Updated on March 3rd, 2023 by Bob Ciura

Income investors are always on the hunt for high-quality dividend stocks. There are many ways to measure high-quality stocks. One way for investors to find great dividend stocks is to focus on those with the longest histories of raising dividends.

With this in mind, we created a downloadable list of all 150 Dividend Champions.

You can download your free copy of the Dividend Champions list, along with relevant financial metrics like price-to-earnings ratios, dividend yields, and payout ratios, by clicking on the link below:

Investors are likely familiar with the Dividend Aristocrats, a group of 65 stocks in the S&P 500 Index with 25+ consecutive years of dividend increases. Meanwhile, investors should also familiarize themselves with the Dividend Champions, which have also raised their dividends for at least 25 years in a row.

While their length of dividend increases is the same, leading to some overlap, there are also some important differences between the Dividend Aristocrats and Dividend Champions. As a result, the Dividend Champions list is much more expansive. There are many high-quality Dividend Champions that are not included on the Dividend Aristocrats list.

This article will discuss large cap stocks, and an analysis of our top 7 Dividend Champions, ranked according to expected total returns in the Sure Analysis Research Database.

Table of Contents

You can instantly jump to any specific section of the article by clicking on the links below:

Overview of Dividend Champions

The requirement to become a Dividend Champion is simple: 25+ years of consecutive annual dividend increases. The Dividend Aristocrats have the same requirement when it comes to number of years, but with a few additional requirements.

To be a Dividend Aristocrat, a company must also be included in the S&P 500 Index, must have a float-adjusted market cap of at least $3 billion, and must have an average daily value traded of at least $5 million. These added requirements preclude many companies that possess a sufficient track record of annual dividend increases, but do not qualify based on market cap or liquidity reasons.

As a result, while there is some overlap between the Dividend Aristocrats and the Dividend Champions, there are also many Dividend Champions that are not Dividend Aristocrats. Income investors might want to consider these stocks due to their impressive histories of annual dividend increases, so we have compiled them in the downloadable spreadsheet above.

In addition, we have ranked the top 7 Dividend Champions according to total expected annual returns over the next five years. Our top 7 Dividend Champions right now are ranked below.

The Top 7 Dividend Champions To Buy Right Now

The following 7 stocks represent Dividend Champions with at least 25 consecutive years of dividend increases, but they also have durable competitive advantages, long-term growth potential, and high expected total returns.

Stocks have been ranked by expected total annual return over the next five years, from lowest to highest.

