Published on March 3rd, 2026 by Bob Ciura

On February 28th, the U.S. and Israel attacked Iran.

In the immediate aftermath of the strikes, oil prices spiked, with WTI crude recently trading above $77 per barrel.

Oil prices rose on the prospect of supply constraints, as well as the potential for more widespread military conflict in the Middle East.

Rising oil prices will be an immediate benefit to the major oil producers.

With this in mind, we compiled a list of nearly 50 energy stocks (along with important investing metrics such as dividend yields), available for download below:

In times of heightened geopolitical risk, income investors should turn to the relative stability of dividend stocks.

This article will list 10 major U.S. oil producers, that stand to benefit directly or indirectly if oil prices continue to rise. These 10 big oil dividend stocks all have yields above the current S&P 500 average.

In turn, their rising profitability could fuel future dividend growth.

Table of Contents

The table of contents below allows for easy navigation. The list is sorted by dividend yield, from lowest to highest.

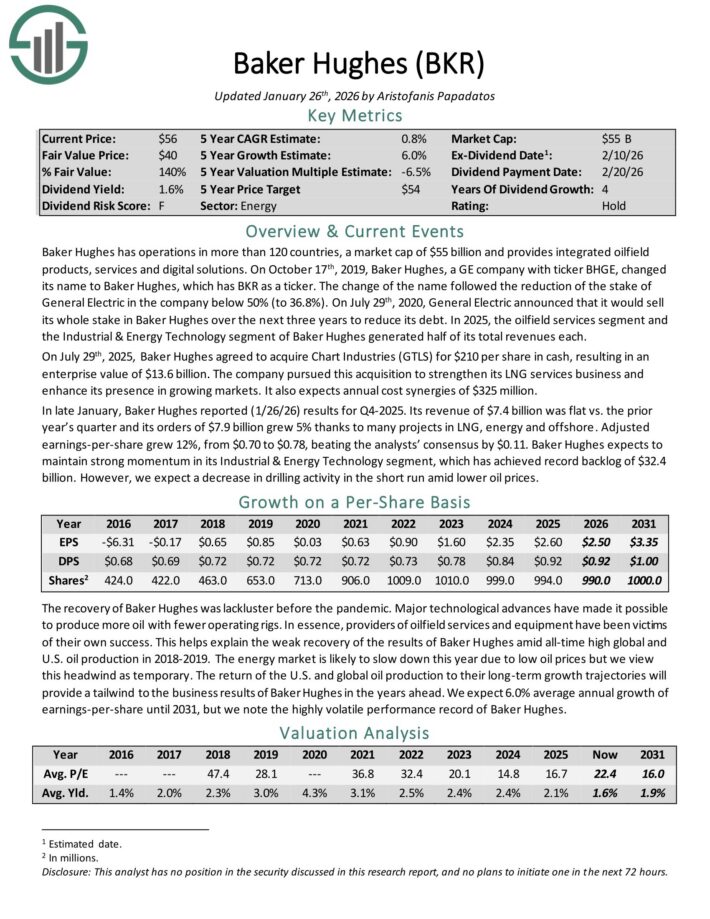

Big Oil Stock: Baker Hughes Co. (BKR)

Baker Hughes has operations in more than 120 countries, and provides integrated oilfield products, services and digital solutions.

In late January, Baker Hughes reported (1/26/26) results for Q4-2025. Its revenue of $7.4 billion was flat vs. the prior year’s quarter and its orders of $7.9 billion grew 5% thanks to many projects in LNG, energy and offshore.

Adjusted earnings-per-share grew 12%, from $0.70 to $0.78, beating the analysts’ consensus by $0.11. Baker Hughes expects to maintain strong momentum in its Industrial & Energy Technology segment, which has achieved record backlog of $32.4 billion.

The return of the U.S. and global oil production to their long-term growth trajectories will provide a tailwind to the business results of Baker Hughes in the years ahead. We expect 6.0% average annual growth of earnings-per-share until 2031.

