Published on September 29th, 2025 by Bob Ciura

Income investors often look to real estate investment trusts, or REITs, as these stocks usually have very high yields.

Real estate investment trusts – or REITs, for short – can be fantastic securities for generating meaningful portfolio income. REITs widely offer higher dividend yields than the average stock.

While the S&P 500 Index on average yields less than 2% right now, it is relatively easy to find REITs with dividend yields of 5% or higher.

With this in mind, we created a list of over 200 REITs.

You can download your free 200+ REIT list (along with important financial metrics like dividend yields and payout ratios) by clicking on the link below:

Looking more specifically at a certain part of the REIT industry, we feel that the healthcare REIT industry is very attractive for income investors.

These REITs own a variety of healthcare properties, including life science buildings, senior housing, skilled nursing facilities, and more.

Healthcare REITs have a favorable long-term growth trajectory because the population continues to get older in the U.S., with those over 80 expected to make up more than half of the country’s population by 2030.

Many of those people will require housing and medical treatment as they age. Combine this fact with a shortage of healthcare properties, and the economic outlook for the major healthcare REITs is very promising.

In addition to the downloadable Excel sheet of all REITs, this article ranks the 8 highest-yielding healthcare REITs in the Sure Analysis Research Database.

Table Of Contents

In addition to the full downloadable Excel spreadsheet, this article covers our top 8 heatlhcare REITs today, as ranked by their current dividend yield.

The table of contents below allows for easy navigation.

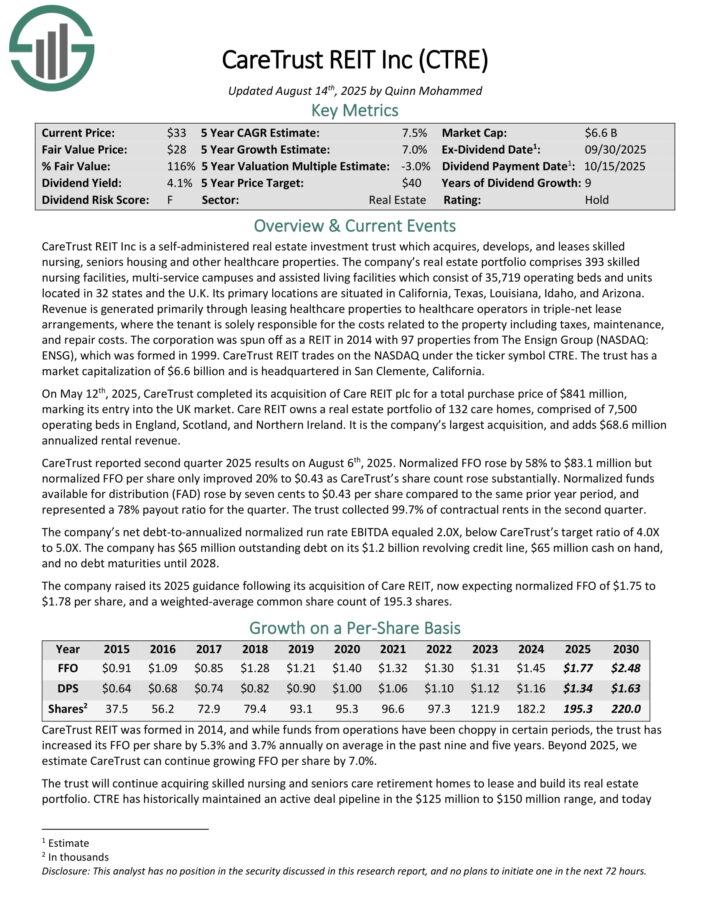

Healthcare REIT #8: CareTrust REIT (CTRE)

CareTrust REIT Inc is a self-administered real estate investment trust which acquires, develops, and leases skilled nursing, seniors housing and other healthcare properties.

The company’s real estate portfolio comprises 393 skilled nursing facilities, multi-service campuses and assisted living facilities which consist of 35,719 operating beds and units located in 32 states and the U.K. Its primary locations are situated in California, Texas, Louisiana, Idaho, and Arizona.

Revenue is generated primarily through leasing healthcare properties to healthcare operators in triple-net lease arrangements.

On May 12th, 2025, CareTrust completed its acquisition of Care REIT plc for a total purchase price of $841 million, marking its entry into the UK market.

