Yves here. It is not at all like the Fed, or central banks generally to think much about possible asset bubbles, since they look like an increase in wealth to investors and bystanders until they don’t. We quoted an op-ed in the Sydney Morning Herald by the former Australia Reserve Bank governor Ian Macfarlane on this issue in 2007. Germane sections:

The biggest single challenge starts with the recognition that as an economy becomes more developed, its financial side grows a lot faster than its real side. As a result, economic outcomes will depend more on what happens in asset markets and less on what happens in the real side of the economy, such as in the goods and labour markets….If a major financial shock were to occur, such as a large fall in share or property prices, the effect on the economy would be greater than before.

So the central question is whether booms and busts in asset markets are more likely to occur in the future…

If it is likely that asset price booms and busts will be at least as common as over the past two decades and that their effect on the economy will be larger, what can monetary policy do about it? …

So, if low inflation does not provide any insurance, what should a central bank do if it suspects that a potentially unsustainable asset price boom is forming, particularly when the boom is being financed by debt?…

Many people have pointed out that it is difficult to identify a bubble in its early stages, and this is true. But even if we can identify an emerging bubble, it may still be extremely difficult for a central bank to act against it for two reasons.

First, monetary policy is a very blunt instrument. When interest rates are raised to address an asset price boom in one sector, such as house prices, the whole economy is affected. If confidence is especially high in the booming sector, it may not be much affected at first by the higher interest rates, but the rest of the economy may be.

Second, there is a bigger issue which concerns the mandate that central banks have been given. There is now widespread acceptance that central banks have been delegated the task of preventing a resurgence in inflation, but nowhere, to my knowledge, have they been delegated the task of preventing large rises in asset prices, which many people would view as rises in the community’s wealth. Thus, if they were to take on this additional role, they would face a formidable task in convincing the public of the need.

Even if the central bank was confident that a destabilising bubble was forming, and that its bursting would be extremely damaging, the community would not necessarily know that this was in prospect, and could not know until the whole episode had been allowed to play itself out. If the central bank went ahead and raised interest rates, it would be accused of risking a recession to avoid something that it was worried about, but the community was not. If in the most favourable case, the central bank raised interest rates by a modest amount and prevented the bubble from expanding to a dangerous level, and it did so at a relatively small cost in terms of income and employment growth forgone, would it get any thanks? Almost certainly not…In all probability, the episode would be regarded by the public as an error of monetary policy because what might have happened could never be observed.

So Wolf was correct to use the word “fret”. Too much lending now takes place outside banks for regulators to deploy credit controls or send word out that lending to certain sectors would get extra scrutiny.

By Wolf Richter, editor at Wolf Street. Originally published at Wolf Street

“AI” was mentioned 21 times in the minutes of the FOMC meeting on June 16-17, released today – up from 8 mentions in the minutes of the prior FOMC meeting in April – in these combinations:

“AI buildout” (4 times) and “AI infrastructure” (2 times)

“AI-related investments” (3 times), “AI business investment,” “AI investment,” “AI-related capital spending,” “AI-related expenditures”

“AI adoption” (2 times)

“AI implications for corporate profitability”

“AI-related price pressures”

“AI-related demand”

“Optimism about AI.”

Plus:

Some participants commented on the possibility that AI could, over time, affect employment prospects for some classes of workers…

Strong corporate earnings and continued investor optimism related to AI contributed to increases in foreign equity prices.

The AI investment mania is now officially a force that is driving demand and pushing up consumer prices including electricity and tech products, stock prices, and input costs for companies that they would then try to pass on. And that is now.

But the hoped-for productivity gains and deflationary pressures from AI were deemed uncertain and in the future:

Some participants remarked that productivity gains associated with AI adoption would eventually reduce production costs and increase aggregate supply, which should put downward pressure on inflation, though they noted this effect would likely take time to materialize

And:

Some participants suggested that those [AI] investments would likely increase the growth of productivity and of potential output in the coming years. These participants remarked, however, that considerable uncertainty remained regarding both the timing and magnitude of potential productivity gains, which were expected to lag the ongoing boost of AI adoption on demand

By contrast, the other two Fed bogymen, “energy” as a result of the war in Iran and “tariffs” were mentioned only 13 and 7 times respectively in the minutes today.

“Electricity” was mentioned once, but in the context of AI driving up electricity prices, along with prices of tech products, thereby pushing inflation higher:

Many participants noted that ongoing strong demand for AI infrastructure would likely sustain upward pressure on prices for technology products and electricity.

Here are some of the other mentions:

Many participants noted that ongoing strong demand for AI infrastructure would likely sustain upward pressure on prices for technology products and electricity.

Most participants, however, also pointed to scenarios in which, in the context of stable labor market conditions, inflation would remain elevated due to strong AI-related demand, the conflict in the Middle East, or the effects of tariffs.

Most participants remarked that growth in economic activity that exceeded that of potential output, owing in part to strong AI business investment, could contribute to more persistent inflationary pressures.

Some participants noted that broad financial conditions were supporting demand. These participants pointed specifically to high equity prices and noted that those prices had been driven by strong corporate earnings and optimism about AI.

Participants generally expected solid real GDP growth to continue throughout the remainder of the year and pointed to several factors likely to support continued expansion, including ongoing AI-related investment, household spending, and fiscal policy

The AI investment mania – the hundreds of billions of dollars that investors are eager to cough up and that are getting thrown around left and right – and the demand and inflationary pressures that those hundreds of billions of dollars generate, have begun to percolate through the economy. And the Fed has begun to fret about the effects.