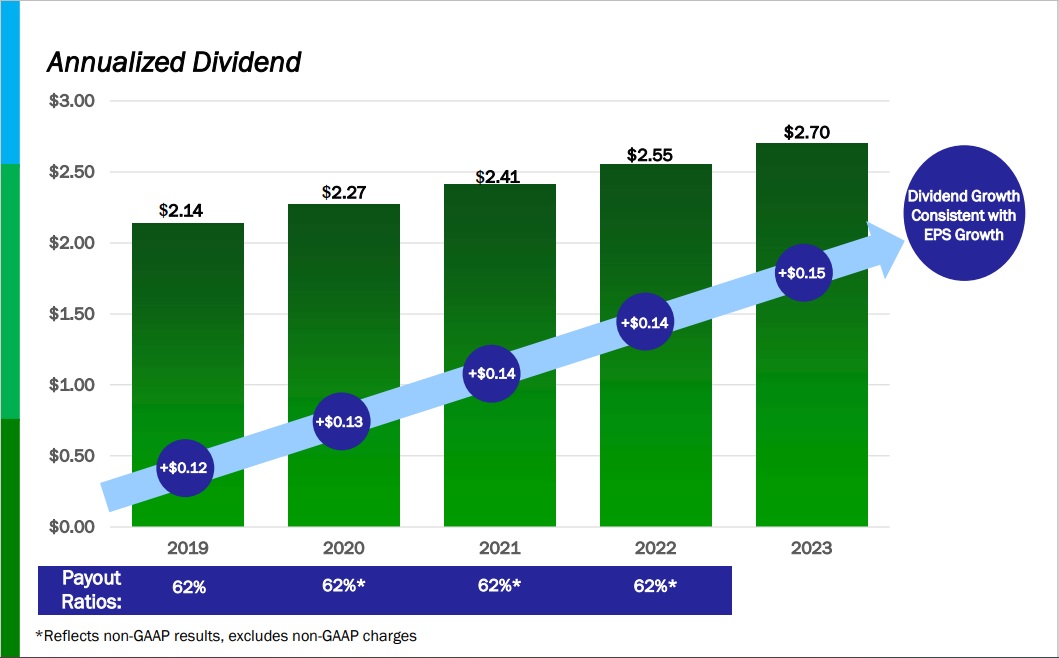

Top Dividend Champion #7: Eversource Energy (ES)

5-year expected returns: 14.0%

Eversource Energy is a diversified holding company with subsidiaries that provide regulated electric, gas, and water distribution service in the Northeast U.S. The company’s utilities serve more than 4 million customers after acquiring NStar’s Massachusetts utilities in 2012, Aquarion in 2017, and Columbia Gas in 2020.

The company has increased its dividend for 25 consecutive years.

Source: Investor Presentation

On February 13th, 2023, Eversource Energy released its fourth quarter 2022 results for the period ending December 31st, 2022. For the quarter, the company reported revenue of $3.0 billion, an increase of 22.1% versus same quarter of last year. The company reported earnings of $320.2 million and earnings-per-share of $0.92 compared with earnings of $306.7 million and earnings-per-share of $0.89 in the prior year. Eversource Energy earned $1,419.9 million, or $4.09 per share, for the full-year 2022.

The company expects earnings per share to grow at a 5% to 7% compound annual rate from 2023 through 2027, the same as for dividend growth. The company projects 2023 earnings of between $4.25 per share and $4.43 per share.

Click here to download our most recent Sure Analysis report on ES (preview of page 1 of 3 shown below):

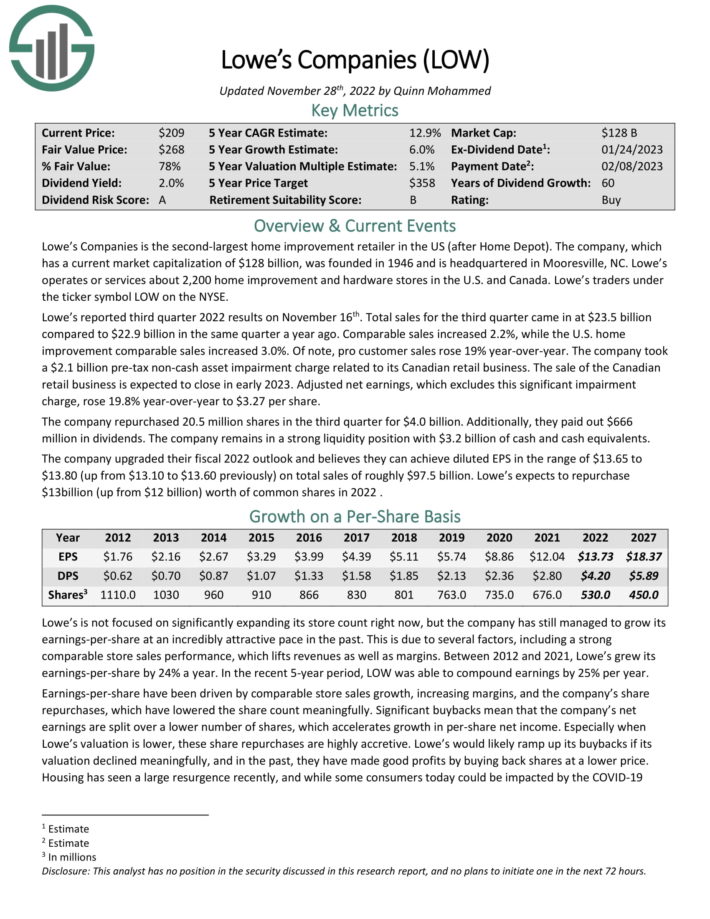

Top Dividend Champion #6: Lowe’s Companies (LOW)

5-year expected returns: 14.5%

Lowe’s Companies is the second-largest home improvement retailer in the US (after Home Depot). Lowe’s operates or services more than 2,200 home improvement and hardware stores in the U.S. and Canada.