Care REIT owns a real estate portfolio of 132 care homes, comprised of 7,500 operating beds in England, Scotland, and Northern Ireland. It is the company’s largest acquisition, and adds $68.6 million annualized rental revenue.

CareTrust reported second quarter 2025 results on August 6th, 2025. Normalized FFO rose by 58% to $83.1 million but normalized FFO per share only improved 20% to $0.43 as CareTrust’s share count rose substantially.

Normalized funds available for distribution rose by seven cents to $0.43 per share compared to the same prior year period, and represented a 78% payout ratio for the quarter. The trust collected 99.7% of contractual rents in the second quarter.

The company’s net debt-to-annualized normalized run rate EBITDA equaled 2.0X, below CareTrust’s target ratio of 4.0X to 5.0X.

The company has $65 million outstanding debt on its $1.2 billion revolving credit line, $65 million cash on hand, and no debt maturities until 2028.

Click here to download our most recent Sure Analysis report on CTRE (preview of page 1 of 3 shown below):

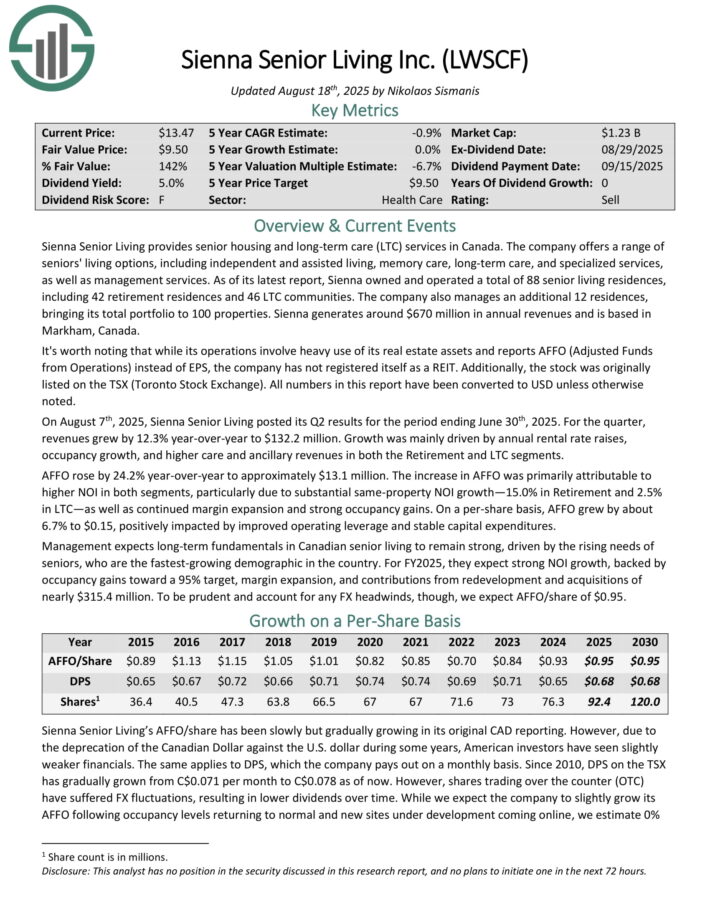

Top REIT #7: Sienna Senior Living (LWSCF)

Sienna Senior Living provides senior housing and long-term care (LTC) services in Canada. The company offers a range of seniors’ living options, including independent and assisted living, memory care, long-term care, and specialized services, as well as management services.

As of its latest report, Sienna owned and operated a total of 88 senior living residences, including 42 retirement residences and 46 LTC communities.

The company also manages an additional 12 residences, bringing its total portfolio to 100 properties. Sienna generates around $670 million in annual revenues and is based in Markham, Canada.

On August 7th, 2025, Sienna Senior Living posted its Q2 results for the period ending June 30th, 2025. For the quarter, revenues grew by 12.3% year-over-year to $132.2 million.

Growth was mainly driven by annual rental rate raises, occupancy growth, and higher care and ancillary revenues in both the Retirement and LTC segments.

AFFO rose by 24.2% year-over-year to approximately $13.1 million. The increase in AFFO was primarily attributable to higher NOI in both segments, particularly due to substantial same-property NOI growth—15.0% in Retirement and 2.5% in LTC—as well as continued margin expansion and strong occupancy gains.

On a per-share basis, AFFO grew by about 6.7% to $0.15, positively impacted by improved operating leverage and stable capital expenditures.