It is refreshing that the Fed is taking this threat to price stability seriously, rather than trying to “look through” these pressures from the AI investment mania and wait for them to go away on their own somehow, while those pressures could be fueling the second wave of inflation.

So there was a pivot at the Fed at the June FOMC meeting, as per today’s meeting minutes: The discussion was about whether to raise rates, with “a few” participants even acknowledging that “there was a case” for hiking at the June meeting.

By contrast, at the meetings last year and earlier this year, the discussion was about whether to cut rates – and the Fed did cut rates three times last fall.

It is rare that the Fed does a one-and-done rate hike. Most often, a rate hike means a new hiking cycle to get inflation under control.

Core inflation measures and overall inflation measures have been above the Fed’s target for over five years. The Fed-favored core PCE price index, which excludes energy and food, has been accelerating since mid-2025 and hit 3.4% in May. The PCE price index was released two weeks after the Fed meeting, and participants had only estimates of it, not the actual data.

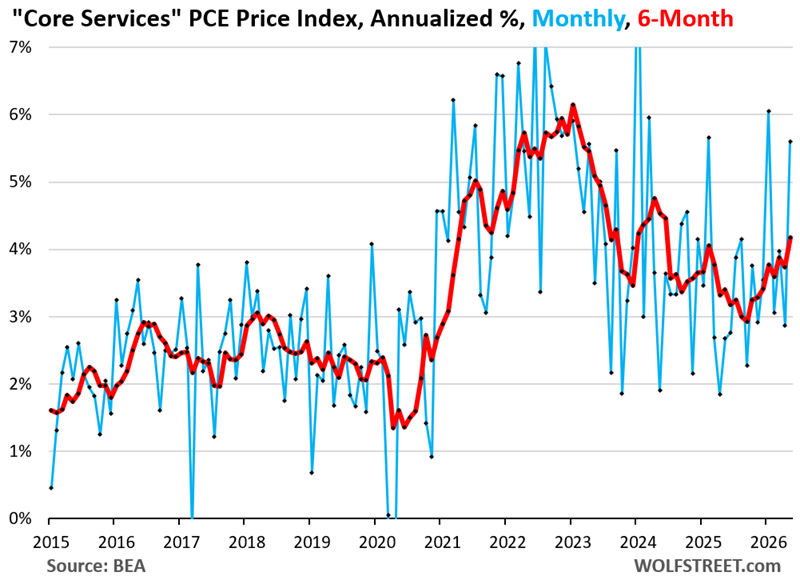

The six-month core PCE price index, which shows the current trend, accelerated to 4.1% annualized, the worst in three years, and this does not include the spiking energy components. Big drivers were non-housing core services, electricity, and tech products.

The six-month core services PCE price index, the big driver behind the core PCE price index, has been accelerating since mid-2025 and hit 4.2% in May. Core services dominate consumer spending. And this time, it’s the non-housing services that are making the noise. If electricity were included in core services, it would look even worse:

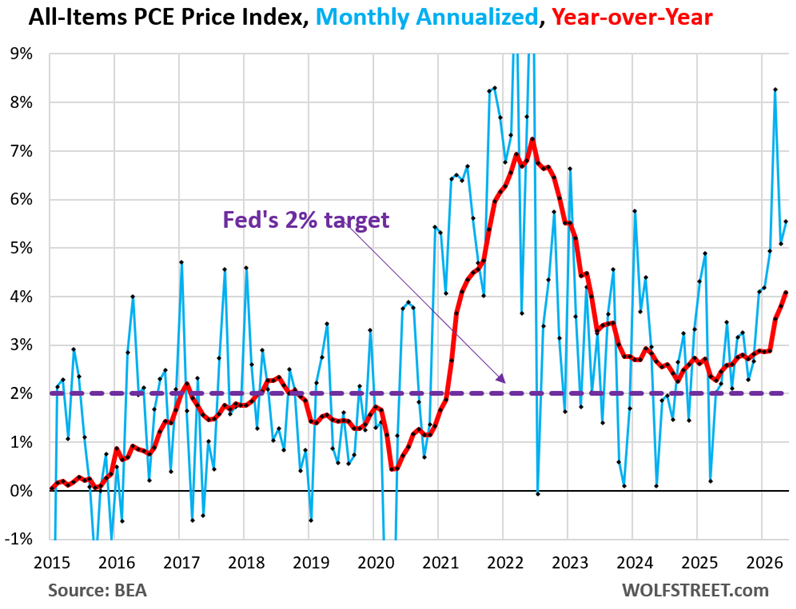

The all-items PCE price index, on which the Fed’s 2% target is based, has been above the Fed’s 2% target since March 2020, for over five years, and now the assumption is spreading, including right here, that the Fed’s de-facto target has been tacitly moved to the 3-4% range, and 2% is just copy-and-paste lip service.

If the Fed wants to stamp out that assumption, it will have to get busy. If it dillydallies around and looks through this inflation, it would be proof that the Fed actually moved the de-factor target to the 3-4% range, and Warsh might as well come out and say it and thereby let long-term Treasury yields and mortgage rates, which are still clinging to the 2% illusion, fly off the handle.

In case you missed it: Consumers Are already Getting the Drift, “Inflation Expectations” Throw the Fed another Curveball.

-1024x683.jpg "Strait Outta Hormuz: Getting the Iran Oil Story Straight")

{kind=link}