Lowe’s reported third quarter 2022 results on November 16th. Total sales for the third quarter came in at $23.5 billion compared to $22.9 billion in the same quarter a year ago. Comparable sales increased 2.2%, while the U.S. home improvement comparable sales increased 3.0%. Of note, pro customer sales rose 19% year-over-year.

The company took a $2.1 billion pre-tax non-cash asset impairment charge related to its Canadian retail business. The sale of the Canadian retail business is expected to close in early 2023. Adjusted net earnings, which excludes this significant impairment charge, rose 19.8% year-over-year to $3.27 per share.

The combination of multiple expansion, 6% expected EPS growth and the 2.1% dividend yield lead to total expected returns of 14.1% per year.

Click here to download our most recent Sure Analysis report on Lowe’s (preview of page 1 of 3 shown below):

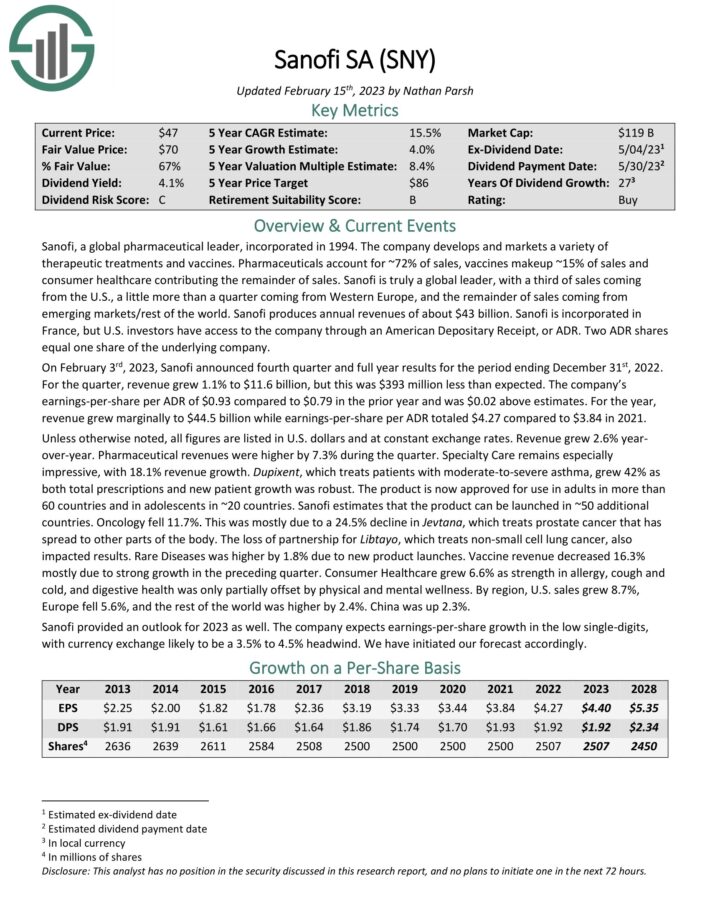

Top Dividend Champion #5: Sanofi SA (SNY)

5-year expected returns: 15.0%

Sanofi develops and markets a variety of therapeutic treatments and vaccines. Pharmaceuticals account for ~72% of sales, vaccines makeup ~15% of sales and consumer healthcare contributing the remainder of sales. Sanofi is incorporated in France, but U.S. investors have access to the company through an American Depositary Receipt, or ADR. Two ADR shares equal one share of the underlying company.

On February 3rd, 2023, Sanofi announced fourth quarter and full year results for the period ending December 31st, 2022. For the quarter, revenue grew 1.1% to $11.6 billion, but this was $393 million less than expected. The company’s earnings-per-share per ADR of $0.93 compared to $0.79 in the prior year and was $0.02 above estimates.

Source: Investor Presentation

For the year, revenue grew marginally to $44.5 billion while earnings-per-share per ADR totaled $4.27 compared to $3.84 in 2021. Unless otherwise noted, all figures are listed in U.S. dollars and at constant exchange rates. Revenue grew 2.6% year-over-year. Pharmaceutical revenues were higher by 7.3% during the quarter.

