Updated on May 29th, 2026 by Bob Ciura

Master Limited Partnerships, otherwise known as MLPs, have obvious appeal for income investors.

This is because MLPs widely offer yields of 5% or even higher in some cases.

With this in mind, we created a full downloadable list of nearly 100 Master Limited Partnerships.

You can download the Excel spreadsheet (along with relevant financial metrics like dividend yield and payout ratios) by clicking on the link below:

This article covers the highest-yielding MLPs today that are covered in the Sure Analysis Research Database.

The table of contents below allows for easy navigation of the article:

Table of Contents

High Yield MLP #13: Brookfield Renewable Partners LP (BEP)

Brookfield Renewable Partners L.P. operates one of the world’s largest portfolios of publicly traded renewable power assets. Its portfolio consists of about 33,000 megawatts of capacity in North America, South America, Europe, and Asia.

Brookfield Renewable Partners is one of four publicly traded listed partnerships that are operated by Brookfield Asset Management (BAM).

In early May, BEP reported (5/1/26) results for the first quarter of 2026. Its funds from operations (FFO) per unit grew 15%, from $0.48 to $0.55, thanks to asset development and acquisitions.

Management expects the strong business momentum to remain in place this year. We still expect 9% growth of FFO per share this year.

BEP is resilient to high inflation, as about 70% of its contracts are indexed to inflation and most of its costs are fixed.

Click here to download our most recent Sure Analysis report on Brookfield Renewable Partners (preview of page 1 of 3 shown below):

High Yield MLP #12: Brookfield Infrastructure Partners LP (BIP)

Brookfield Infrastructure Partners L.P. is one of the largest global owners and operators of infrastructure networks, which includes operations in sectors such as energy, water, freight, passengers, and data.

Brookfield Infrastructure Partners is one of four publicly-traded listed partnerships that is operated by Brookfield Asset Management (BAM).

BIP reported strong results for Q1 2026 on 04/29/26. For the quarter, the diversified utility reported funds fromoperations of $689 million, up 9.8% year over year, driven by its data and midstream segments that experienced increases of 46% and 12%, respectively.

The FFO increase reflects organic growth at the high end of its target range of 6% to 9%, driven by higher inflation-linked revenues, strong utilization in its midstream segment, and the commissioning of over $1.7 billion of projects from its capital backlog since Q1 2025.

Click here to download our most recent Sure Analysis report on Brookfield Infrastructure Partners (preview of page 1 of 3 shown below):

High Yield MLP #11: Genesis Energy LP (GEL)

Genesis Energy is a diversified midstream energy limited partnership, which generates 44% of its operating income from offshore pipeline transportation, 34% from sodium minerals and sulfur services, 4% from onshore facilities and 18% from marine transportation.

In early May, Genesis Energy reported (5/7/26) financial results for the first quarter of fiscal 2026. The offshore pipeline segment grew its operating income 40% over the prior year’s quarter thanks to improved volumes in two major platforms.

Therefore, despite a -7% decrease in the operating income of the marine transportation segment, total operating income grew 29%. Distribution coverage ratio decreased sequentially from 2.8 to 2.0.

The MLP reaffirmed its positive guidance for 2026 thanks to the expansion of Deepwater Gulf, expecting 15%-20% growth of EBITDA.

Click here to download our most recent Sure Analysis report on GEL (preview of page 1 of 3 shown below):

