it comes to dividend growth stocks, the Dividend Aristocrats are the “cream of the crop.” These are stocks in the S&P 500 Index, with 25+ consecutive years of dividend increases. Additionally, the Dividend Aristocrats must meet certain market cap and liquidity requirements.

It is relatively difficult to become a Dividend Aristocrat, which is why only 69 of them exist. With that in mind, we created a full list of all 69 Dividend Aristocrats.

You can download your copy of the Dividend Aristocrats list, along with important metrics like price-to-earnings ratios and dividend yields, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

At the same time, Real Estate Investment Trusts (REITs) seem like natural fits for the Dividend Aristocrats Index. REITs are required to distribute at least 90% of their earnings to shareholders. And yet, there are only 3 REITs on the list of Dividend Aristocrats, including Federal Realty Investment Trust (FRT).

The reason for the relative lack of REITs in the Dividend Aristocrats Index is primarily due to the high payout requirement of REITs. It’s challenging to grow dividends every year when the bulk of income is already being distributed, as this leaves little margin for error.

Federal Realty has a very impressive dividend history, particularly for a REIT. Federal Realty has increased its dividend for 58 years in a row, making it a Dividend King as well.

This article will discuss the only REIT on the Dividend Aristocrats and the Dividend Kings list.

Business Overview

Federal Realty was founded in 1962. Federal Realty’s business model is to own and rent out real estate properties as a Real Estate Investment Trust. It uses a significant portion of its rental income and external financing to acquire new properties.

This helps create a “snowball” effect of rising income over time.

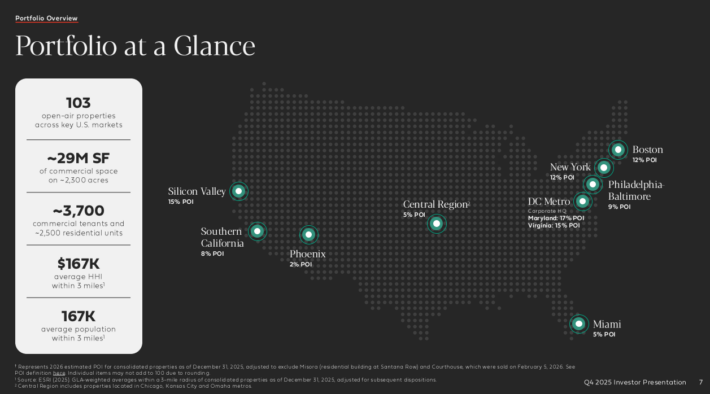

Federal Realty primarily owns shopping centers. However, it also operates in the redevelopment of multi-purpose properties, including retail, apartments, and condominiums.

Source: Investor Presentation

The portfolio is highly diversified in terms of the tenant base. Federal Realty also has a high-quality tenant portfolio.

The trust’s investment strategy is to pursue densely populated, affluent communities with high commercial and residential real estate demand. This strategy has fueled strong growth over the decades.

Growth Prospects

Federal Realty Investment Trust released its fourth-quarter earnings report for 2025 on February 12th, 2026. Federal Realty Investment Trust reported strong fourth-quarter 2025 results, with funds-from-operation (FFO) of $1.84, which compared to $1.73 in the prior year. Revenue grew 7.9% to $335.8 million.

For the year, FFO grew 6.6% to $7.22 per share while revenue increased 6.4% to $1.28 million.

This performance was particularly impressive, as the company achieved record leasing activity of 2.5 million square feet of retail space and generated its strongest comparable rent spreads in over a decade at 15% on a cash basis and 27% on a straight line basis, reflecting robust tenant demand and pricing power. Portfolio occupancy reached 94.5% with a 96.6% leased rate, further highlighting the attractiveness of Federal Realty’s open-air shopping centers and mixed-use properties.

Additionally, the company deployed $340 million into acquisitions that added nearly one million square feet and committing $280 million to new residential development projects.

For 2026, Federal Realty Investment Trust guided towards FFO of $7.42 to $7.52 per share, implying low single-digit growth from last year.

Competitive Advantages & Recession Performance

One way REITs establish a competitive advantage is by investing in the highest-quality portfolios. Federal Realty has done this by focusing on affluent areas of the country where demand exceeds supply. This is also how it can continue to boost its cash basis rollover growth over time; it owns properties in the most desirable areas, and tenants are willing to pay more to gain access to the best consumers.

The trust also has a very diversified portfolio that helps protect it from a downturn in any one area.

Source: Investor Presentation

Federal Realty benefits from a favorable economic backdrop, with high occupancy rates and the ability to raise rents over time.

Another competitive advantage for Federal Realty is a strong balance sheet. The trust’s senior unsecured debt holds a credit rating of A- from Standard & Poor’s, solidly investment-grade and a high rating for a REIT.

A strong balance sheet helps keep borrowing costs low, which is critical for the REIT business model.

These competitive strengths allowed Federal Realty to perform well during the last recession. Federal Realty’s FFO during the Great Recession is shown below:

2007 FFO-per-share of $3.63

2008 FFO-per-share of $3.87 (6.6% increase)

2009 FFO-per-share of $3.87 (flat)

2010 FFO-per-share of $3.88 (0.3% increase)

2011 FFO-per-share of $4.00 (3% increase)

FFO either held steady or increased during each year of the recession. This was a remarkable achievement that speaks to the strength of the business.

We expect Federal Realty to hold up well during the next downturn, but we also note that growth will certainly slow during such a period.

Valuation & Expected Returns

Based on 2026 expected FFO-per-share of $7.45, Federal Realty stock trades for a price-to-FFO ratio of 14.2. Investors can think of this as similar to a price-to-earnings ratio.

On a valuation basis, Federal Realty appears overvalued. Our fair value estimate is a P/FFO ratio of 12.0, implying downside potential due to the high valuation multiple.

Therefore, future returns could be reduced by 3.3% per year over the next five years if the P/FFO ratio declines from 14.2 to 12.0.

FFO-per-share growth, expected to reach 4.3% per year, plus the 4.3% current dividend yield and the valuation headwind, results in total expected returns of 4.9% per year.

Federal Realty helps make up for this rate of return with strong dividend growth and its impeccable track record. It has increased its dividend for nearly 60 years in a row.

Final Thoughts

Investors flock to REITs for dividends, and with high yields across the asset class, it is easy to see why they are so popular for income investors.

Federal Realty does have a generous dividend yield, particularly compared to the average name in the S&P 500. The stock does consistently trade for a relatively high valuation. However, high-quality businesses tend to sport above-average valuations.

Federal Realty is a strong choice for dividend investors given its history, but we rate the stock a hold due to its projected total returns.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

{kind=link}