Sanofi provided an outlook for 2023 as well. The company expects earnings-per-share growth in the low single-digits.

Click here to download our most recent Sure Analysis report on Sanofi (preview of page 1 of 3 shown below):

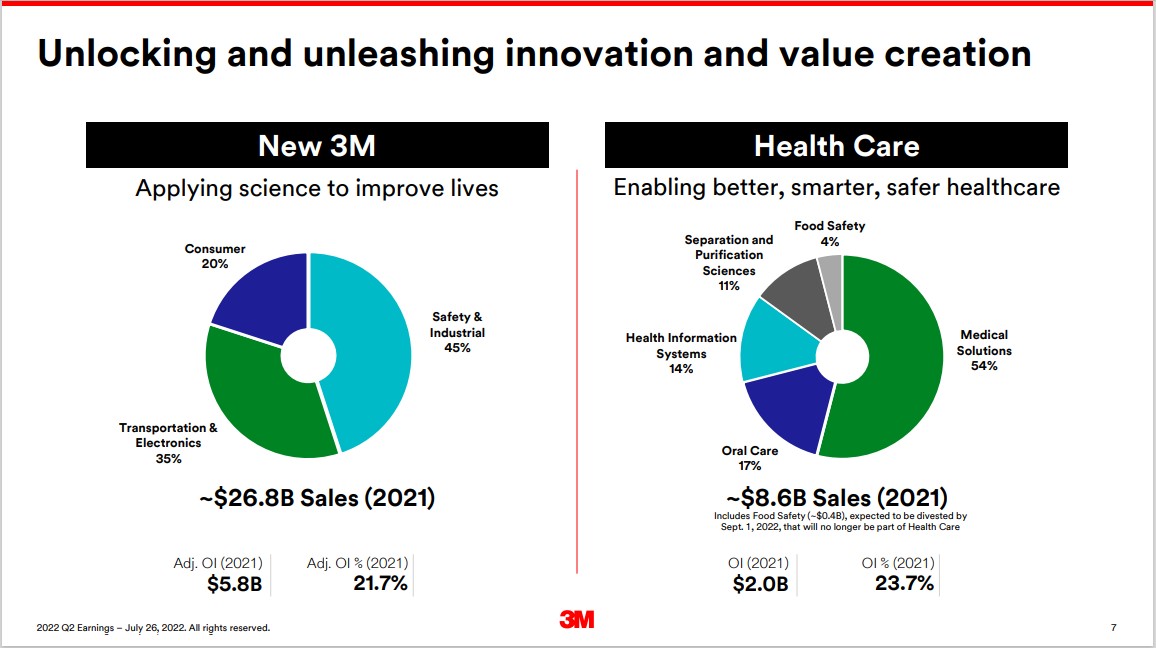

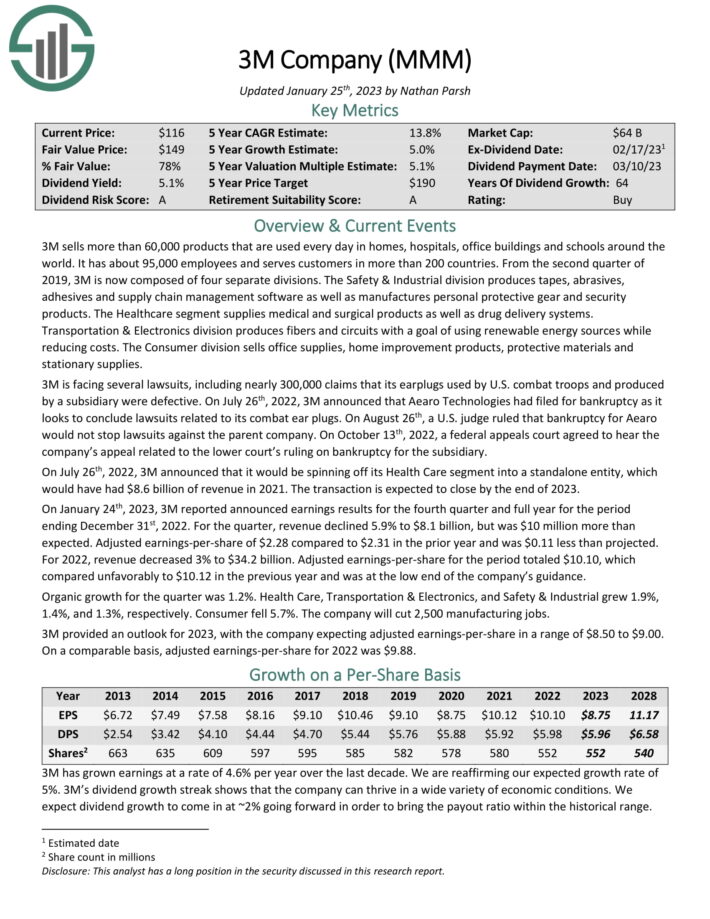

Top Dividend Champion #4: 3M Company (MMM)

5-year expected returns: 15.1%

3M sells more than 60,000 products that are used every day in homes, hospitals, office buildings and schools around the world. It has about 95,000 employees and serves customers in more than 200 countries. 3M is now composed of four separate divisions.

Source: Investor Presentation

The company also announced that it would be spinning off its Health Care segment, which would have had $8.6 billion of revenue in 2021. The transaction is expected to close by the end of 2023.

On January 24th, 2023, 3M reported announced earnings results for the fourth quarter and full year for the period ending December 31st, 2022. For the quarter, revenue declined 5.9% to $8.1 billion, but was $10 million more than expected. Adjusted earnings-per-share of $2.28 compared to $2.31 in the prior year and was $0.11 less than projected.