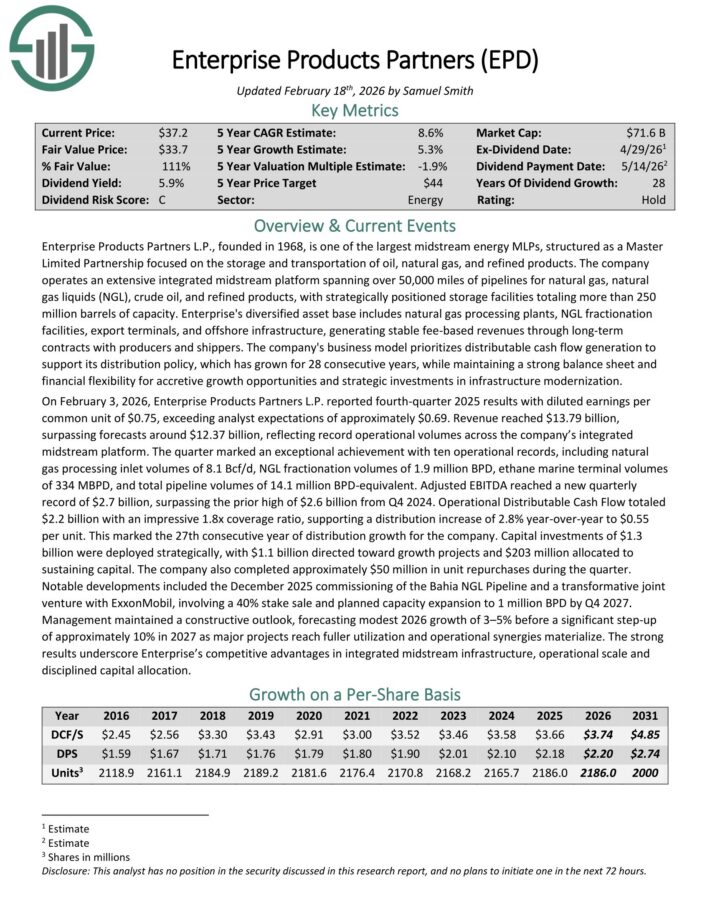

High Yield MLP #10: Enterprise Products Partners LP (EPD)

Enterprise Products Partners was founded in 1968. It is structured as a Master Limited Partnership, or MLP, and operates as an oil and gas storage and transportation company.

Enterprise Products has a large asset base which consists of nearly 50,000 miles of natural gas, natural gas liquids, crude oil, and refined products pipelines.

It also has storage capacity of more than 250 million barrels. These assets collect fees based on volumes of materials transported and stored.

On February 3, 2026, Enterprise Products Partners L.P. reported fourth-quarter 2025 results with diluted earnings per common unit of $0.75, exceeding analyst expectations of approximately $0.69.

Revenue reached $13.79 billion, surpassing forecasts around $12.37 billion, reflecting record operational volumes across the company’s integrated midstream platform.

The quarter marked an exceptional achievement with ten operational records, including natural gas processing inlet volumes of 8.1 Bcf/d, NGL fractionation volumes of 1.9 million BPD, ethane marine terminal volumes of 334 MBPD, and total pipeline volumes of 14.1 million BPD-equivalent.

Adjusted EBITDA reached a new quarterly record of $2.7 billion, surpassing the prior high of $2.6 billion from Q4 2024.

Operational Distributable Cash Flow totaled $2.2 billion with an impressive 1.8x coverage ratio, supporting a distribution increase of 2.8% year-over-year to $0.55 per unit.

This marked the 27th consecutive year of distribution growth for the company.

Click here to download our most recent Sure Analysis report on EPD (preview of page 1 of 3 shown below):

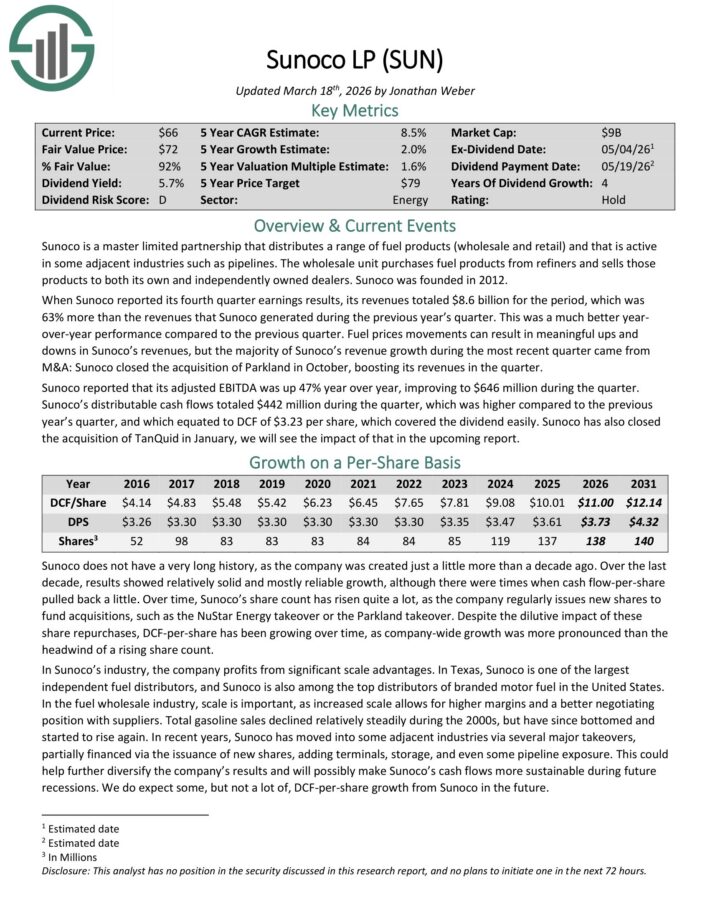

High Yield MLP #9: Sunoco LP (SUN)

Sunoco is a master limited partnership that distributes a range of fuel products (wholesale and retail) and that is active in some adjacent industries such as pipelines.

