Published on May 14th, 2026 by Nathan Parsh

Dynacor Group (DNGDF) has two appealing investment characteristics:

#1: It is offering a slightly above-average dividend yield of 2.4%, which is double the average dividend yield of the S&P 500.

#2: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yields and payout ratios) by clicking on the link below:

The combination of an above-average dividend yield and a monthly dividend makes Dynacor an attractive option for individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about Dynacor.

Business Overview

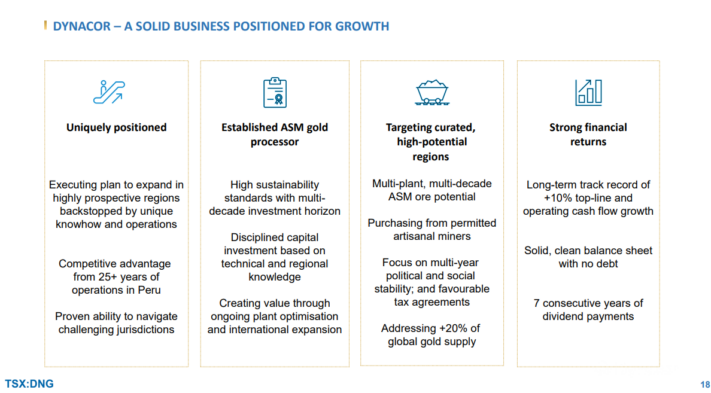

Dynacor is an industrial gold processor with core operations in Peru, where it purchases ore from artisanal and small-scale miners and processes it at its wholly owned Veta Dorada plant in Chala.

The facility has a nameplate capacity of 430 tons per day and is optimized for continuous, high-efficiency throughput. The company was founded in 1996 and is headquartered in Montreal, Canada.

The business model of Dynacor is unique in that it does not engage in exploration or mining; instead the company operates an extensive ore-purchasing network across Peru to source high-grade feedstock.

Dynacor operates a strong logistics network for collecting ore, runs its own labs for analysis, and handles gold exports with secure, reliable systems. Dynacor also reinvests in expanding its supply network and enhancing plant capacity, while maintaining a lean cost structure and consistent production flow.

Dynacor has greatly benefited from the highly inflationary environment that has prevailed since 2022. The unprecedented fiscal stimulus packages offered by most governments during the coronavirus crisis led to a surge of inflation to a 40-year high in 2022.

During inflationary periods, investors rush to buy gold, as the precious metal has always provided great protection against inflation. As a result, the price of gold has nearly triple, from approximately $1,700 in early 2022 to $4,692 right now.

The rally of the price of gold has been clearly reflected in the business results of Dynacor. The company nearly tripled its earnings per share, from $0.11 in 2020 to $0.30 in 2021. The company then posted all-time high earnings per share of $0.46 for 2024.

The company then followed that up with an impressive performance in both the fourth quarter and full year 2025. For the quarter, revenue grew 88% to $137.4 million while net income was up nearly fourfold to $7.2 million. Earnings per share improved to $0.17 from $0.05 in the prior year.

These gains were driven by both unprecedented gold prices and a significant rebound in sales volumes following the resolution of earlier supply chain issues. Gold sales totaled 32,838 gold-equivalent ounces, up from 27,417 ounces in the same period of 2024. The average selling price reached a record $4,135 per ounce during the quarter, compared to roughly $2,663 per ounce in the prior-year period.

For the year, earnings per share increased 10.2% to $0.51.

For 2026, we expect earnings per share of approximately $0.40.

Growth Prospects

The performance of Dynacor over the past decade reflects a slow-building but ultimately sharp improvement in profitability, underpinned by operational discipline, plant optimization, and favorable gold market conditions.

From 2015 to 2019, earnings per share rose incrementally from $0.09 to $0.13, reflecting slow but steady progress as the company ramped up the throughput at its Veta Dorada plant and expanded its ore purchasing network in Peru.

These years saw operational discipline, but earnings growth was limited by moderate gold prices and the early-stage scale of the business. However, as mentioned above, growth of earnings per share has greatly accelerated in the last few years.

It is also important to note that the company has consistently grown its production over the last decade.

Source: Investor Presentation

More precisely, Dynacor has grown its production nearly doubled between 2021 and 2025.

We expect the company to continue growing its output significantly over the next five years. As we also expect strong gold prices to remain in place for the foreseeable future, we expect Dynacor to grow its earnings per share at an 8% average annual rate over the next five years.

Thanks to its blowout earnings in recent years, Dynacor has a rock-solid balance sheet. To be sure, it is one of the very few companies that does not pay any interest expense, as its interest income exceeds its interest expense. Moreover, the company does not have any debt; instead it has a net cash position of $19 million.

As the net cash position is 11% of the market capitalization of the stock, it is certainly excessive. Overall, the rock-solid financial position of Dynacor is a testament to the strength of its business model.

Dividend & Valuation Analysis

Dynacor is currently offering market beating dividend yield of 2.4%, which is more than twice that of the average yield of the S&P 500. The stock is an interesting candidate for income investors, but they should be aware that the dividend is not entirely safe due to the cycles of the price of gold.

Dynacor has a reasonable expected payout ratio of 28% for 2026, which provides a decent margin of safety for the dividend. Moreover, thanks to the promising growth prospects and the pristine balance sheet of the company, its dividend should be considered safe in the absence of a major downturn.

In reference to the valuation, Dynacor is currently trading for 11.4 times its expected earnings per share this year. We assume a fair price-to-earnings ratio of 9.0 for this stock.

Therefore, the current earnings multiple is higher than our assumed fair price-to-earnings ratio. If the stock trades at its fair valuation level in five years, then multiple contraction will lower annual returns by 4.7% over this period.

Taking into account 8% expected growth of earnings per share over the next five years, the 2.4% current dividend yield, and a headwind from multiple compression, Dynacor could offer a 5.5% average annual total return over the next five years. This indicates that the stock is not exactly attractive right now from a total return perspective.

Final Thoughts

Dynacor has promising growth prospects thanks to production growth and potentially higher gold prices in the upcoming years. The stock is offering a decent dividend yield that appears safe.

On the other hand, the company has proven highly vulnerable to the cycles of the price of gold. As a result, it is suitable only for patient investors, who can endure high stock price volatility .

We rate the stock as a hold due to expected total returns over the next five years.

Additional Reading

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

-1024x683.jpg "Strait Outta Hormuz: Getting the Iran Oil Story Straight")

")

-1024x683.jpg "The Do-Nothing Congress Strikes Again – And the Clock Is Ticking")

{kind=link}