For 2022, revenue decreased 3% to $34.2 billion. Adjusted earnings-per-share for the period totaled $10.10, which compared unfavorably to $10.12 in the previous year and was at the low end of the company’s guidance.

Organic growth for the quarter was 1.2%. Health Care, Transportation & Electronics, and Safety & Industrial grew 1.9%, 1.4%, and 1.3%, respectively. Consumer fell 5.7%. The company will cut 2,500 manufacturing jobs. 3M provided an outlook for 2023, with the company expecting adjusted earnings-per-share in a range of $8.50 to $9.00.

Click here to download our most recent Sure Analysis report on 3M (preview of page 1 of 3 shown below):

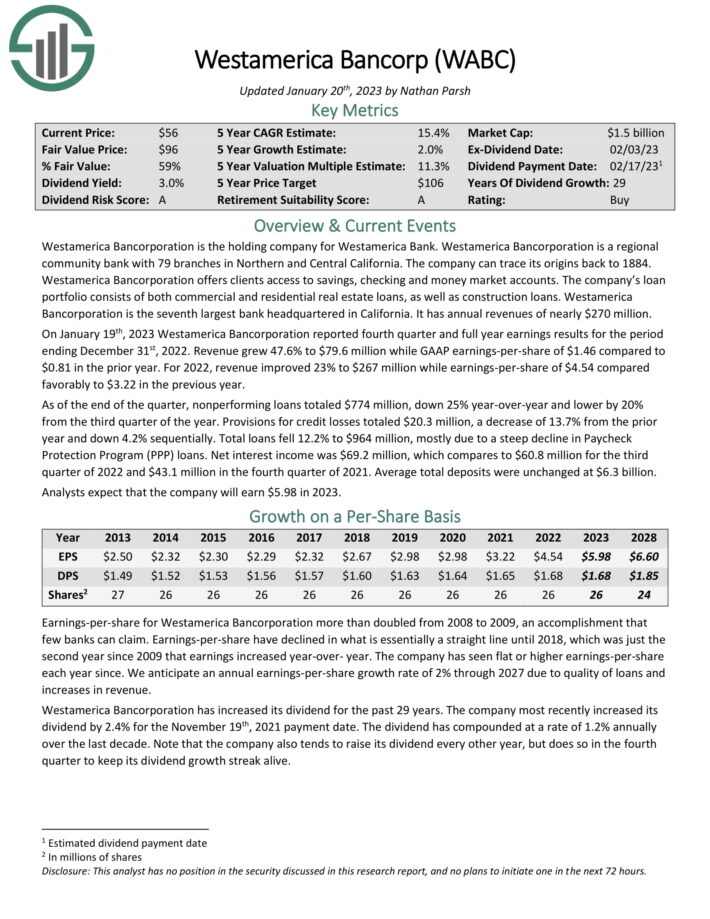

Top Dividend Champion #3: Westamerica Bancorp (WABC)

5-year expected returns: 16.0%

Westamerica Bancorporation is the holding company for Westamerica Bank. Westamerica is a regional community bank with 79 branches in Northern and Central California. The company can trace its origins back to 1884. Westamerica offers clients access to savings, checking and money market accounts.