The wholesale unit purchases fuel products from refiners and sells those products to both its own and independently owned dealers.

When Sunoco reported its fourth quarter earnings results, revenue totaled $8.6 billion for the period, which was 63% more than the revenues that Sunoco generated during the previous year’s quarter.

This was a much better year-over-year performance compared to the previous quarter. Fuel prices movements can result in meaningful ups and downs in Sunoco’s revenue, but the majority of Sunoco’s revenue growth during the most recent quarter came from acquisitions.

Sunoco closed the acquisition of Parkland in October, boosting its revenue in the quarter. Sunoco reported that its adjusted EBITDA was up 47% year over year, improving to $646 million during the quarter.

Distributable cash flows totaled $442 million during the quarter, which was higher compared to the previous year’s quarter, and which equated to DCF of $3.23 per share, which covered the dividend easily.

Click here to download our most recent Sure Analysis report on SUN (preview of page 1 of 3 shown below):

High Yield MLP #8: Star Group LP (SGU)

Star Group, L.P. is a home heating oil and propane distributor and services provider. The company’s Petro Holdings subsidiary provides heating oil and propane to 416,000 US Northeast and Mid-Atlantic customers.

In addition, the company also sells diesel and gasoline to customers across the United States.

It operates two segments: Home Heating Oil and Propane and Other Products and Services, including commercial heating and HVAC services, equipment installations, and repair and maintenance services.

On February 4th, 2026, the company announced its Q1 results for the fiscal year 2021, reporting non-GAAP EPS of $0.89.

Star Group kicked off fiscal 2026 with a solid first quarter, as revenue rose 10.5% year over year to $539.3 million. The growth was largely driven by higher product volumes and continued expansion in service and installation offerings.

Heating oil and propane volumes increased 13.9% to 93.9 million gallons, benefiting from both acquisitions and significantly colder weather. In fact, temperatures across the company’s operating regions were nearly 19% colder than last year and below historical norms, providing a natural boost to demand.

On the profitability side, results showed clear improvement, albeit with a few moving parts. Net income rose to $35.8 million, supported by a sharp increase in Adjusted EBITDA, which climbed to $68.4 million from $51.9 million a year ago.

Click here to download our most recent Sure Analysis report on SGU (preview of page 1 of 3 shown below):

High Yield MLP #7: Global Partners LP (GLP)

Global Partners LP is one of the largest independent owners, operators and suppliers of retail fueling stations and convenience stores, with approximately 1,600 locations.

It has 290 company-operated convenience stores and 54 liquid energy terminals, which have a storage capacity of 22.3 million barrels.

The company operates through three segments: Wholesale, Gasoline Distribution and Station Operations (GDSO), and Commercial.

The Wholesale segment sells oil products to retailers and wholesale distributors. The GDSO segment sells branded and unbranded gasoline to gasoline station operators.

The Commercial segment sells and delivers oil products to customers in the public sector.

On May 8th, 2026, Global Partners reported results for the first quarter of fiscal 2026. Total volume grew from 1.9 billion gallons in the prior year’s quarter to 2.1 billion gallons and total revenue grew 15%.

Thanks to higher sales and wider margins, earnings-per-share surged from $0.36 to $1.85. The company greatly benefited from the highly volatile oil prices, which resulted from the crisis in the Middle East.

Click here to download our most recent Sure Analysis report on GLP (preview of page 1 of 3 shown below):

High Yield MLP #6: Plains GP Holdings LP (PAGP)

Plains GP Holdings via its subsidiary Plains All American Pipeline (PAA), manages midstream energy infrastructure across the USA and Canada. Their operations span two sectors: Crude Oil and Natural Gas Liquids (NGLs).

They transport these resources through pipelines, gathering systems, and trucks while providing storage, terminalling, throughput, NGL fractionation, isomerization, and natural gas processing services. Their logistics aid producers, refiners, and clients in the energy sector.

On February 7th, 2025, the company announced results for the fourth quarter of 2024. Plains GP Holdings reported Q4 non-GAAP EPS of -$0.05, missing the market’s estimates by $0.25. The company reported revenues of $12.4 billion for the quarter, which were down 2.4% year-over-year.