Click here to download our most recent Sure Analysis report on BKR (preview of page 1 of 3 shown below):

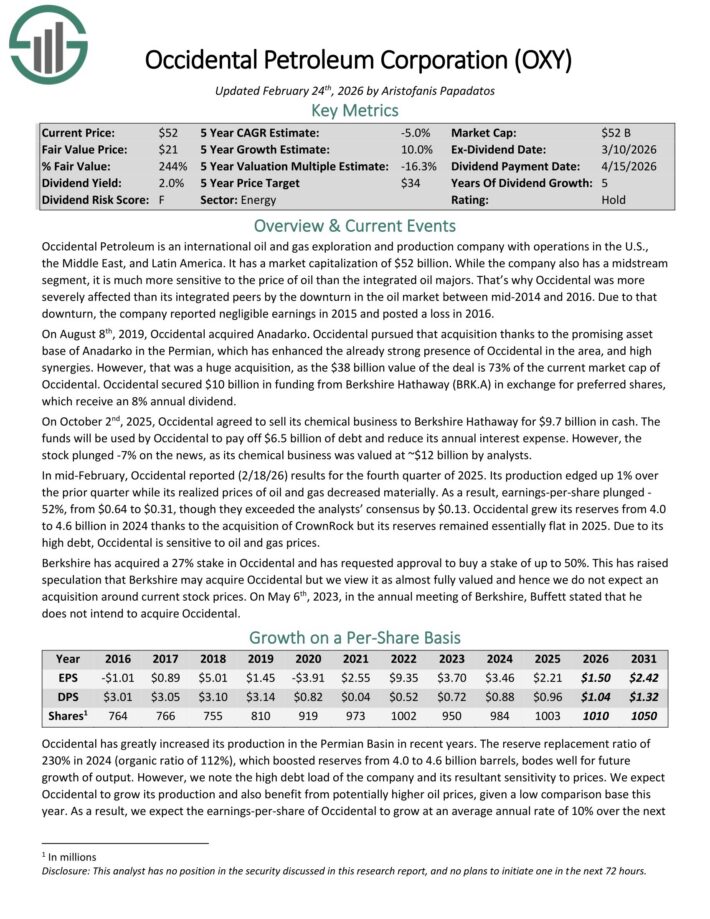

Big Oil Stock: Occidental Petroleum (OXY)

Occidental Petroleum is an international oil and gas exploration and production company with operations in the U.S., the Middle East, and Latin America.

While the company also has a midstream segment, it is much more sensitive to the price of oil than the integrated oil majors.

On October 2nd, 2025, Occidental agreed to sell its chemical business to Berkshire Hathaway for $9.7 billion in cash. The funds will be used by Occidental to pay off $6.5 billion of debt and reduce its annual interest expense.

In mid-February, Occidental reported (2/18/26) results for the fourth quarter of 2025. Its production edged up 1% over the prior quarter while its realized prices of oil and gas decreased materially.

As a result, earnings-per-share plunged 52%, from $0.64 to $0.31, though they exceeded the analysts’ consensus by $0.13.

Occidental grew its reserves from 4.0 to 4.6 billion in 2024 thanks to the acquisition of CrownRock but its reserves remained essentially flat in 2025. Due to its high debt, Occidental is sensitive to oil and gas prices.

Occidental has greatly increased its production in the Permian Basin in recent years. The reserve replacement ratio of 230% in 2024 (organic ratio of 112%), which boosted reserves from 4.0 to 4.6 billion barrels, bodes well for future growth of output.

Click here to download our most recent Sure Analysis report on OXY (preview of page 1 of 3 shown below):

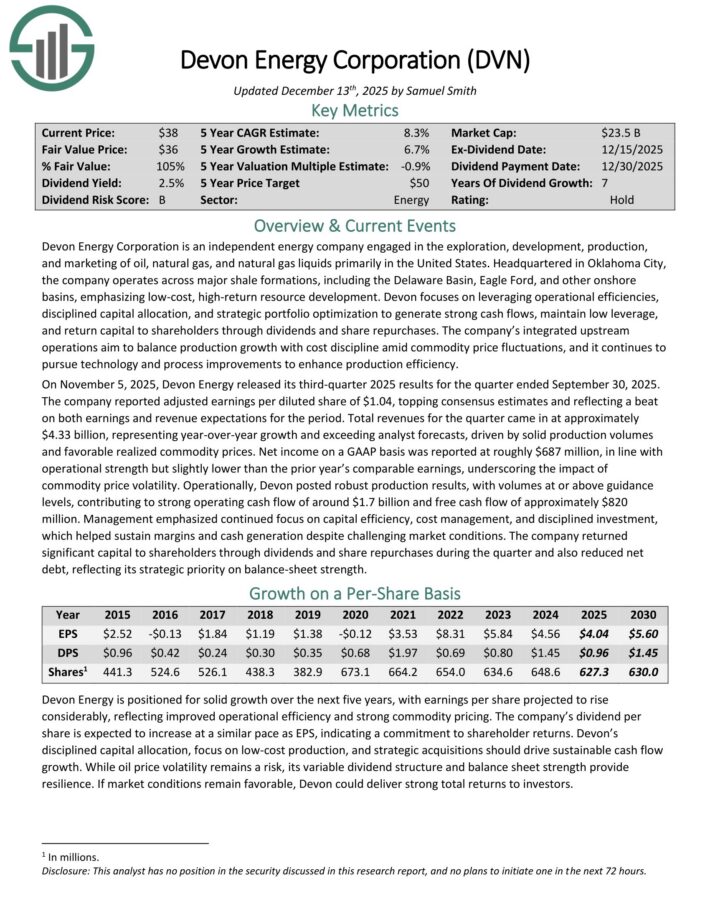

Big Oil Stock: Devon Energy (DVN)

Devon Energy Corporation is an independent energy company engaged in the exploration, development, production, and marketing of oil, natural gas, and natural gas liquids primarily in the United States.