Management expects long-term fundamentals in Canadian senior living to remain strong, driven by the rising needs of seniors, who are the fastest-growing demographic in the country.

For FY2025, they expect strong NOI growth, backed by occupancy gains toward a 95% target, margin expansion, and contributions from redevelopment and acquisitions of nearly $315.4 million.

Click here to download our most recent Sure Analysis report on LWSCF (preview of page 1 of 3 shown below):

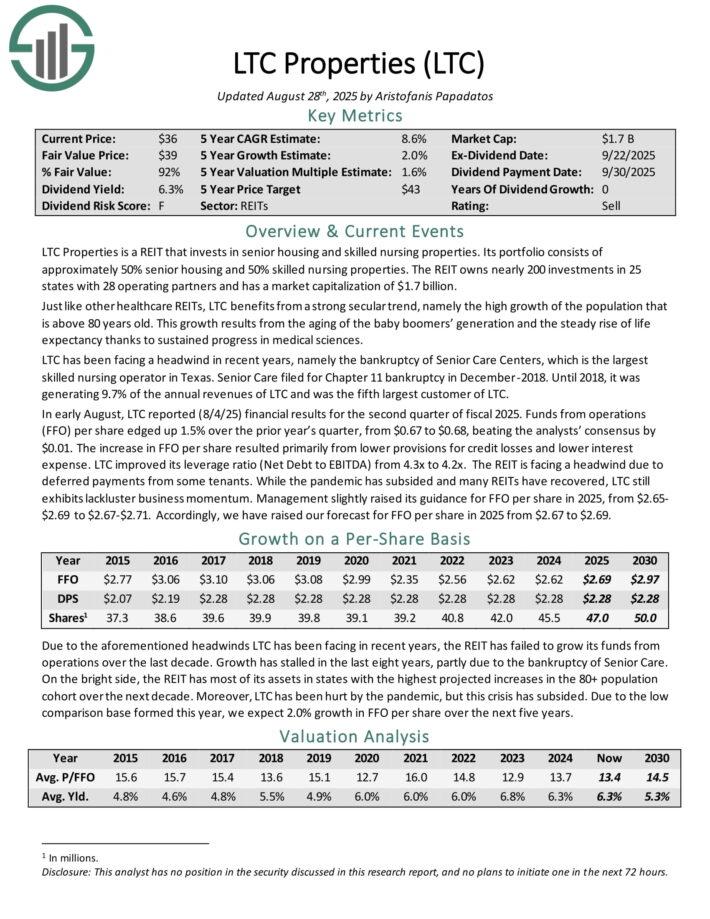

Top REIT #6: LTC Properties (LTC)

LTC Properties is a REIT that invests in senior housing and skilled nursing properties. Its portfolio consists of approximately 50% senior housing and 50% skilled nursing properties.

The REIT owns nearly 200 investments in 25 states with 28 operating partners.

In early August, LTC reported (8/4/25) financial results for the second quarter of fiscal 2025. Funds from operations (FFO) per share edged up 1.5% over the prior year’s quarter, from $0.67 to $0.68, beating the analysts’ consensus by $0.01.

The increase in FFO per share resulted primarily from lower provisions for credit losses and lower interest expense. LTC improved its leverage ratio (Net Debt to EBITDA) from 4.3x to 4.2x.

The REIT is facing a headwind due to deferred payments from some tenants. While the pandemic has subsided and many REITs have recovered, LTC still exhibits lackluster business momentum.

Management slightly raised its guidance for FFO per share in 2025, from $2.65-$2.69 to $2.67-$2.71.

Click here to download our most recent Sure Analysis report on LTC (preview of page 1 of 3 shown below):