The company’s loan portfolio consists of both commercial and residential real estate loans, as well as construction loans. Westamerica is the seventh largest bank headquartered in California. It has annual revenues of nearly $270 million.

On January 19th, 2023 Westamerica reported fourth quarter and full year earnings results. Revenue grew 47.6% to $79.6 million while GAAP earnings-per-share of $1.46 compared to $0.81 in the prior year. For 2022, revenue improved 23% to $267 million while earnings-per-share of $4.54 compared favorably to $3.22 in the previous year.

As of the end of the quarter, nonperforming loans totaled $774 million, down 25% year-over-year and lower by 20% from the third quarter of the year. Provisions for credit losses totaled $20.3 million, a decrease of 13.7% from the prior year and down 4.2% sequentially. Total loans fell 12.2% to $964 million, mostly due to a steep decline in Paycheck Protection Program (PPP) loans.

Net interest income was $69.2 million, which compares to $60.8 million for the third quarter of 2022 and $43.1 million in the fourth quarter of 2021. Average total deposits were unchanged at $6.3 billion. Analysts expect that the company will earn $5.98 in 2023.

The company has a long history of paying dividends and has increased its payout for 29 consecutive years. Shares currently yield 3%. We expect 2% annual EPS growth, while the stock also appears to be significantly undervalued. Total returns are estimated at 15.2% per year.

Click here to download our most recent Sure Analysis report on WABC (preview of page 1 of 3 shown below):

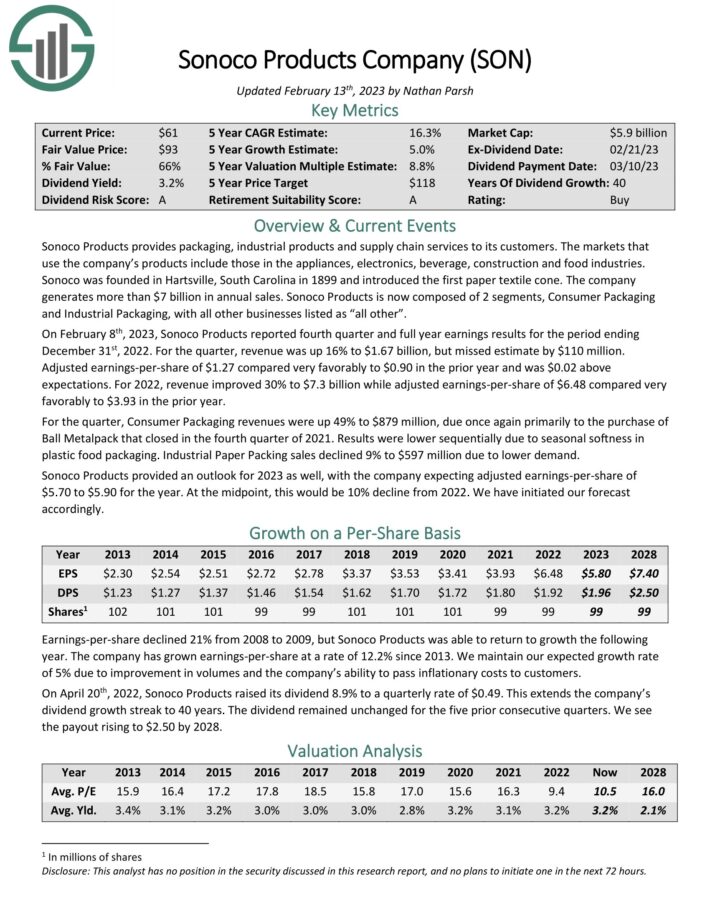

Top Dividend Champion #2: Sonoco Products Company (SON)

5-year expected returns: 16.8%

Sonoco Products provides packaging, industrial products and supply chain services to its customers. The markets that use the company’s products include those in the appliances, electronics, beverage, construction and food industries. The company generates about $7.2 billion in annual sales.