The company operates across major shale formations, including the Delaware Basin, Eagle Ford, and other onshore basins, emphasizing low-cost, high-return resource development.

On November 5, 2025, Devon Energy released its third-quarter 2025 results for the quarter ended September 30, 2025. The company reported adjusted earnings per diluted share of $1.04, topping consensus estimates and reflecting a beat on both earnings and revenue expectations for the period.

Total revenue for the quarter came in at approximately $4.33 billion, representing year-over-year growth and exceeding analyst forecasts, driven by solid production volumes and favorable realized commodity prices.

Net income on a GAAP basis was reported at roughly $687 million, in line with operational strength but slightly lower than the prior year’s comparable earnings, underscoring the impact of commodity price volatility.

Operationally, Devon posted robust production results, with volumes at or above guidance levels, contributing to strong operating cash flow of around $1.7 billion and free cash flow of approximately $820 million.

Management emphasized continued focus on capital efficiency, cost management, and disciplined investment, which helped sustain margins and cash generation despite challenging market conditions.

The company returned significant capital to shareholders through dividends and share repurchases during the quarter and also reduced net debt.

Click here to download our most recent Sure Analysis report on DVN (preview of page 1 of 3 shown below):

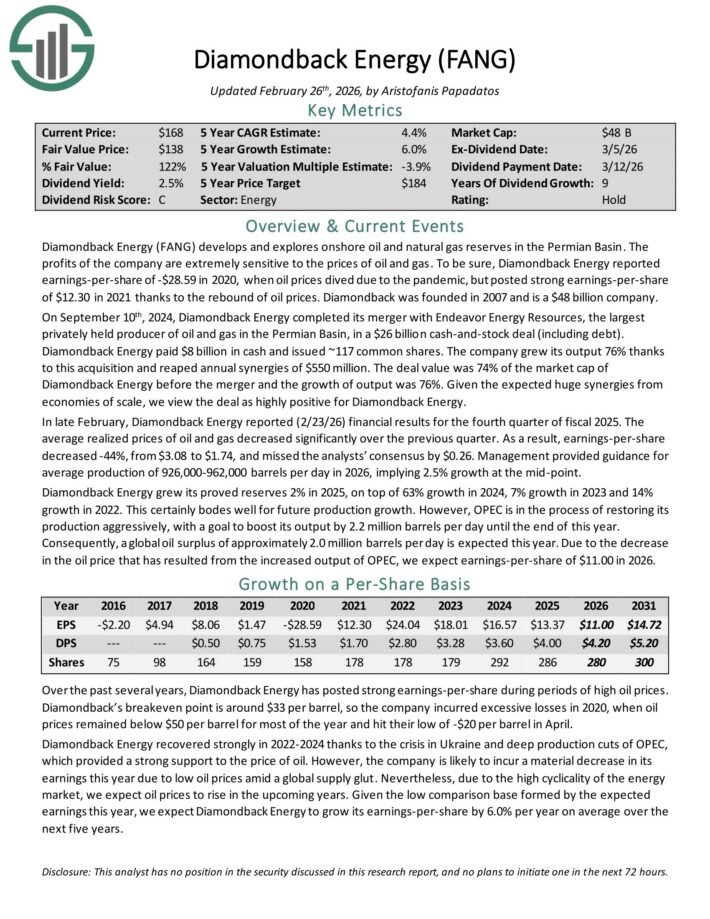

Big Oil Stock: Diamondback Energy (FANG)

Diamondback Energy (FANG) develops and explores onshore oil and natural gas reserves in the Permian Basin. The profits of the company are extremely sensitive to the prices of oil and gas.

In late February, Diamondback Energy reported (2/23/26) financial results for the fourth quarter of fiscal 2025. The average realized prices of oil and gas decreased significantly over the previous quarter.

As a result, earnings-per-share decreased -44%, from $3.08 to $1.74, and missed the analysts’ consensus by $0.26.

Management provided guidance for average production of 926,000-962,000 barrels per day in 2026, implying 2.5% growth at the mid-point.