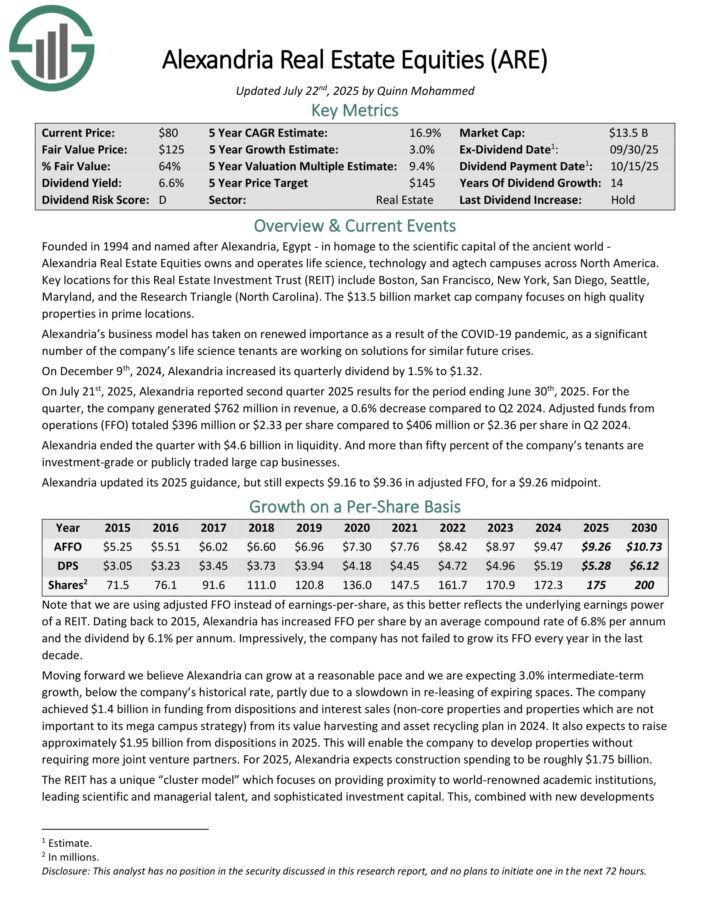

Top REIT #5: Alexandria Real Estate Equities (ARE)

Alexandria Real Estate Equities owns and operates life science, technology and agtech campuses across North America. Key locations for this Real Estate Investment Trust (REIT) include Boston, San Francisco, New York, San Diego, Seattle, Maryland, and the Research Triangle (North Carolina).

The company focuses on high quality properties in prime locations. Alexandria’s business model has taken on renewed importance as a result of the COVID-19 pandemic, as a significant number of the company’s life science tenants are working on solutions for similar future crises.

On December 9th, 2024, Alexandria increased its quarterly dividend by 1.5% to $1.32. On July 21st, 2025, Alexandria reported second quarter 2025 results for the period ending June 30th, 2025.

For the quarter, the company generated $762 million in revenue, a 0.6% decrease compared to Q2 2024.

Adjusted funds from operations (FFO) totaled $396 million or $2.33 per share compared to $406 million or $2.36 per share in Q2 2024.

Alexandria ended the quarter with $4.6 billion in liquidity. And more than fifty percent of the company’s tenants are investment-grade or publicly traded large cap businesses.

Click here to download our most recent Sure Analysis report on ARE (preview of page 1 of 3 shown below):

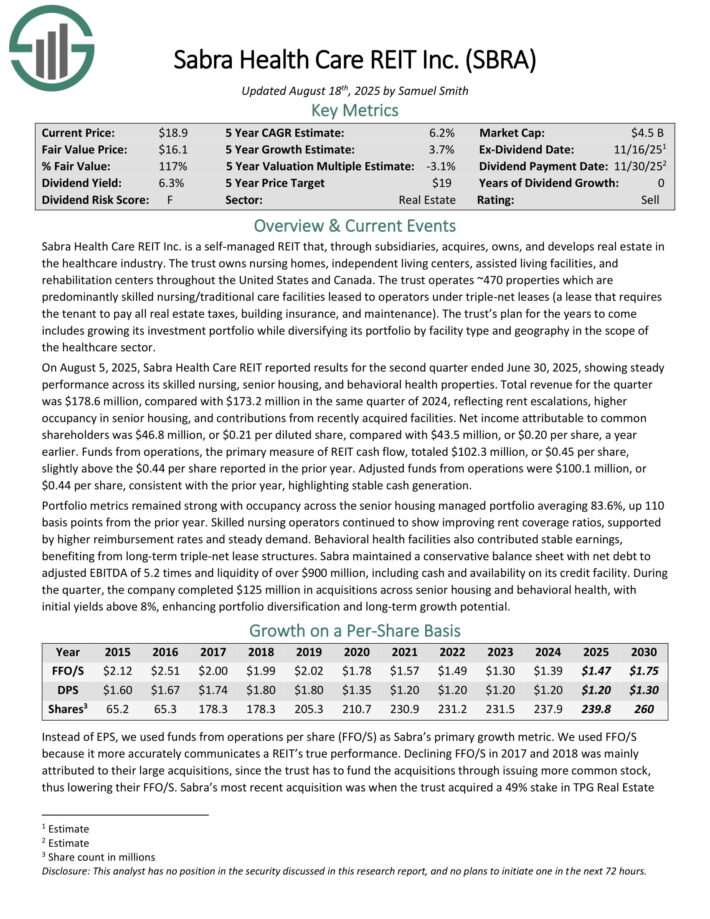

Top REIT #4: Sabra Health Care REIT (SBRA)