Looking ahead, Plains expects 2025 adjusted EBITDA between $2.8 billion and $2.95 billion, representing a 3% increase at the midpoint. The company also announced a 20% increase in its quarterly distribution to $1.52 per unit annually, with the next payout of $0.25 per unit scheduled for February 14, 2025.

With Permian crude production forecast to grow by 200,000 to 300,000 barrels per day, Plains anticipates high utilization rates on Corpus Christi-bound assets and increasing volumes on the basin pipeline.

Click here to download our most recent Sure Analysis report on PAGP (preview of page 1 of 3 shown below):

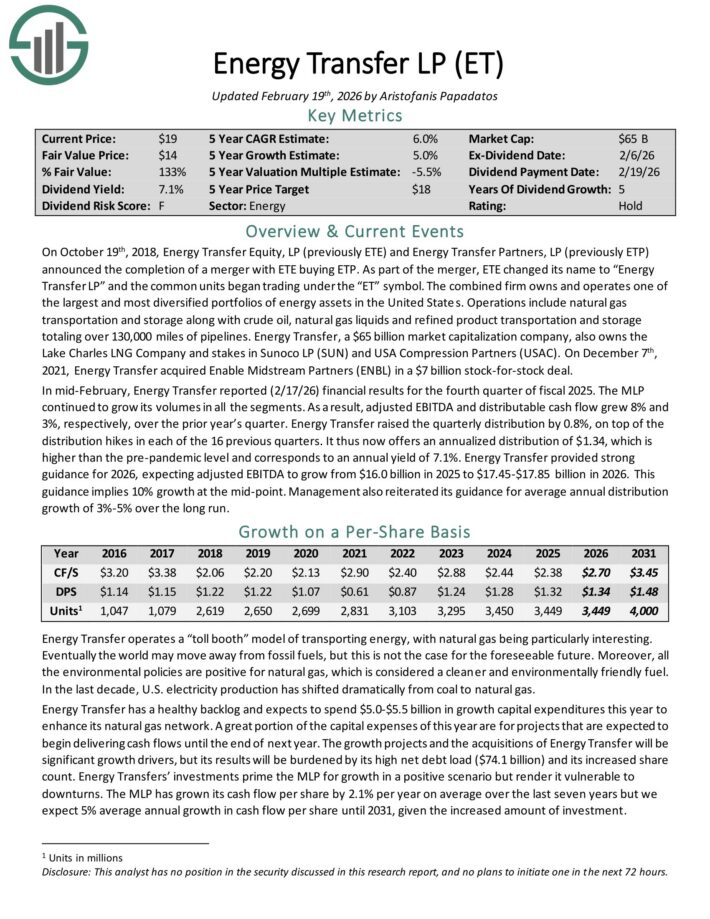

High Yield MLP #5: Energy Transfer LP (ET)

Energy Transfer LP owns and operates one of the largest and most diversified portfolios of energy assets in the United States.

Operations include natural gas transportation and storage along with crude oil, natural gas liquids and refined product transportation and storage totaling over 130,000 miles of pipelines.

Energy Transfer also owns the Lake Charles LNG Company and stakes in Sunoco LP (SUN) and USA Compression Partners (USAC).

In mid-February, Energy Transfer reported (2/17/26) financial results for the fourth quarter of fiscal 2025. The MLP continued to grow its volumes in all the segments.

As a result, adjusted EBITDA and distributable cash flow grew 8% and 3%, respectively, over the prior year’s quarter. Energy Transfer raised the quarterly distribution by 0.8%, on top of the distribution hikes in each of the 16 previous quarters.

Energy Transfer provided strong guidance for 2026, expecting adjusted EBITDA to grow from $16.0 billion in 2025 to $17.45-$17.85 billion in 2026. This guidance implies 10% growth at the mid-point.

Click here to download our most recent Sure Analysis report on ET (preview of page 1 of 3 shown below):

High Yield MLP #4: MPLX LP (MPLX)

MPLX LP is a Master Limited Partnership that was formed by the Marathon Petroleum Corporation (MPC) in 2012. In 2019, MPLX acquired Andeavor Logistics LP.

The business operates in two segments:

Logistics and Storage, which relates to crude oil and refined petroleum products

Gathering and Processing, which relates to natural gas and natural gas liquids (NGLs)

On October 28th, 2025, MPLX announced a quarterly distribution of $1.0765 per unit, which was a 12.5% raise.