Diamondback Energy grew its proved reserves 2% in 2025, on top of 63% growth in 2024, 7% growth in 2023 and 14% growth in 2022. This certainly bodes well for future production growth.

Over the past several years, Diamondback Energy has posted strong earnings-per-share during periods of high oil prices. Diamondback’s breakeven point is around $33 per barrel.

The low dividend payout ratio of 38% is likely to provide a wide margin of safety for the dividend for the foreseeable future.

Click here to download our most recent Sure Analysis report on FANG (preview of page 1 of 3 shown below):

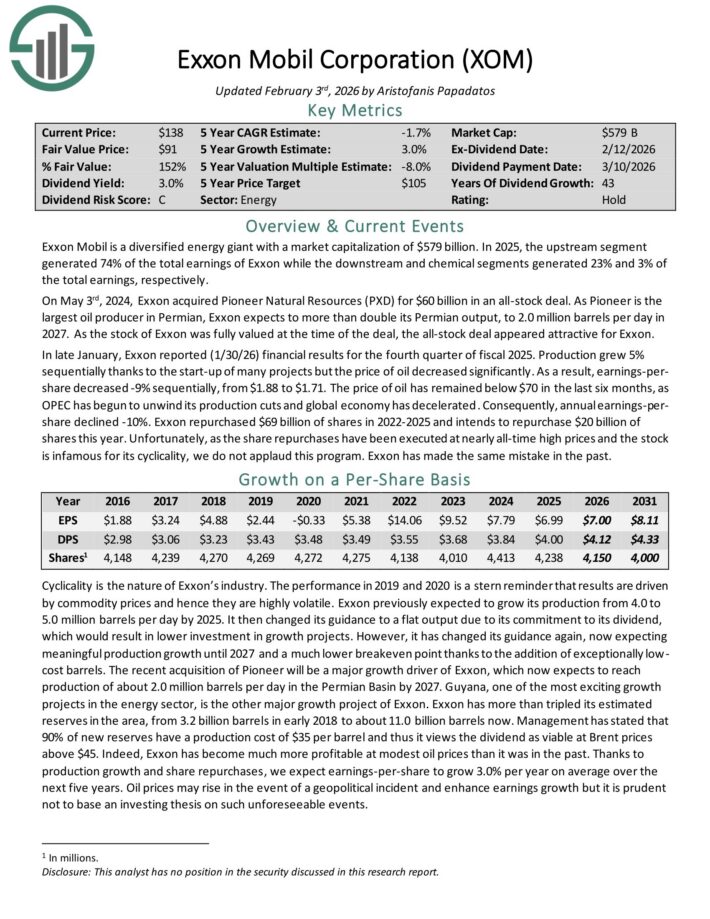

Big Oil Stock: Exxon Mobil (XOM)

Exxon Mobil is a diversified energy giant with a market capitalization of $643 billion.

In 2025, the upstream segment generated 74% of the total earnings of Exxon while the downstream and chemical segments generated 23% and 3% of the total earnings, respectively.

In late January, Exxon reported (1/30/26) financial results for the fourth quarter of fiscal 2025. Production grew 5% sequentially thanks to the start-up of many projects but the price of oil decreased significantly.

As a result, earnings-per-share decreased -9% sequentially, from $1.88 to $1.71. The price of oil has remained below $70 in the last six months, as OPEC has begun to unwind its production cuts and global economy has decelerated.

Consequently, annual earnings-per-share declined -10%. Exxon repurchased $69 billion of shares in 2022-2025 and intends to repurchase $20 billion of shares this year.

Exxon is expecting meaningful production growth until 2027 and a much lower breakeven point thanks to the addition of exceptionally low-cost barrels.

The recent acquisition of Pioneer will be a major growth driver of Exxon, which now expects to reach production of about 2.0 million barrels per day in the Permian Basin by 2027.

Guyana, one of the most exciting growth projects in the energy sector, is the other major growth project of Exxon. Exxon has more than tripled its estimated reserves in the area, from 3.2 billion barrels in early 2018 to about 11.0 billion barrels now.