Sonoco Products is now composed of 2 core segments, Consumer Packaging and Industrial Packaging, with all other businesses listed as “all other”.

Source: Investor Presentation

On February 8th, 2023, Sonoco Products reported fourth quarter and full year earnings results for the period ending December 31st, 2022. For the quarter, revenue was up 16% to $1.67 billion, but missed estimate by $110 million. Adjusted earnings-per-share of $1.27 compared very favorably to $0.90 in the prior year and was $0.02 above expectations.

For 2022, revenue improved 30% to $7.3 billion while adjusted earnings-per-share of $6.48 compared very favorably to $3.93 in the prior year.

For the quarter, Consumer Packaging revenues were up 49% to $879 million, due once again primarily to the purchase of Ball Metalpack that closed in the fourth quarter of 2021. Results were lower sequentially due to seasonal softness in plastic food packaging. Industrial Paper Packing sales declined 9% to $597 million due to lower demand.

Sonoco Products provided an outlook for 2023 as well, with the company expecting adjusted earnings-per-share of $5.70 to $5.90 for the year. At the midpoint, this would be 10% decline from 2022.

Click here to download our most recent Sure Analysis report on SON (preview of page 1 of 3 shown below):

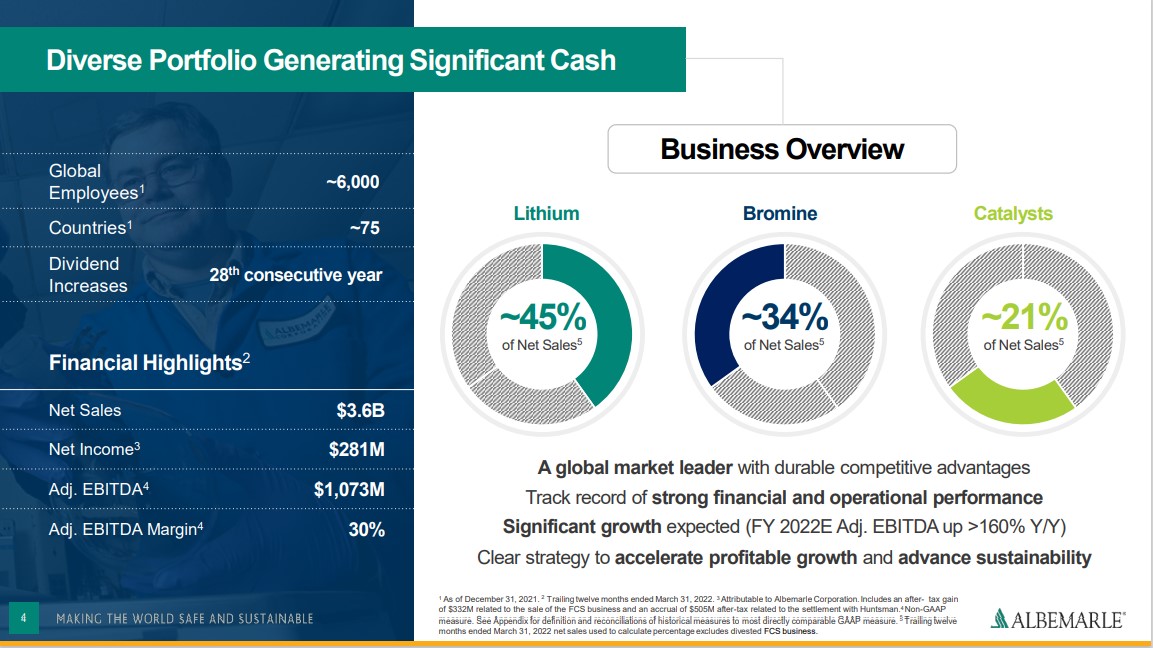

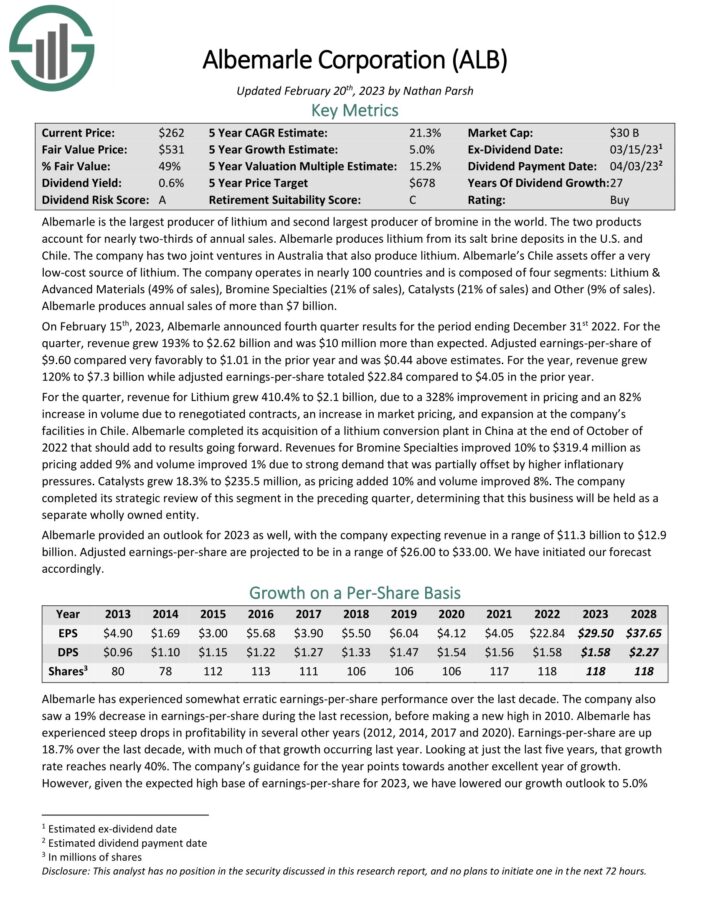

Top Dividend Champion #1: Albemarle Corporation (ALB)

5-year expected returns: 22.4%

Albemarle is the largest producer of lithium and second largest producer of bromine in the world. The two products account for nearly two-thirds of annual sales. Albemarle produces lithium from its salt brine deposits in the U.S. and Chile. The company has two joint ventures in Australia that also produce lithium. Albemarle’s Chile assets offer a very low-cost source of lithium.

Related: 2023 Lithium Stocks List

The company operates in nearly 100 countries and is composed of four segments: Lithium & Advanced Materials (49% of sales), Bromine Specialties (21% of sales), Catalysts (21% of sales) and Other (9% of sales). Albemarle produces annual sales of more than $7.5 billion.