In early May, MPLX reported (5/5/26) financial results for the first quarter of fiscal 2026. Adjusted EBITDA dipped -2% while distributable cash flow (DCF) per share declined -5% over the prior year’s quarter.

The MLP reported higher tariff rates but was hurt by hedging losses and higher interest expense. MPLX maintained a decent consolidated debt to adjusted EBITDA ratio of 3.7x and a healthy distribution coverage ratio of 1.3x.

The recently acquired assets in the Utica and Permian basins have begun to generate cash flows.

Click here to download our most recent Sure Analysis report on MPLX (preview of page 1 of 3 shown below):

High Yield MLP #3: Hess Midstream LP (HESM)

Hess Midstream LP owns and operates midstream assets primarily located in the Bakken and Three Forks Shale plays in North Dakota. It provides oil, gas and water midstream services to Hess and third-party customers in the U.S.

Hess Midstream has long-term commercial contracts, which extend through 2033. Its contracts are 100% fee-based and minimize the exposure of the company to commodity prices.

In early May, Hess Midstream reported (5/4/26) financial results for the first quarter of fiscal 2025. Throughput volumes increased 1% for gas processing but decreased -5% for oil terminaling and -9% for water gathering over the prior year’s quarter due to lower production, which was caused by fewer new wells.

Nevertheless, thanks to lower general and administrative expenses, earnings-per-share grew 5%, from $0.65 to $0.68. Management reaffirmed its guidance for 2026 thanks to positive business momentum in all segments.

It expects 10% growth of throughput volumes, 11% growth of adjusted EBITDA and at least 5% annual growth of distributions until 2027.

It also continues to prioritize financial strength and expects to reduce leverage ratio (Net Debt to EBITDA) below 2.5x by the end of this year.

Click here to download our most recent Sure Analysis report on HESM (preview of page 1 of 3 shown below):

High Yield MLP #2: Western Midstream Partners LP (WES)

Western Midstream Partners, LP is a master limited partnership that is focused on gathering, compressing, treating, processing, and transporting natural gas.

It also transports natural gas liquids and crude oil and gathers, transports, recycles, treats, and disposes of produced water for its customers.

Its key operational regions are Texas, New Mexico and the Rocky Mountains.

In early May, Western Midstream Partners reported (5/6/26) financial results for the first quarter of fiscal 2026. Total natural gas volumes grew 6% over the prior year’s quarter, to record levels.

Earnings-per-share nearly doubled, from $0.47 to $0.87, exceeding the analysts’ estimates by $0.09. Moreover, thanks to positive prospects from recent growth projects, management provided positive guidance for 2026.

It expects adjusted EBITDA near the high end of previous guidance of $2.5-$2.7 billion, implying ~9% growth. It also raised the quarterly distribution by 2%.

Click here to download our most recent Sure Analysis report on WES (preview of page 1 of 3 shown below):

High Yield MLP #1: Delek Logistics Partners LP (DKL)

Distribution yield: 10.7%

Delek Logistics Partners, LP is a publicly traded master limited partnership (MLP) headquartered in Brentwood, Tennessee.

Established in 2012 by Delek US Holdings, Inc. (NYSE: DK), Delek Logistics owns and operates a network of midstream energy infrastructure assets.

These assets include approximately 850 miles of crude oil and refined product transportation pipelines and a 700-mile crude oil gathering system, primarily located in the southeastern United States and west Texas.

The company’s operations are integral to Delek US’s refining activities, particularly supporting refineries in Tyler, Texas, and El Dorado, Arkansas.

On April 29th, 2026, Delek Logistics Partners released its first-quarter results for fiscal 2026. Earnings-per-share and distributable cash flow per share decreased -18% and -4%, respectively, over the prior year’s quarter due to the impact of winter storm Fern.

Despite this headwind, the MLP exhibited solid business execution and thus its management reiterated its guidance for 2026. It still expects EBITDA of $520-$560 million, thus implying just 1% growth at the midpoint.

We expect the MLP to benefit from the ongoing war in Iran, as U.S. producers are likely to increase their output amid sky-high oil prices.

Click here to download our most recent Sure Analysis report on DKL (preview of page 1 of 3 shown below):

Final Thoughts

Income investors will find a lot to like about Master Limited Partnerships. Specifically, MLPs tend to have very high yields.

Of course, investors should always do their own research to understand the unique tax implications and risk factors of MLPs.

But for income investors primarily looking for high yields, these MLPs may be attractive.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research:

Other Sure Dividend Resources:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

Still Runs on Special-Situations Advisory Demand More Than a Simple Valuation Screen")

{kind=link}