Click here to download our most recent Sure Analysis report on XOM (preview of page 1 of 3 shown below):

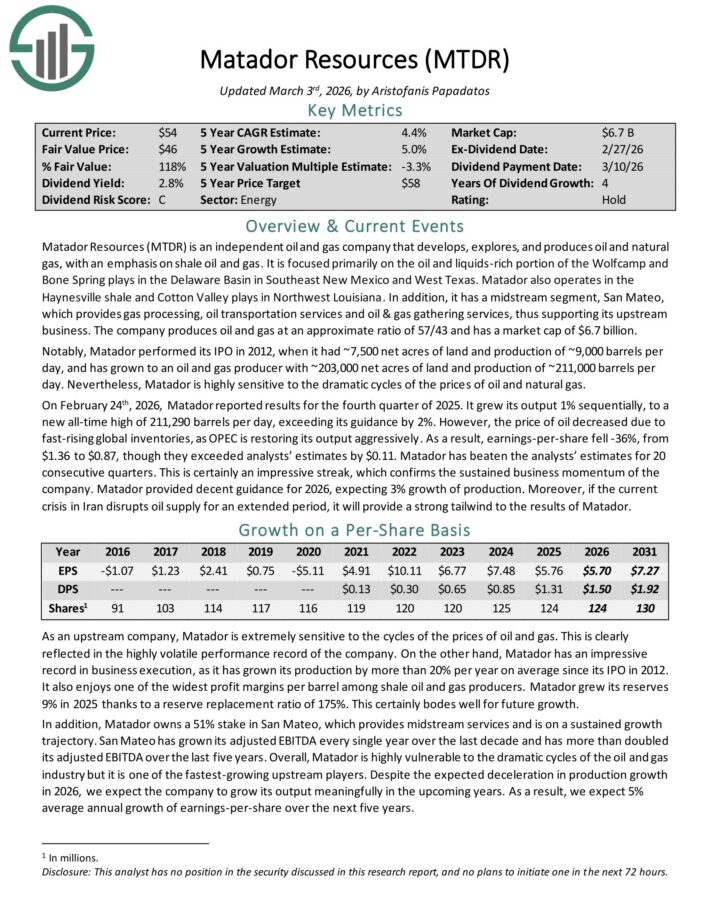

Big Oil Stock: Matador Resources (MTDR)

Matador Resources (MTDR) is an independent oil and gas company that develops, explores, and produces oil and natural gas, with an emphasis on shale oil and gas.

It is focused primarily on the oil and liquids-rich portion of the Wolfcamp and Bone Spring plays in the Delaware Basin in Southeast New Mexico and West Texas.

Matador also operates in the Haynesville shale and Cotton Valley plays in Northwest Louisiana. The company produces oil and gas at an approximate ratio of 57/43.

Matador is an oil and gas producer with ~203,000 net acres of land and production of ~211,000 barrels per day. It is highly sensitive to the dramatic cycles of the prices of oil and natural gas.

On February 24th, 2026, Matador reported results for the fourth quarter of 2025. It grew its output 1% sequentially, to a new all-time high of 211,290 barrels per day, exceeding its guidance by 2%.

However, the price of oil decreased due to fast-rising global inventories, as OPEC is restoring its output aggressively. As a result, earnings-per-share fell -36%, from $1.36 to $0.87, though they exceeded analysts’ estimates by $0.11.

Matador has beaten the analysts’ estimates for 20 consecutive quarters. This is certainly an impressive streak, which confirms the sustained business momentum of the company.

Matador provided decent guidance for 2026, expecting 3% growth of production.

Click here to download our most recent Sure Analysis report on MTDR (preview of page 1 of 3 shown below):

