AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $14.20 (-0.5%)

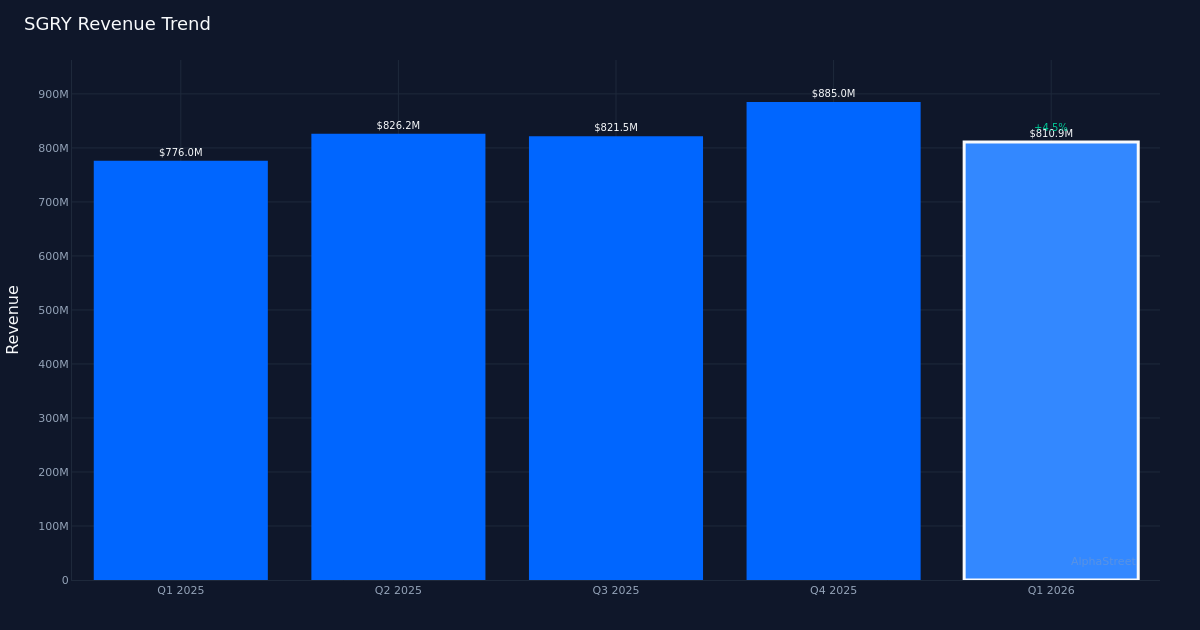

Better-than-expected quarter. Surgery Partners, Inc. (NASDAQ: SGRY) posted a Q1 2026 adjusted loss of $0.03 per share, significantly narrower than the expected loss of $0.12 per share. Revenue totaled $810.9M for the quarter, representing a 4.5% increase from the $776.0M recorded in Q1 2025. The bottom line showed an adjusted net loss of $4.1M, demonstrating meaningful progress toward profitability as the operator of ambulatory surgery centers continues to scale its platform of 122 total consolidated surgical facilities.

Organic growth momentum. The company’s same-facility revenue growth of 4.4% for the quarter indicates healthy underlying demand at existing locations rather than reliance purely on acquisitions. This metric is particularly important for surgical facility operators, as it reflects patient volume trends, case mix improvements, and pricing power within established sites. The close alignment between same-facility growth at 4.4% and total revenue growth at 4.5% suggests the company’s expansion strategy is complementing rather than masking organic performance, a quality indicator for investors evaluating the durability of this growth trajectory.

Full-year outlook. Management’s full-year revenue guidance of $3.35B to $3.45B provides a meaningful framework for assessing the sustainability of current momentum. The midpoint of this range would represent continued growth from current quarterly run rates, though investors should note the company did not provide updated earnings guidance alongside the first quarter results. The revenue range allows for some variability in case volumes and payor mix while maintaining the growth narrative that has characterized the surgical facility consolidation story across the sector.

Muted market reaction. Despite the sizable earnings beat, SGRY shares traded largely unchanged following the report. This tepid response likely reflects the market’s focus on the absolute loss position rather than the magnitude of the beat, or perhaps concern about the absence of formal profitability guidance. The stock’s lack of movement suggests investors may be waiting for sustained positive earnings before reassessing valuation multiples, even as the company demonstrates clear progress on its path to consistent profitability.

Analyst sentiment. Wall Street maintains a constructive view on the shares, with consensus standing at 9 buy ratings, 4 hold ratings, and 0 sell ratings. This positive skew reflects confidence in the company’s market position within the ambulatory surgery center consolidation trend, though the presence of four hold ratings indicates some analysts are waiting for clearer evidence of sustained earnings power before upgrading to more aggressive recommendations.

What to Watch: The critical question is whether Surgery Partners can maintain this same-facility growth momentum while converting incremental revenue into positive earnings. With 122 facilities now in the portfolio, the operating leverage inherent in the model should begin materializing more visibly in coming quarters. Investors should monitor whether Q2 results show continued narrowing of losses or potentially the company’s first profitable quarter on an adjusted basis, which would validate the thesis that scale is finally translating to sustainable profitability.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

")

{kind=link}