Updated on May 1st, 2026 by Nathan Parsh

Northland Power (NPIFF) has two appealing investment characteristics:

#1: It is offering an above-average dividend yield of 3.0%, which is nearly three times the 1.1% dividend yield of the S&P 500.

#2: It pays dividends monthly instead of quarterly.Related: List of monthly dividend stocks

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

Northland Power’s combination of an above-average and monthly dividend yield makes it appealing to individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about Northland Power.

Business Overview

Northland Power is an independent power producer that develops, builds, owns, and operates green power projects in North America, Europe, Latin America, and Asia. The company produces electricity from renewable resources, such as wind, solar, hydroelectric power, and clean-burning natural gas and biomass for sale under power purchase agreements and other revenue arrangements.

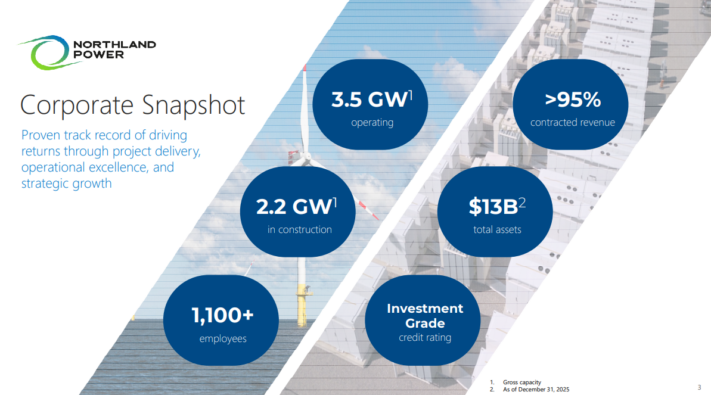

Northland Power manages 3.5 gigawatts of gross operating capacity and has approximately 2.2 GW in active construction across two flagship projects: Hai Long (Taiwan) and Baltic Power (Poland).

Northland Power greatly benefits from a strong secular trend, namely the shift of the entire world from fossil fuels to clean energy sources. This shift has dramatically accelerated since the onset of the coronavirus crisis about three years ago.

The tailwind from this secular trend is clearly reflected in Northland Power’s growth trajectory.

Source: Investor Presentation

The company has expanded from just one country in 2015 to seven countries now. During this period, Northland Power has essentially tripled its generating capacity.

Thanks to its essential nature and high-growth mode of business, Northland Power proved essentially immune to the coronavirus crisis. In addition, thanks to its ability to pass on its increased costs to its customers, the company has proved resilient in the highly inflationary environment prevailing right now.

Growth Prospects

As mentioned above, Northland Power has a major growth driver in place, namely the global shift from fossil fuels to renewable energy sources. This shift has greatly accelerated in the last three years and has decades to run.

It is also important to note that most renewable energy sources had high production costs in the past, and thus, they needed government subsidies to become economically viable. However, thanks to major technological advances, this is not the case anymore. The production cost of solar and wind energy has pronouncedly decreased, and hence, renewable energy sources can easily replace fossil fuels nowadays. To provide a perspective, the cost of solar power has decreased from more than $4 per watt to less than $1 per watt over the last decade.

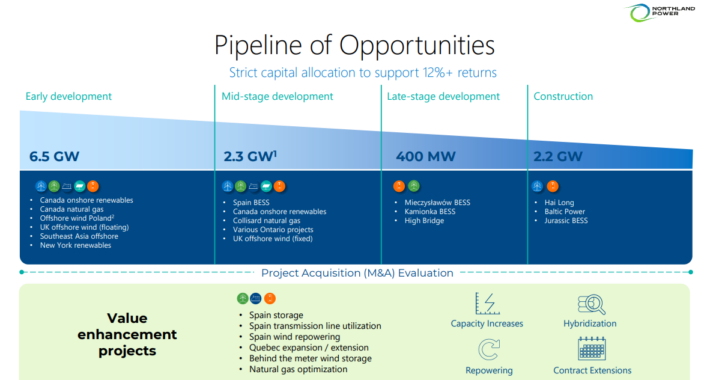

The primary growth drivers of Northland Power are depicted in the chart below.

Source: Investor Presentation

The company has several growth projects under construction right now, with a total capacity of 2.2 GW. In addition, the company’s has 9.2 GW in development. As the company’s current generating capacity is only 3.5 GW, it is evident that Northland Power has immense growth potential over the next several years.

Northland Power reported its fourth quarter and full-year 2025 results on February 25th, 2026. Revenue surged 26% year-over-year to $528 million. Growth was driven by record-high production from German offshore wind assets, increased demand for dispatchable power at natural gas facilities, and the first full-quarter contribution from the Oneida battery storage project. These gains were partially offset by lower market prices for Spanish assets.

Adjusted EBITDA grew 25% $285 million as fleet availability was 96%. Strong offshore wind conditions also aided results. Quarterly net income was $212 million, but the company ended the year with a $79 million net loss, mainly due to a $324 million non-cash impairment at Nordsee One in the third quarter. Importantly, Northland reached the high end of its revised 2025 guidance.

The company issued 2026 Adjusted EBITDA guidance for the year, with a projected range of $1.06 billion to $1.20 billion (CAD $1.45 billion to $1.65 billion). This will be driven by progress at Hai Long and Baltic Power and the expected late-year startup of the Jurassic storage facility.

We expect that Northland Power will generate earnings-per-share of $1.43 for the year. The company is projected to grow EPS at a rate of 2.0% annually through 2031.

Dividend & Valuation Analysis

Northland Power currently offers a solid yield of 3.0%, which is above that of the average yield of the S&P 500. The stock is thus an interesting candidate for income-oriented investors, but the latter should be aware that the dividend is affected by the fluctuation of the exchange rate between the Canadian dollar and the USD.

While Northland Power has posted payout ratios of over 100% in the past, but the projected payout ratio for 2026 is just 36%. The company also has a healthy balance sheet, with a stable BBB credit rating from S&P. Given its promising growth prospects and resilience to recessions, its dividend (in CAD) should be considered safe with some risk if earnings do not improve.

On the other hand, investors should note that Northland Power has failed to grow its dividend meaningfully over the last decade, primarily due to the devaluation of the Canadian dollar vs. the USD. As a result, it is prudent not to expect meaningful dividend growth going forward.

Shares of the company are trading at 12.0 our EPS estimates for the year, which is below our target of 12.5. Reverting to our multiple by 2031 would add 0.7% to annual returns over this period.

Combined with the 2.0% EPS growth rate, the 3.0% starting dividend yield, and a small tailwind from multiple expansion, we forecast total annual returns of 5.5% over the next five years.

Final Thoughts

Northland Power has solid business model. Even better, the company has ample room to continue growing for decades. Moreover, the stock offers a decent yield of 3.0% that is supported by a reasonable payout ratio. It thus combines many positive features suitable not only for income-oriented investors but also for growth-oriented investors.

However, investors should be aware that the stock is highly volatile during periods when its growth decelerates. Therefore, only patient investors, who can ignore short-term pressure and remain focused on the long run, should consider purchasing this stock.

Don’t miss the resources below for more monthly dividend stock investing research.

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

")

-1024x683.jpg "Strait Outta Hormuz: Getting the Iran Oil Story Straight")

-1024x683.jpg "Trump, Congress, and the FISA Fiasco")

Has an AI-Systems and Hybrid-IT Story Bigger Than the Legacy-Hardware Label")

{kind=link}