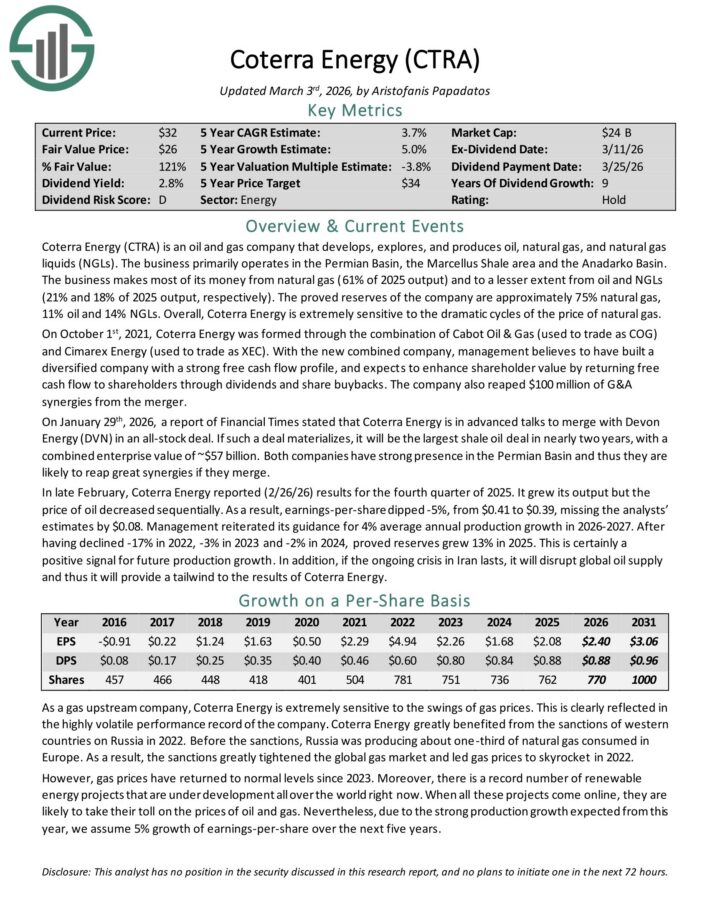

Big Oil Stock: Coterra Energy (CTRA)

Coterra Energy (CTRA) is an oil and gas company that develops, explores, and produces oil, natural gas, and natural gas liquids (NGLs).

The business primarily operates in the Permian Basin, the Marcellus Shale area and the Anadarko Basin. The business makes most of its money from natural gas (61% of 2025 output) and to a lesser extent from oil and NGLs (21% and 18% of 2025 output, respectively).

The proved reserves of the company are approximately 75% natural gas, 11% oil and 14% NGLs.

On October 1st, 2021, Coterra Energy was formed through the combination of Cabot Oil & Gas (used to trade as COG) and Cimarex Energy (used to trade as XEC).

With the new combined company, management believes to have built a diversified company with a strong free cash flow profile, and expects to enhance shareholder value by returning free cash flow to shareholders through dividends and share buybacks. The company also reaped $100 million of G&A synergies from the merger.

On January 29th, 2026, a report of Financial Times stated that Coterra Energy is in advanced talks to merge with Devon Energy (DVN) in an all-stock deal.

If such a deal materializes, it will be the largest shale oil deal in nearly two years, with a combined enterprise value of ~$57 billion. Both companies have strong presence in the Permian Basin and thus they are likely to reap great synergies if they merge.

In late February, Coterra Energy reported (2/26/26) results for the fourth quarter of 2025. It grew its output but the price of oil decreased sequentially.

As a result, earnings-per-share dipped -5%, from $0.41 to $0.39, missing the analysts’ estimates by $0.08. Management reiterated its guidance for 4% average annual production growth in 2026-2027.

After having declined -17% in 2022, -3% in 2023 and -2% in 2024, proved reserves grew 13% in 2025. This is certainly a positive signal for future production growth.

Click here to download our most recent Sure Analysis report on CTRA (preview of page 1 of 3 shown below):

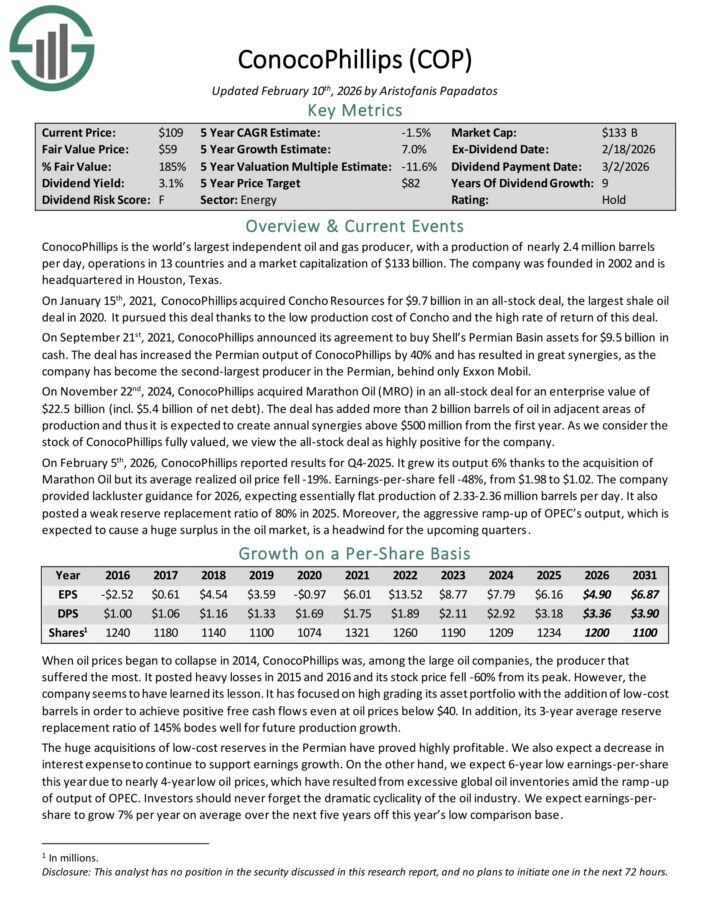

Big Oil Stock: ConocoPhillips (COP)

ConocoPhillips is the world’s largest independent oil and gas producer, with a production of nearly 2.4 million barrels per day, operations in 13 countries and a market capitalization of $144 billion.