Source: Investor Presentation

Albemarle produces annual sales of $7.3 billion. It is one of the top lithium stocks.

On February 15th, 2023, Albemarle announced fourth quarter results for the period ending December 31st 2022. For the quarter, revenue grew 193% to $2.62 billion and was $10 million more than expected. Adjusted earnings-per-share of $9.60 compared very favorably to $1.01 in the prior year and was $0.44 above estimates.

For the year, revenue grew 120% to $7.3 billion while adjusted earnings-per-share totaled $22.84 compared to $4.05 in the prior year. For the quarter, revenue for Lithium grew 410.4% to $2.1 billion, due to a 328% improvement in pricing and an 82% increase in volume due to renegotiated contracts, an increase in market pricing, and expansion at the company’s facilities in Chile.

Albemarle completed its acquisition of a lithium conversion plant in China at the end of October of 2022 that should add to results going forward.

Click here to download our most recent Sure Analysis report on Albemarle (preview of page 1 of 3 shown below):

Final Thoughts

The various lists of stocks by length of dividend history are a good resource for investors who focus on high-quality dividend stocks.

In order for a company to raise its dividend for at least 25 years, it must have durable competitive advantages, highly profitable businesses, and leadership positions in their respective industries.

They also have long-term growth potential and the ability to navigate recessions while continuing to raise their dividends.

The top 7 Dividend Champions presented in this article have long histories of dividend growth, and the combination of high dividend yields, low valuations, and future earnings growth potential make them attractive buys right now.

The Dividend Champions list is not the only way to quickly screen for stocks that regularly pay rising dividends.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

{kind=link}