The weekly commentary from BlackRock—the world’s largest asset manager and investment firm, with over $12.5 trillion in assets—published on February 9, states that,

Emerging market (EM) equities and bonds have had a strong start to the year following a stellar 2015. We believe returns can return to positive territory… although selectivity is key. We are focused on the big forces… particularly AI in technology hardware in Asia and commodity-linked equities in Latin America.

The report then includes the following chart on “MSCI Emerging Markets Index Performance, 2015-2026” and notes that it “shows EM equities are carrying over last year’s outperformance to 2026: the MSCI EM Index outperformed its developed market counterpart in January.”

The report continues,

The strength of emerging market equities has continued into 2026: the MSCI Emerging Markets Index posted a gain of nearly 9 percent last month, its best January since 2012 and one of its biggest monthly gains in recent years, easily outperforming the 2.2% gain in developed market equities.

It further notes that, “South Korean equities have risen more than 20% following strong gains last year, while India continues to lag, even with the recent US trade deal.”

It goes on to assert that, “Investor appetite for emerging markets remains strong: 2025 was a record year for capital inflows, with Emerging market debt and equity ETPs raising $152 billion and $103 billion, respectively, according to data from BlackRock and Markit.” According to BlackRock analysts,

Emerging markets are key to AI development, from industrial metals to manufacturing supply chains… like copper, which is needed to drive technology development and is mainly found in emerging countries… especially in Latin America… We also anticipate that the restructuring of global supply chains will benefit Mexico, Brazil, and Vietnam, while rising commodity prices will benefit Latin America.

On the other hand, given the volatility of local currencies, “We prefer emerging market debt in hard currency and maintain selectivity in emerging market equities,” these analysts recommend.

Incidentally, it is striking that the report does not mention Argentina, considering the extremely high level of publicity its president—an excellent propagandist—has garnered.

But propaganda and rhetoric aside, the reality is that investments in Argentina are not noteworthy. For comparison with the BlackRock chart here is one showing the Argentine S&P Merval’s performance during 2025:

Source: Dolarito

In summary, as can be seen in the following graph, if we take the year-to-date performance of the S&P Merval, the result does not reach 20 percent, and if we discount the rise in the CPI, it is negative “in real terms,” and the future suggests a similar performance:

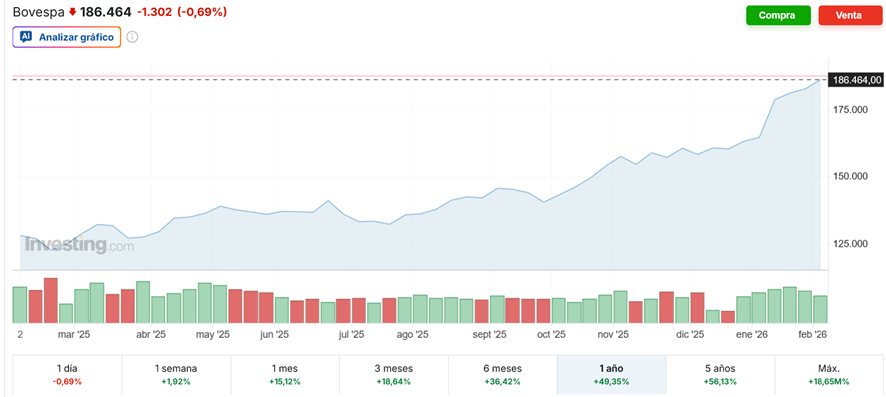

The following comparison is important. As can be seen in the following charts, both the Brazilian stock exchange (Bovespa) and the Colombian stock exchange (Colcap) have performed much better over the past year. The Bovespa:

The Colcap:

Why is this comparison important? Because both countries are governed by leftists, and Colombia by a former guerrilla fighter. This demonstrates that politicians’ speeches are worthless. What should be analyzed is what they do, and the reality is that today both Brazil and Colombia have economies with less state intervention than Argentina (as the Heritage Index shows).

But to leave no doubt, let’s look beyond the stock markets. Foreign Direct Investment (FDI) in Colombia during 2025 closed at USD 9.173 billion, marking a 14.1 percent drop compared to 2024, according to figures from the central bank, mainly due to an increase in the tax burden ordered by the current socialist government.

Meanwhile, in Brazil, FDI reached a significant milestone in 2025, totaling USD 84.1 billion between January and November, the highest level in a decade and surpassing the figures for 2014.