On February 5th, 2026, ConocoPhillips reported results for Q4-2025. It grew its output 6% thanks to the acquisition of Marathon Oil but its average realized oil price fell -19%. Earnings-per-share fell -48%, from $1.98 to $1.02.

The company provided lackluster guidance for 2026, expecting essentially flat production of 2.33-2.36 million barrels per day. It also posted a weak reserve replacement ratio of 80% in 2025.

It has focused on high grading its asset portfolio with the addition of low-cost barrels in order to achieve positive free cash flows even at oil prices below $40.

In addition, its 3-year average reserve replacement ratio of 145% bodes well for future production growth.

The huge acquisitions of low-cost reserves in the Permian have proved highly profitable. We also expect a decrease in interest expense to continue to support earnings growth.

Click here to download our most recent Sure Analysis report on COP (preview of page 1 of 3 shown below):

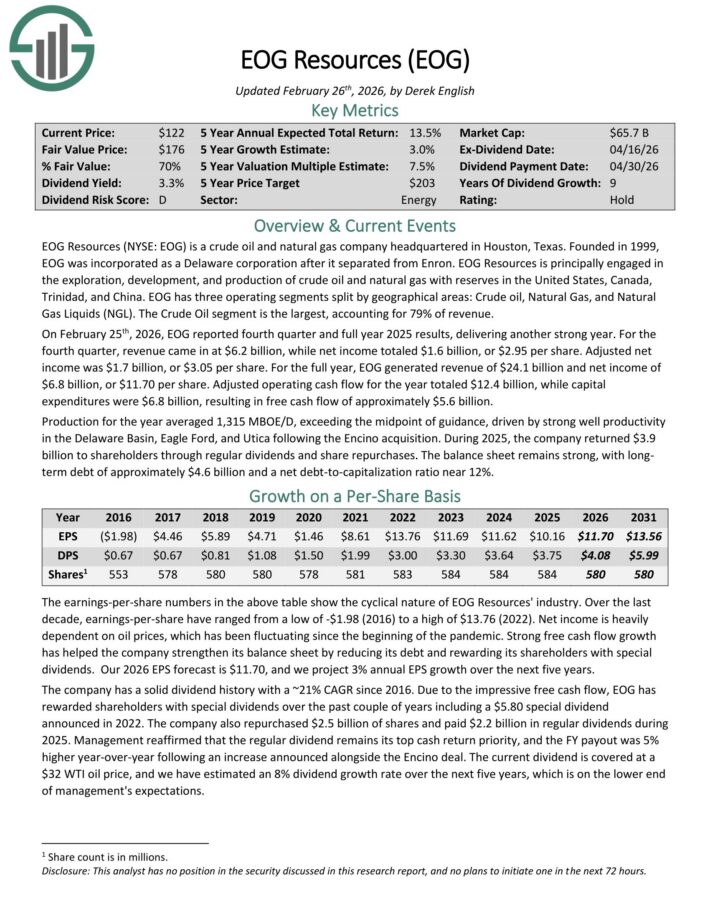

Big Oil Stock: EOG Resources (EOG)

EOG Resources (NYSE: EOG) is a crude oil and natural gas company headquartered in Houston, Texas. It is principally engaged in the exploration, development, and production of crude oil and natural gas with reserves in the United States, Canada, Trinidad, and China.

EOG has three operating segments split by geographical areas: Crude oil, Natural Gas, and Natural Gas Liquids (NGL). The Crude Oil segment is the largest, accounting for 79% of revenue.

On February 25th, 2026, EOG reported fourth quarter and full year 2025 results, delivering another strong year. For the fourth quarter, revenue came in at $6.2 billion, while net income totaled $1.6 billion, or $2.95 per share. Adjusted net income was $1.7 billion, or $3.05 per share.

For the full year, EOG generated revenue of $24.1 billion and net income of $6.8 billion, or $11.70 per share. Adjusted operating cash flow for the year totaled $12.4 billion, while capital expenditures were $6.8 billion, resulting in free cash flow of approximately $5.6 billion.

Production for the year averaged 1,315 MBOE/D, exceeding the midpoint of guidance, driven by strong well productivity in the Delaware Basin, Eagle Ford, and Utica following the Encino acquisition.

During 2025, the company returned $3.9 billion to shareholders through regular dividends and share repurchases.