Sabra Health Care REIT Inc. is a self-managed REIT that, through subsidiaries, acquires, owns, and develops real estate in the healthcare industry. The trust owns nursing homes, independent living centers, assisted living facilities, and rehabilitation centers throughout the United States and Canada.

The trust operates ~470 properties which are predominantly skilled nursing/traditional care facilities leased to operators under triple-net leases (a lease that requires the tenant to pay all real estate taxes, building insurance, and maintenance).

The trust’s plan for the years to come includes growing its investment portfolio while diversifying its portfolio by facility type and geography in the scope of the healthcare sector.

On August 5, 2025, Sabra Health Care REIT reported results for the second quarter ended June 30, 2025, showing steady performance across its skilled nursing, senior housing, and behavioral health properties.

Total revenue for the quarter was $178.6 million, compared with $173.2 million in the same quarter of 2024, reflecting rent escalations, higher occupancy in senior housing, and contributions from recently acquired facilities.

Net income attributable to common shareholders was $46.8 million, or $0.21 per diluted share, compared with $43.5 million, or $0.20 per share, a year earlier.

Funds from operations totaled $102.3 million, or $0.45 per share, slightly above the $0.44 per share reported in the prior year.

Adjusted funds from operations were $100.1 million, or $0.44 per share, consistent with the prior year, highlighting stable cash generation.

Portfolio metrics remained strong with occupancy across the senior housing managed portfolio averaging 83.6%, up 110 basis points from the prior year.

Skilled nursing operators continued to show improving rent coverage ratios, supported by higher reimbursement rates and steady demand.

Click here to download our most recent Sure Analysis report on SBRA (preview of page 1 of 3 shown below):

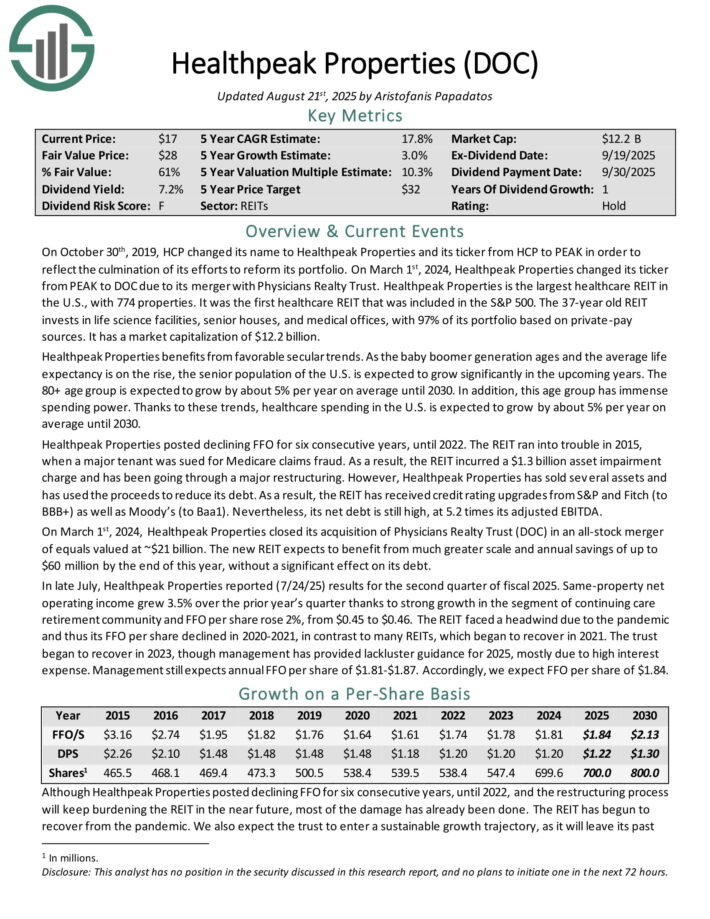

Top REIT #3: Healthpeak Properties (DOC)

Healthpeak Properties is the largest healthcare REIT in the U.S., with 774 properties. It was the first healthcare REIT that was included in the S&P 500. The 37-year old REIT invests in life science facilities, senior houses, and medical offices, with 97% of its portfolio based on private-pay sources.