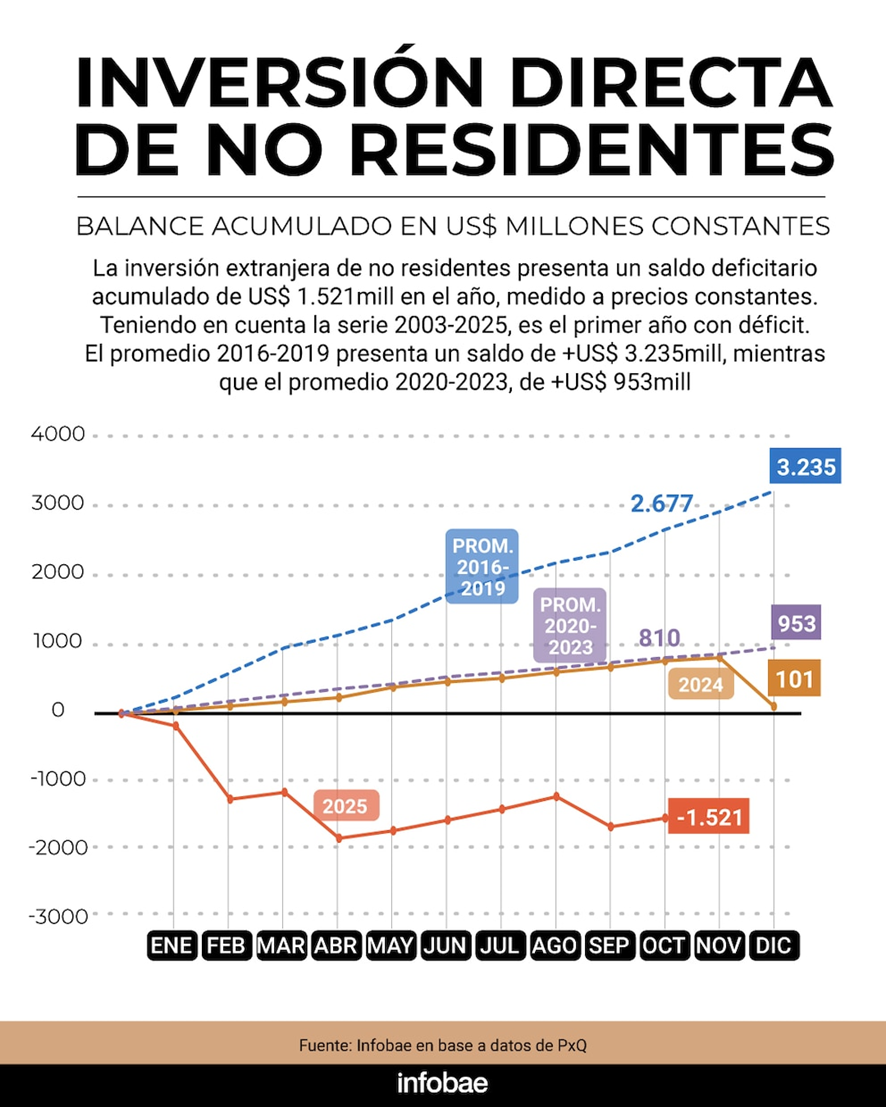

In stark contrast, the government has managed to ensure that, for the first time since 2003, FDI in Argentina shows a negative cumulative balance of USD 1.521 billion between January and November 2025:

According to the latest data from the tax collection agency, ARCA, 15,000 companies closed between November 2023 and August 2025. Clearly, while the president is expected to fulfill his campaign promise to move towards a free market economy, Argentina is disinvesting and all indications are that this process will continue.

As the prominent economist Roberto Cachanosky points out,

If you look at the inflation data from 2025 up to January of this year, you’ll find that, starting in June of last year, inflation has been continuously rising… But at the same time… (as shown by) the Monthly Economic Activity Estimator (EMAE)… the economy is completely stagnant, it’s completely flat.

The first serious problem Argentina faces is that its foreign exchange market is not free; the government manipulates it. This market regulates domestic production, meaning that to buy abroad, one must produce domestically to obtain the necessary dollars. When local production is weak, few foreign currencies enter the country, thus raising the price of goods measured in pesos. This, in turn, makes local production cheaper in dollar terms, incentivizing domestic consumption and exports, and consequently, local production and investment.

Furthermore, as the Austrian School teaches, strictly speaking, there is no equilibrium point on the supply and demand (SD) curve, but rather a specific environment that tends toward equilibrium, which is never actually reached. For example, when the curve moves toward a certain price level in an attempt to find equilibrium, it incentivizes other businesses to seek new information—new technology—to improve their products, processes, or logistics so they can reduce costs and become more competitive, pushing the SD curve to a new equilibrium price, and so on in an endless cycle.

In short, a state-controlled exchange market destroys—through excess or deficiency—local production and transforms the search for information to improve products into a search for information on how to better cope with state bureaucratic interference.

Argentina’s other serious problem is the very heavy fiscal tax and regulatory burden. The current government has deregulated poorly. And it maintains a very high tax burden—direct and indirect taxes, inflation, and interest rates manipulated by the bureaucracy—believing that the state must first be “organized.” In other words, it would have to be strengthened in reality in order to free the market. What it achieves is the destruction of the private sector, which declines, thus reducing its contributions to the state, in a vicious cycle.

In short, the Argentine president, with two years in office, has made thirteen trips to the US alone with the intention of attracting investment. As expected, he has achieved the opposite effect simply because the market is not moved by the wishful thinking of politicians who believe that investors will follow their “recommendations.” Money is cold; it doesn’t listen to speeches, it looks at real numbers, and it goes where it benefits, stealthily and without saying a word.

{kind=link}