The balance sheet remains strong, with longterm debt of approximately $4.6 billion and a net debt-to-capitalization ratio near 12%.

Click here to download our most recent Sure Analysis report on EOG (preview of page 1 of 3 shown below):

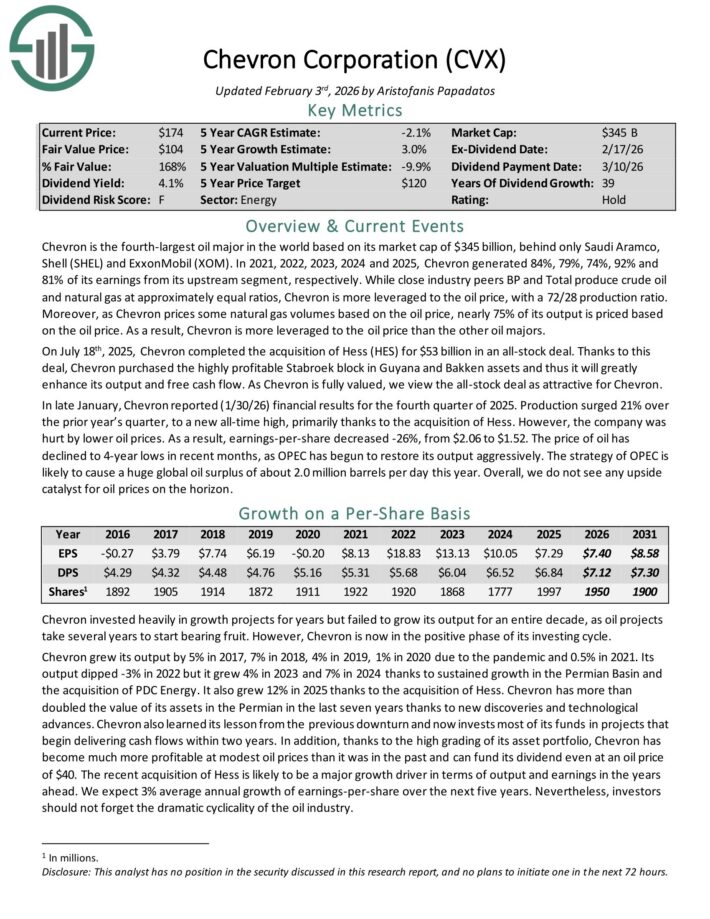

Big Oil Stock: Chevron Corporation (CVX)

Chevron is the fourth-largest oil major in the world based on its market cap of $378 billion, behind only Saudi Aramco, Shell (SHEL) and ExxonMobil (XOM).

In 2021, 2022, 2023, 2024 and 2025, Chevron generated 84%, 79%, 74%, 92% and 81% of its earnings from its upstream segment, respectively.

Its close industry peers produce crude oil and natural gas at approximately equal ratios, but Chevron is more leveraged to the oil price, with a 72/28 production ratio.

Moreover, as Chevron prices some natural gas volumes based on the oil price, nearly 75% of its output is priced based on the oil price. As a result, Chevron is more leveraged to the oil price than the other oil majors.

In late January, Chevron reported (1/30/26) financial results for the fourth quarter of 2025. Production surged 21% over the prior year’s quarter, to a new all-time high, primarily thanks to the acquisition of Hess.

However, the company was hurt by lower oil prices. As a result, earnings-per-share decreased -26%, from $2.06 to $1.52.

Chevron grew 4% in 2023 and 7% in 2024 thanks to sustained growth in the Permian Basin and the acquisition of PDC Energy. It also grew 12% in 2025 thanks to the acquisition of Hess.

Chevron has more than doubled the value of its assets in the Permian in the last seven years thanks to new discoveries and technological advances.

Chevron is a member of the exclusive Dividend Aristocrats list thanks to its 39 consecutive years of dividend increases.

Click here to download our most recent Sure Analysis report on Chevron Corporation (CVX) (preview of page 1 of 3 shown below):

Final Thoughts

The energy sector has many quality dividend stocks, a select few of which have maintained long histories of increasing their dividends.

With that said, it’s not the only place where great investments can be found.

For investors that already have a full dose of energy exposure but are still looking for high-quality investment opportunities, the following Sure Dividend databases will be useful:

The Dividend Aristocrats List: dividend stocks in the S&P 500 with 25+ years of consecutive dividend increases.

The Dividend Kings List: containing the ‘best-of-the-best’ when it comes to dividend growth, the Dividend Kings List is composed of dividend stocks with 50+ years of consecutive dividend increases.

The Blue Chip Stocks List: dividend stocks with 10+ years of dividend increases that represent quality long-term investments.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

{kind=link}