On July 24th 2025, the REIT reported second-quarter financial results. Quarterly revenue of $694.35 million was in-line with analyst estimates, and represented a year-over-year decline of 0.2%.

Adjusted funds-from-operation (FFO) was $0.46 per share, up 2.2% from the same quarter last year. Adjusted FFO-per-share was also in-line with estimates. Same-store cash net operating income growth was 3.5% for the second quarter.

Investment activity for the quarter included two new development agreements with a combined projected cost of $148 million to support Northside Hospital’s continued outpatient expansion in the Atlanta market.

Healthpeak Properties also sold one outpatient medical land parcel in June 2025 and two outpatient medical buildings in July 2025 for combined proceeds of approximately $35 million.

For 2025, Healthpeak Properties confirmed its forecast for adjusted diluted FFO-per-share to be in a range of $1.81 to $1.87. In addition, same-store cash (Adjusted) NOI growth is expected to be 3.0% to 4.0% for the full year.

Click here to download our most recent Sure Analysis report on DOC (preview of page 1 of 3 shown below):

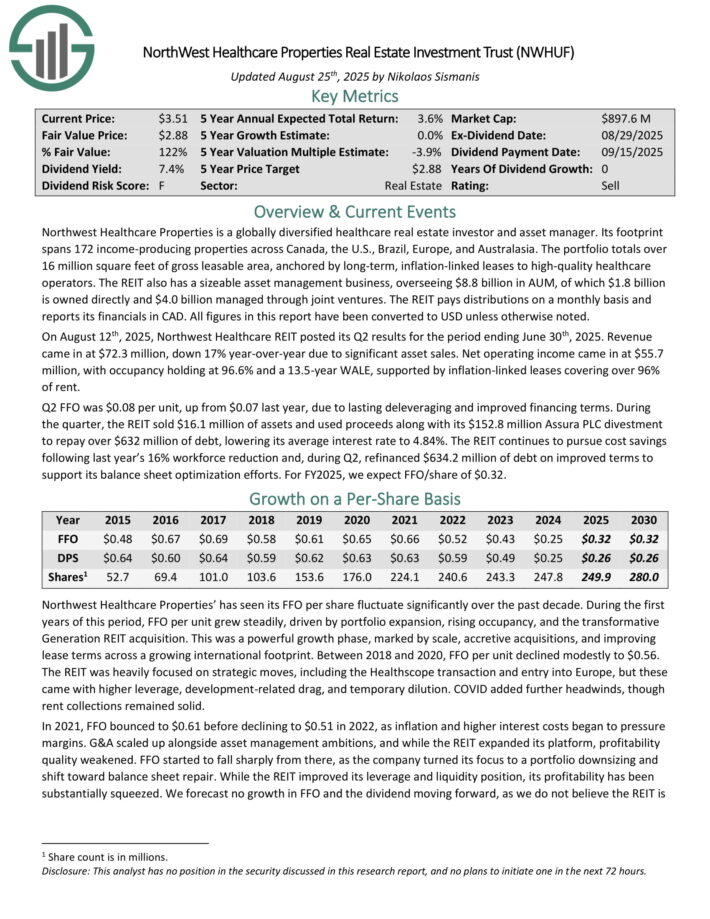

Top REIT #2: NorthWest Healthcare Properties (NWHUF)

Northwest Healthcare Properties is a globally diversified healthcare real estate investor and asset manager. Its footprint spans 172 income-producing properties across Canada, the U.S., Brazil, Europe, and Australasia.

The portfolio totals over 16 million square feet of gross leasable area, anchored by long-term, inflation-linked leases to high-quality healthcare operators.

The REIT also has a sizeable asset management business, overseeing $8.8 billion in AUM, of which $1.8 billion is owned directly and $4.0 billion managed through joint ventures.

On August 12th, 2025, Northwest Healthcare REIT posted its Q2 results for the period ending June 30th, 2025. Revenue came in at $72.3 million, down 17% year-over-year due to significant asset sales.

Net operating income came in at $55.7 million, with occupancy holding at 96.6% and a 13.5-year WALE, supported by inflation-linked leases covering over 96% of rent.

Q2 FFO was $0.08 per unit, up from $0.07 last year, due to lasting deleveraging and improved financing terms. During the quarter, the REIT sold $16.1 million of assets and used proceeds along with its $152.8 million Assura PLC divestment to repay over $632 million of debt, lowering its average interest rate to 4.84%.

The REIT continues to pursue cost savings following last year’s 16% workforce reduction and, during Q2, refinanced $634.2 million of debt on improved terms to support its balance sheet optimization efforts.

Click here to download our most recent Sure Analysis report on NWHUF (preview of page 1 of 3 shown below):

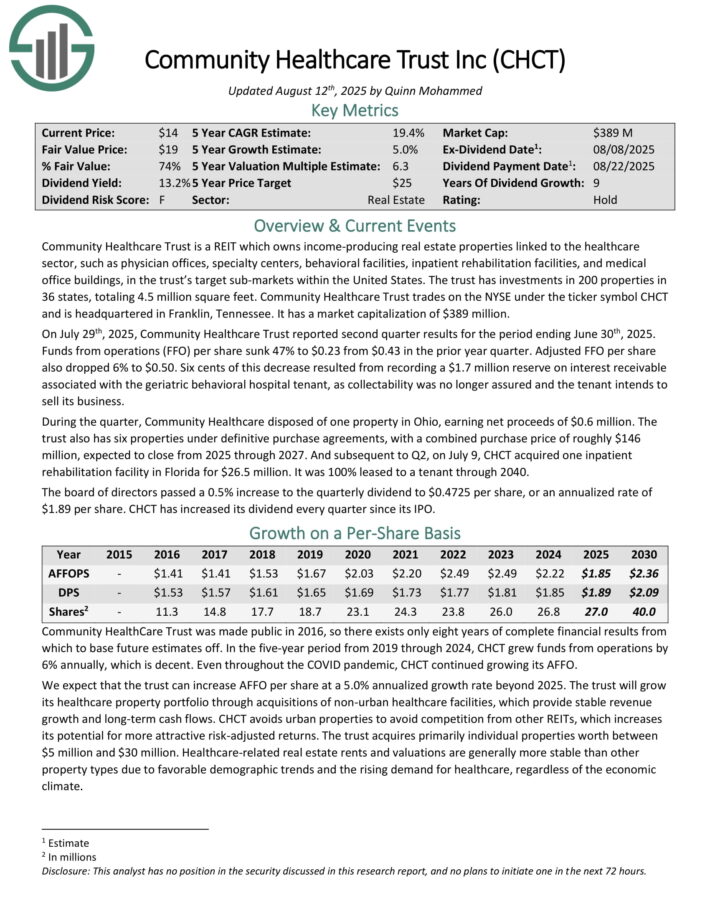

Top REIT #1: Community Healthcare Trust (CHCT)

Community Healthcare Trust owns income-producing real estate properties linked to the healthcare sector, such as physician offices, specialty centers, behavioral facilities, inpatient rehabilitation facilities, and medical office buildings, in the trust’s target sub-markets within the United States.

The trust has investments in 200 properties in 36 states, totaling 4.5 million square feet.

On July 29th, 2025, Community Healthcare Trust reported second quarter results for the period ending June 30th, 2025.

Funds from operations per share sank 47% to $0.23 from $0.43 in the prior year quarter. Adjusted FFO per share also dropped 6% to $0.50.

Six cents of this decrease resulted from recording a $1.7 million reserve on interest receivable associated with the geriatric behavioral hospital tenant, as collectability was no longer assured and the tenant intends to sell its business.

During the quarter, Community Healthcare disposed of one property in Ohio, earning net proceeds of $0.6 million. The trust also has six properties under definitive purchase agreements, with a combined purchase price of roughly $146 million, expected to close from 2025 through 2027.

And subsequent to Q2, on July 9, CHCT acquired one inpatient rehabilitation facility in Florida for $26.5 million. It was 100% leased to a tenant through 2040.

Click here to download our most recent Sure Analysis report on CHCT (preview of page 1 of 3 shown below):

Additional Reading

You can see more high-quality dividend stocks in the following Sure Dividend databases, each based on long streaks of steadily rising dividend payments:

You might also be looking to create a highly customized dividend income stream to pay for life’s expenses.

The following lists provide useful information on high dividend stocks and stocks that pay monthly dividends:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

(Rookie Reply)")

, plus more!")

{kind=link}